a16z is devouring seed wheels: 20 top VC 10 data disassembled

If a16z and Sequoia were to end up, would it make sense to invest in seed money?

This post is part of our special coverage Syria Protests 2011

Original: Deep tide TechFlow

Introduction: large funds of over $10 billion are being managed at an unprecedented rate. Murph Capital pulled Harmonic's data and dismantled the early investment behaviour of 20 top-level mega-funds in the three cycles of SaaS, zero interest rate and AI. The conclusion is not simple: mega-fund seed rotation rates are indeed 3.7-4.2 times the market average, but when they are deployed, this advantage is quickly diluted. For emerging managers, living space still exists, but the right track must be chosen。

A month ago, I sent a tweet asking a simple question: is a giant fund really taking over the seed wheel, or is it just feeling like that? After over 65,000 visits and hundreds of private letters, it is clear that the problem is painful。

The new manager (Emerging Manager, hereinafter EM) wrote that they felt pressure but could not quantify it; the LP asked: If a16z and Sequoia had ended up, would it make sense to throw seed money? The G.P.P., a major fund, would like to know how radical the competitors were at an early stage。

@pavelprata push:IS THE GIANT FUND REALLY TAKING OVER THE SEED WHEEL? I DECIDED TO STUDY THE BEHAVIOUR OF THE WORLD'S LARGEST VC FUND (MORE THAN $10 BILLION AUM) AT AN EARLY STAGE AND ANSWER A SIMPLE QUESTION: EM SHOULD BE CONCERNED ABOUT ITS STRUCTURAL ADVANTAGES

A broad consensus quickly emerged, and I generally agree:

- The mega-fund did significantly increase the distribution of seed wheels, about three times in the last decade

- Markets are sufficiently large and dispersed, and their share remains relatively small, concentrated in the top fours

- Their core motivation is not immediate capital returns, but early exposure to talent, high-value data, minimizing the risk of missing the next generation

But consensus is only the starting point. There is a much more interesting and uneven picture behind the larger direction, and the data is not visible。

so we pulled & nbsp;Harmonic& nbsp; data collected & nbsp;Twenty mega-funds in three times(SaaS, zero interest rate, AI), trying to answer honestly: What happened to the seed-wheel market? Where are the giant funds going? How does this affect pricing? Em, is there any real reason to worry

intuitive vs. data

The research framework begins。

We rely on public information to match real-time data from Harmonic (covering over 30 million companies and 190 million people). On the time line, we have analysed the last decade, divided into three eras:

- SaaS era (2015-2019): 5 Regular annual market cycle. Clouds, SaaS, trading platforms and financial technology are mainstream narratives, interest rates are normal and markets are disciplined。

- Zero interest rate era (2020-2022): 3 annual zero interest rate policy. Capital is almost free, investors from all walks of life are rushing in for early returns, and Tiger Global and SoftBank appear to be in every round of meaningful financing. Seed wheel markets are severely overheated, but in a confusing manner and lack structural logic。

- AI AGE (2023-2026):& nbsp; from ChatGPT to today. A huge technological shock has created a new type of company for which mega-seed wheels have become normal。

Technically, we focus on seed wheels, but in practice we include Pre-Seed and Seed Extension. The reason is simple: the boundaries of these early stages are often blurred or altered, and they are disingenuous to be precise。

Get to the point. Frankly, before the study began, I had a strong hunch that mega-funds were increasingly appearing on radar at an early stage. This intuition comes largely from social media, a16z, General Catallyst and Sequoia ' s logo appear increasingly frequently in seed ship announcements, accompanied by high-profile media attacks each time. The data confirm this:

- six months before 2026, a16z participated in approximately & nbsp;48 seed wheels, 46 per cent of which were tradedI don't know. This is a systematic seed strategy, not a piecemeal bet。

- the most prominent is the size of the cheque: the median number of a16z casts is & nbsp;$10.5 millionAND IT'S MORE LIKE THE CLASSIC A WHEEL THAN THE TRADITIONAL SEED WHEEL。

- If you add General Catallyst and SequoiaThis 3 giants completed 87 seed deals in just 5.5 months, average & nbsp;Early investment per 1.5 working daysI don't know。

@a16z push:We're honored to be on the Westmag Seed Wheel. One of the undervalued advantages of investing in entire hardware stacks is to be able to access the supply chain challenges plaguing the industrial base..

