Grayscale: It's time to change the pledge model of the Taicha

Community discussions are under way to establish a pledge incentive cap curve, which Grayscale considers to be a long-term benefit for ETH prices. 。

Original by Zach Pandl, Research Manager, Grayscale

& nbsp; yuan w ed: Deep tide TechFlow

Introduction:Zach Pandl, Research Manager of & nbsp; Grayscale, notes that the current pledge incentive model of the Taifung is facing two structural problems: L2 diversion leading to a decrease in the destruction of tokens and a rise in the net increase in hair; and a pledge threshold approaching zero, which may eventually lock almost all ETH into the pledge. Community discussions are under way to set up a pledge incentive cap curve, which Grayscale considers to be of long-term benefit to ETH prices。

The Taifeng community is considering revising the network ' s pledge reward model, with the core idea being to encourage only a certain percentage of the pledge, beyond which no additional incentive will be given. If landed, the pledge ' s nominal gains would be reduced. But Graysdale believes that this is a long-term good thing for ETH prices for two reasons: control of ETH inflation and enhancement of the narrative of ETH as a value storage asset。

This reform discussion was driven by two overlapping issues。

Deterioration of token destruction and net increase

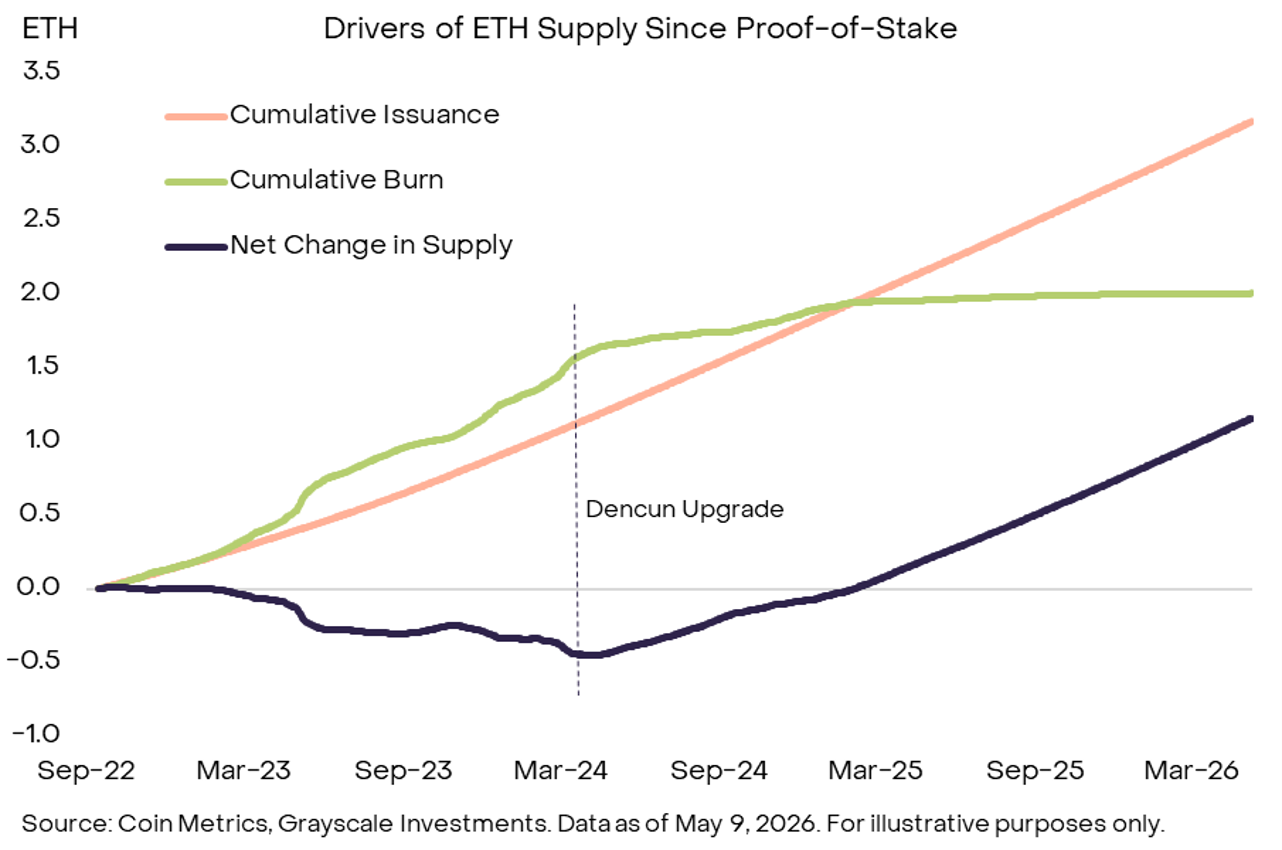

THE SUPPLY OF ETH DEPENDS ON THE DIFFERENCE BETWEEN NEW ISSUANCE AND TOKEN DESTRUCTION. AT PRESENT, THE ETA L1 WILL DESTROY ALL BASIC TRANSACTION CHARGES, WHICH MEANS THAT MORE ETH WILL BURN DOWN AND SUPPLY GROWTH WILL BE CURTAILED。

CHANGES OVER THE PAST FEW YEARS HAVE UPSET THIS BALANCE. AN INCREASING NUMBER OF ACTIVITIES HAVE BEEN RELOCATED TO THE L2 NETWORK, RESULTING IN LOWER TRANSACTION COSTS AND THE DESTRUCTION OF TOKENS AND A RISE IN NET GAINS。