At the same time, the latest data from Carta show that the valuation of seed wheels is expanding rapidly from a valuation perspective. While it may be argued that this is only the result of a small number of radical players, most EM ' s fund mathematics still forces them to operate near or below the median to obtain sufficient initial holdings and maintain a viable return path。

THE LOGIC OF MEGA-FUNDS IS COMPLETELY DIFFERENT. PRICE DISCIPLINE IS NO LONGER A REAL CONSTRAINT WITH ACCUMULATION OF AUM, BRAND PREMIUMS AND HIGH-QUALITY PROJECT FLOWS. THIS GAP IS TEARING THE MARKET APART INTO TWO DISTINCT LAYERS, WHICH WE CALL MORE OR LESS "CLASSIC SEED WHEELS" AND "SUPER-SEED WHEELS":

- THE 90TH PERCENTILE OF THE SEED WHEEL VALUATION IN 2026 Q1 JUMPED TO $93.7 MILLIONIt's almost double that four years ago

- In the past yearValue above median increased by at least 53 per cent

- At the bottom, there's hardly any movement:25 percentiles slowly climbed from $18 million to $22.7 million

@PeterJ Walker push:THE FIRST 5 PER CENT OF THE SEED WHEEL VALUATIONS ARE NOW OFTEN IN EXCESS OF $175 MILLION, WHICH HAS TRIPLED OVER THE PAST 12 MONTHS. THERE'S A LITTLE BIT OF THE RIDICULOUS SMELL OF 2021。

But all this is still circumstantial evidence that points to a broad direction without giving a definitive answer as to what happened in the early market and how systematically large funds exist。

THAT IS WHY WE DECIDED TO DIG DEEP. WE'VE ANALYZED THE INDIVIDUAL DYNAMICS OF EACH FUND IN THREE TIMES, THE PATTERNS OF THEIR BEHAVIOR, AND WHAT THIS SHIFT ULTIMATELY MEANS FOR EM。

Dismantling trading machines

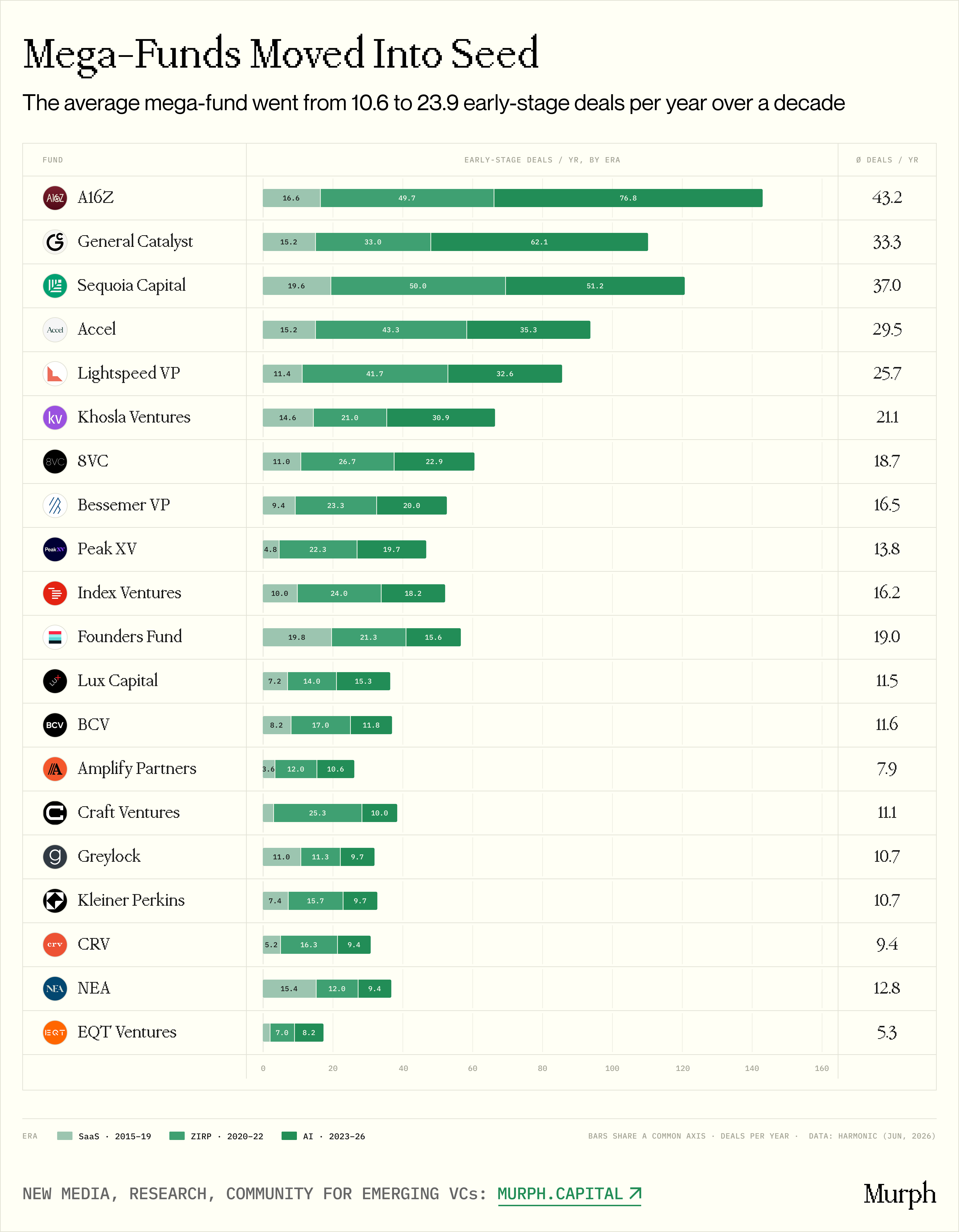

Figure 20 Comparison of the number of mega-funds trading early in the three eras

On average, a typical SaaS-era mega-fund is completed every year & nbsp;10.6 Early transactionsI DON'T KNOW. BY THE TIME OF AI23.9 pensAnd the whole queue grew by an average of 2.37 times。

WHAT'S INTERESTING IS WHAT HAPPENED AFTER THE ZERO INTEREST RATE ENDED. IF THIS INCREASE IS SIMPLY A BY-PRODUCT OF FREE FUNDING, THE INCREASE SHOULD BE REVERSED. BUT OF THE 20 FUNDS IN OUR DATA SET, THE AVERAGE NUMBER OF AI TRANSACTIONS PER YEAR IS ALMOST EQUAL TO THAT OF ZERO INTEREST:23.9 Yes, 24.3I don't know. In factOnly 3 funds have reduced the early investment tempoI don't know. This proves that the transition is structural, although a few anomalies raise the overall figure:

- a16z: 16.6 → 49.7 → 76.8 per year

- General Catallyst: 15.2 → 33.0 → 62.1 per year

- Khosla Ventures: 14.6 → 21.0 → 30.9 pens/year

There are at least three underlying drivers behind this:

AI-ERA COMPANIES ARE NATURALLY MORE COSTLY。& nbsp; GPU infrastructure, data pipeline, US$ 30-500,000 annually for research scientists, creating completely different baseline costs. The SaaS era is half a million dollars worth of what can be done (two engineers plus AWS), and the AI era needs two to five million dollars. The expanded median cheque reflects, in part, real R & D expenditure, not just an inflation in valuation. Moreover, the early days of the SaaS era were essentially exploratory in nature (which allowed the founders to change, transform, spend years looking for PDF), and AI had a much shorter pre-emptive edge window. If your model goes through, you'll lose the competition quickly, and this window closes faster。