Figure: Drivers of ETH supply changes since Exhibit 1 - POS. After the upgrading of Dencun, cumulative destruction levels (Green Line) were flat, while cumulative distribution (Orange Line) continued to rise, leading to a change in net supply of ETH (Dark Line) from negative to positive. Source: Coin Metrics, Grayscale Investments, data as of 9 May 2026

To make matters worse, Etherport L1 is now actively opting for an expansion to counter competition in high-volume chains like Solana. Pandl: L1 transaction costs will remain low in the foreseeable future, currency destruction will remain low and net supply growth will further increase。

The cost of friction on the pledge is almost zero

WHEN THE PLEDGE WAS LAUNCHED AT THE EARLIEST IN THE TAIFENG, THE USER WAS UNABLE TO EXTRACT THE ASSET, AND THE ETH PLEDGE WAS LOCKED IN A BAD LIQUIDITY CONDITION AND THEREFORE THERE WAS A RISK PREMIUM. DRAWDOWNS ARE NOW OPEN AND LIQUIDITY HAS IMPROVED SIGNIFICANTLY, RESULTING IN A EVAPORATION OF THE RISK PREMIUM。

MORE CRITICALLY, MOBILE PLEDGE TOKENS (LSTS), EXCHANGE TRADED PRODUCTS (ETPS) AND THE ENTERPRISE ETH TREASURY HAVE JOINED THE PLEDGE. THE MARGINAL COST OF PLEDGE ETH IS NOW CLOSE TO ZERO. AS LONG AS THE NETWORK CONTINUES TO YIELD MARGINAL GAINS TO THE PLEDGE, ALMOST ALL ETH MAY EVENTUALLY BE PLEDGED。

The pledge is a necessary condition for the proper functioning of the Taifeng Agreement, but an excessive pledge rate may be counterproductive。

Two risks. First, unnecessary dilution. Net increases do not substantially enhance cybersecurity, as a country spends too much on defence, but do nothing to help national security. Second, a few agencies dominate the risk of centralization of pledge activities. This possibility exists because of the network effects of service providers。