Competition over the founders shifted pricing power。 In the early stages of the revolutionary technology cycle, high-capacity combinations with top-level talent are valuable. The best AI founders can choose between a16z, Sequoia and Lightseed in the seed phase and build a list of shareholders that can help them to melt into a larger next round in a shorter time. In many cases, pricing rights have shifted from investors to the founders: the wheel has grown not because companies objectively need more capital, but because the founders can demand and get it。

The math of the size of the fund is telling。 in our queue & nbsp;AUM GREW FROM ABOUT $34 BILLION TO $24.9 BILLION, OR ABOUT SEVEN TIMES OVER A DECADEI DON'T KNOW. AT THE SAME TIME, THEIR SEED TRADE HAS INCREASED ONLY 2-4 TIMES. AUM EXPANDS MUCH FASTER THAN SEED ACTIVITY, AND SEED CHECKS ARE SMALLER THAN IN THE PORTFOLIO OF THESE FUNDS。

Take a16z: Management is about $4 billion in 2015 and now manages $90 billion (calculating the latest $15 billion fund-raising, VC history is the largest single book). A $6 million seed check represents only 0.01 per cent of the $90 billion AUM. In mathematics, the Fund has no incentive to bargain for each million dollar valuation. Conversely, in an increasingly concentrated market, the risk of missing intergenerational opportunities is catastrophic。

SO WE CAN SAY WITH GREAT CONFIDENCE THAT THE INFLUX OF AI-ERA MEGA-FUNDS INTO SEED SHIPS IS NOT A SPECULATIVE ACT IN THE ERA OF FREE FUNDING, BUT A STRATEGIC MISSION. THIS SHIFT HAS BEEN FACILITATED BY THE INFLUX OF HUGE CAPITAL INTO LARGE FUNDS, TOGETHER WITH THE EMERGENCE OF NEW TYPES OF COMPANIES AND TALENT WORTH COMPETING AT THE EARLIEST。

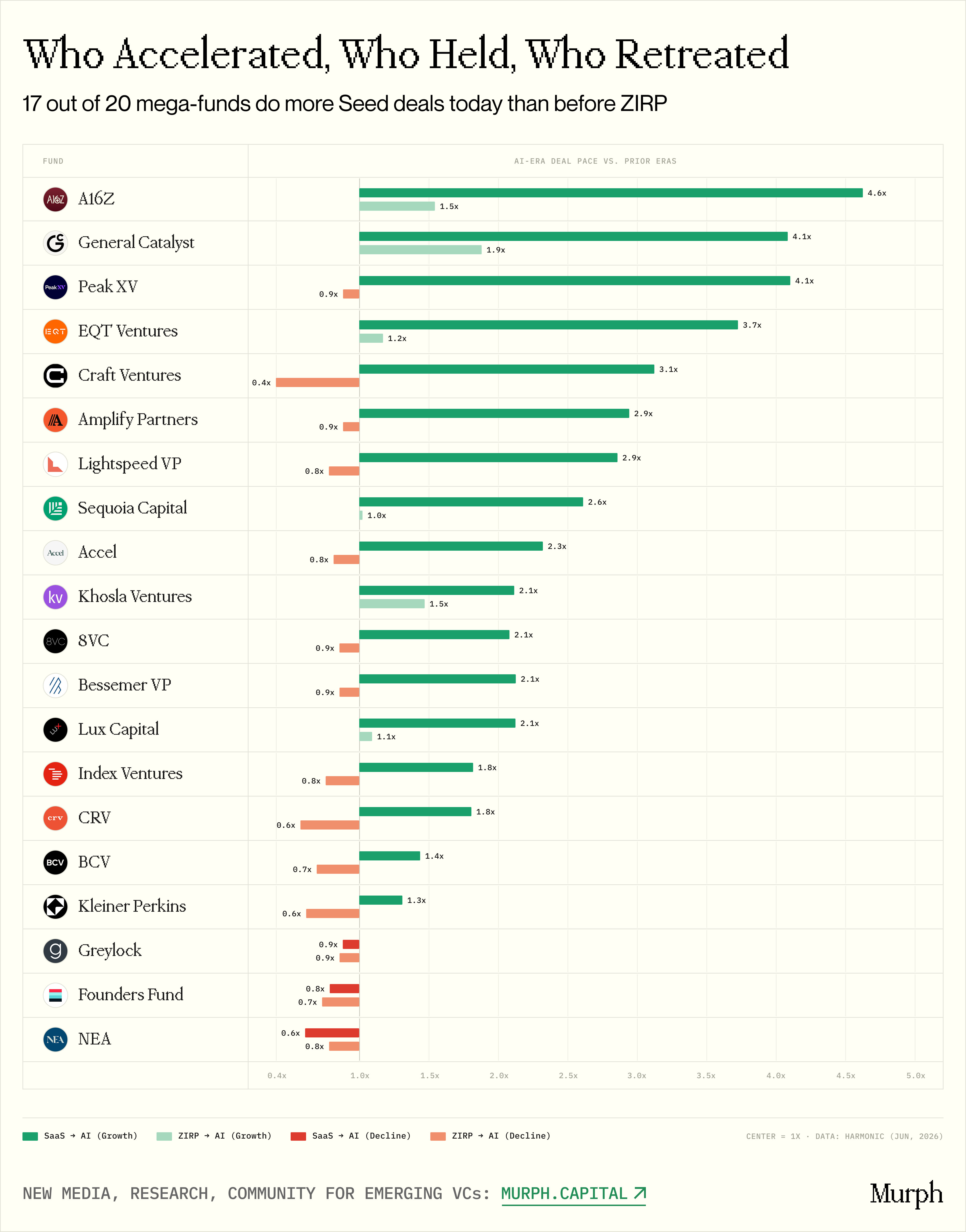

Group analysis based on increased speed

Figure 20 Funds grouped on an incremental trajectory

IN THE ERA OF ZERO INTEREST RATES, THE CONCENTRATION OF DATA IN ALL 20 MEGA-FUNDS INCREASED EARLY TRANSACTIONS WITHOUT EXCEPTION. AFTER THE EPIDEMIC, THE FED FELL NEAR ZERO, AND MASSIVE LP CAPITAL FLOWS INTO VC POCKETS, REACHING A STAGGERING $166.5 BILLION IN US VC FUND-RAISING IN 2021。

large dry powder (dry powder), some of which sank to the seed phase for water testing; the other, which took the initiative to exit from late rotations (at that time the valuation was extremely inflated), also shifted downstream。

BUT IN THE AI ERA, INTEREST RATES STABILIZED AT OVER 5 PER CENT, WITH MARKETS HIGHLY DIVIDED. THE MACRO-DIFFERING DIVIDE DIVIDED THE FUND INTO THREE LINES OF ACTION:

Accelerating

AI TRADES EVEN EXCEEDED THE ZERO INTEREST RATE PERIOD:

- a16z (75.3 per year)

- General Catalest (61.5 cases/year)

- Khosla Ventures (31.5 years)

These funds do not simply remain in the seed phase after the loss of cheap funds, but they do double their bets and dramatically expand their presence。

Stable

AI trading volumes are slightly below the zero interest rate peak, but are still much higher than the SaaS era:

- Sequoia (19.6 → 49.3 → 50.6)

- Accel (15.2 → 43.3 → 34.7 )

- Lightseed (11.6% → 41.7 → 32.1)

The sharp rise in zero interest rates has already been reversed, but baseline activities have permanently increased to two to three times the historical level. I can't go back。

Discipline

Three periods of steady growth:

- Bessemer (9.4→ 23.0→ 20.9)

- Lux (7.2→ 14.3→ 14.7)

- Index Ventures (10.0→ 23.3→ 17.6)

They avoid the spike in zero interest rates and the outbreak of AI, but the baseline has moved up permanently. The SaaS age of 10 a year is now stable at 15-21。

The only exceptions are three funds: Founders Fund, NEA and Greylock. From SaaS to AI, they either reduced or evened out early activity。