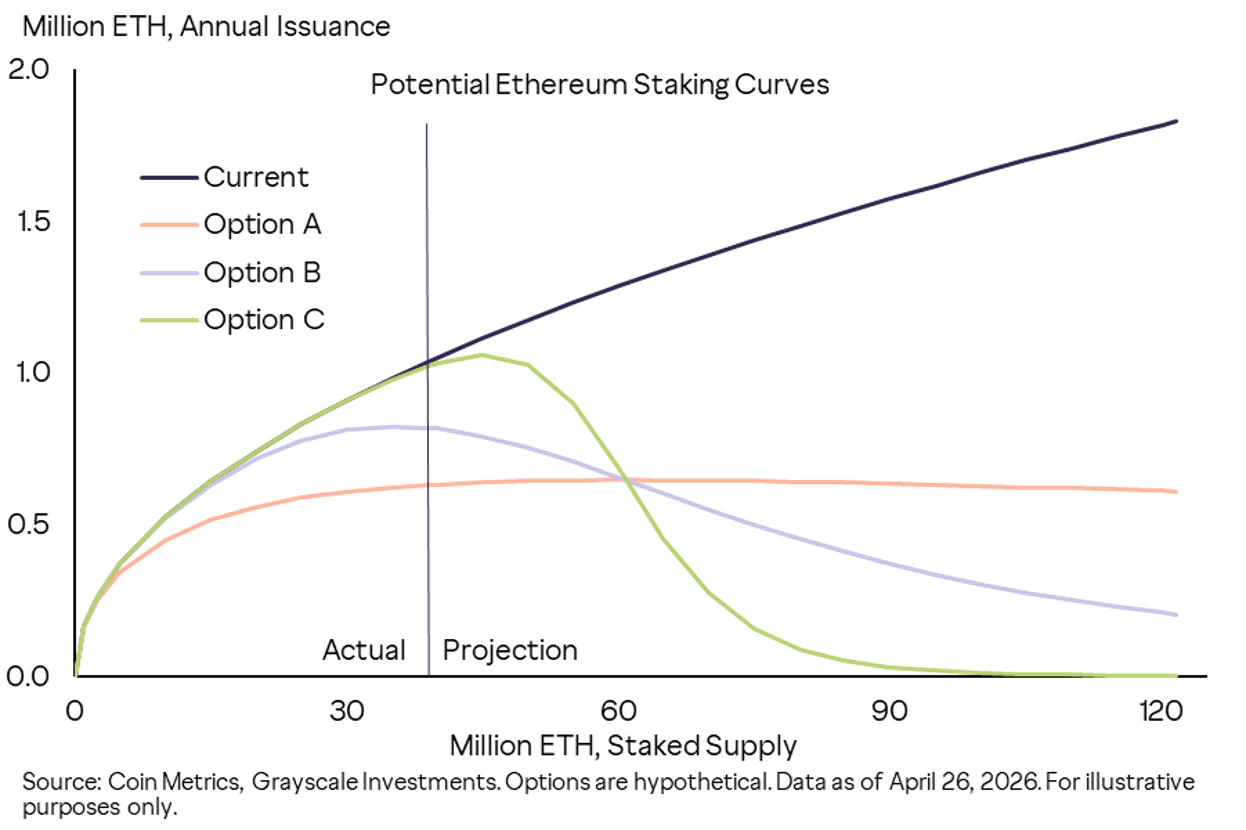

Set pledge reward ceiling curve

One solution would be to move to incentive models that only stimulate pledge to a certain level。

Figure: Exhibit 2 - Alternative pledge incentive curves that may be considered in the Taifeng. Under the current model (dark line), annualized distribution increases linearly with the pledge; the three options, Option A/B/C, have caps or nodes at different pledge levels, allowing circulation to flatten or even decrease when the pledge ratio exceeds a certain threshold. Source: Coin Metrics, Grayscale Investments, data as of 26 April 2026, options are scenarios

Graysdale believes that this change has long been beneficial to the market value of ETH. ETH is a functional commodity, not a financial claim like equities and bonds, and should not be priced solely on the basis of cash flows. Updating the pledge incentive model reduces supply growth and increases the scarcity of ETH. For bulk commodities, a good price reduction is the same logic as ETH。

Reducing end-of-network risk and controlling long-term inflation also increases the need for unstaked ETH to store assets as digital value。

THERE IS ALSO AN EASILY OVERLOOKED PERSPECTIVE: ETH PRICE VOLATILITY HAS A FAR GREATER IMPACT ON INVESTMENT RETURNS THAN ON PLEDGE RETURNS. THE CURRENT ANNUALIZED PLEDGE RATE OF RETURN OF ABOUT 3 PER CENT EQUALS THE PRICE VOLATILITY OF ETH FOR ONE DAY (APPROXIMATELY 60 PER CENT FOR THE 360 DAYS AND 3 PER CENT FOR THE DAY)。

Conclusions& nbsp; Possible modifications of the pledge incentive model in the Taifeng to control long-term supply growth and reduce specific tail risks. If you land, Graysdale thinks it's good for ETH prices。