Founders Fund is probably the only institution that has made a philosophical choice. Peter Thiel was deeply influenced by the reverse framework of Giral's imitation of theory, looking for opportunities elsewhere as a clear signal of crowded market consensus. So when the other 17 mega-funds went to the seed phase, the Foundations Fund went the other way and turned to large, concentrated late-stage bets, injecting capital into intergenerational anomalies like OpenAI, Databricks, Anduril。

Greylock remains deeply committed to the "first check" tradition, but chooses to play a high concentration card. It does not engage in water-line trading machines, but rather focuses on fewer, higher-minded bets, sometimes even hatching companies directly in its own offices。

NEA ' S LARGE MULTISTAGE MISSION MAKES IT MORE DIFFICULT TO ANALYSE SEED VOLATILITY ALONE, AND WE DO NOT SPECULATE WITHOUT HARD DATA。

core configuration vs

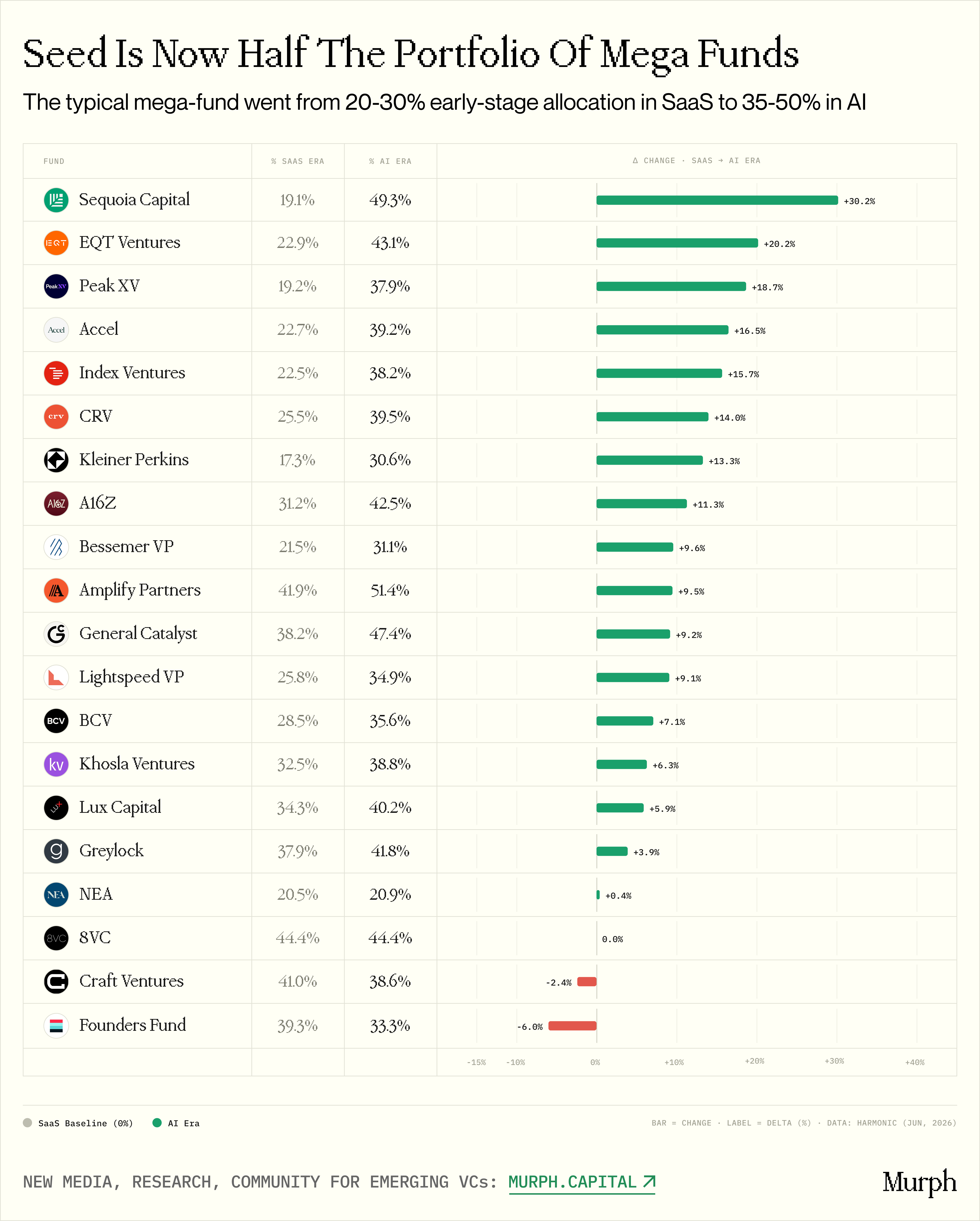

Figure: Changes in the proportion of early transactions to total investments by fund

An absolute number does not answer a key question: are seed wheels a side business or a core strategy for these giants

A FUND MAKES 30 SEEDS A YEAR, BUT IF 200 A TO D ROUNDS ARE MADE AT THE SAME TIME, THE SEEDS ARE ONLY 15%. CONVERSELY, IF 30 SEEDS CAME FROM 60 TOTAL INVESTMENTS, SEEDS ACCOUNTED FOR 50 PER CENT。

Fifteen per cent means detection projects, pet projects of individual partners, cheap options. Fifty per cent means strategic missions: specialized teams, institutionalization processes, large-scale deployment machines。

This is why our third (and perhaps most revealing) perspective tracks the exact scale of the early ecological input of each giant fund:

OF THE 20 FUNDS, 16 HAVE REACHED AN ALL-TIME HIGH IN THE EARLY YEARS OF AI。& nbsp; SaaS, a typical mega-fund will & nbsp;20-30% turnover-oriented seedsI don't know. The AI era, the baseline skyrocketed to & nbsp;35-50 per centI don't know。

Three cases were particularly persuasive:

Sequoia: complete transformation。 is the most dramatic strategic shift in our overall data concentration. In the SaaS era, Sequoia made up less than one fifth of the early investment, which was dominated by the masters of the A/B+, making tactical seed bets. By the time of AI, almost half of the transactions were in the early years, up 30 percentage points。

General Catallyst: V-shaped curve。The SaaS era GC has focused on the early years, accounting for 38%. The era of zero interest rates has fallen to 30 per cent, as has the long-term gains driven by free funding. But the AI era triggered a sharp reversal to 47%. This was a conscious and radical return to early investment, peaking higher than ever before。

a16z: AI jumps after stabilizing the baseline。The unique feature of & nbsp; a16z is that the early configuration of SaaS and the zero interest rate era was perfect at 31.2 per cent. When other funds sunk in chaos during the era of zero interest rates, a16z maintained a structural balance. Then the AI era came and jumped to 42.5%。

THIS GROUP IS IMPORTANT BECAUSE THE LP OFTEN HEARS A FAMILIAR NARRATIVE FROM A GIANT FUND: "WHEN WE MEET AN EXTRAORDINARY FOUNDING TEAM, WE WRITE A SEED CHECK. THE DATA PROVES THAT THE PHRASE IS DEAD。

Seed share of Sequoia & nbsp;49 per centGC & nbsp;47%,a16z & nbsp;42%I don't know. The mega-fund has shifted the core engine to the seed phase and weaponized this transformation with specialized teams, customizing internal corridors and own accelerator projects such as a16z Spedrun and Sequoia Arc。

FOR EM, THIS PROVIDES A CRITICAL BUT SOBERING BACKGROUND: YOUR DAILY COMPETITION HAS GONE FAR BEYOND THE $50 MILLION FINE FUND NEXT DOOR. TODAY, WHEN YOU WERE FIGHTING FOR QUOTAS, YOUR OPPONENTS WERE THE GIANTS OF $10-90 BILLION AUM, WHO HAD POINTED 40-50 PER CENT OF THE AGENCY TRADING MACHINE AT YOUR TRACK。

A key indicator to truly understand the mechanisms of such pressure would also have to be added: the size of the cheque and the rotation。

traditional seeds. vs. super seeds

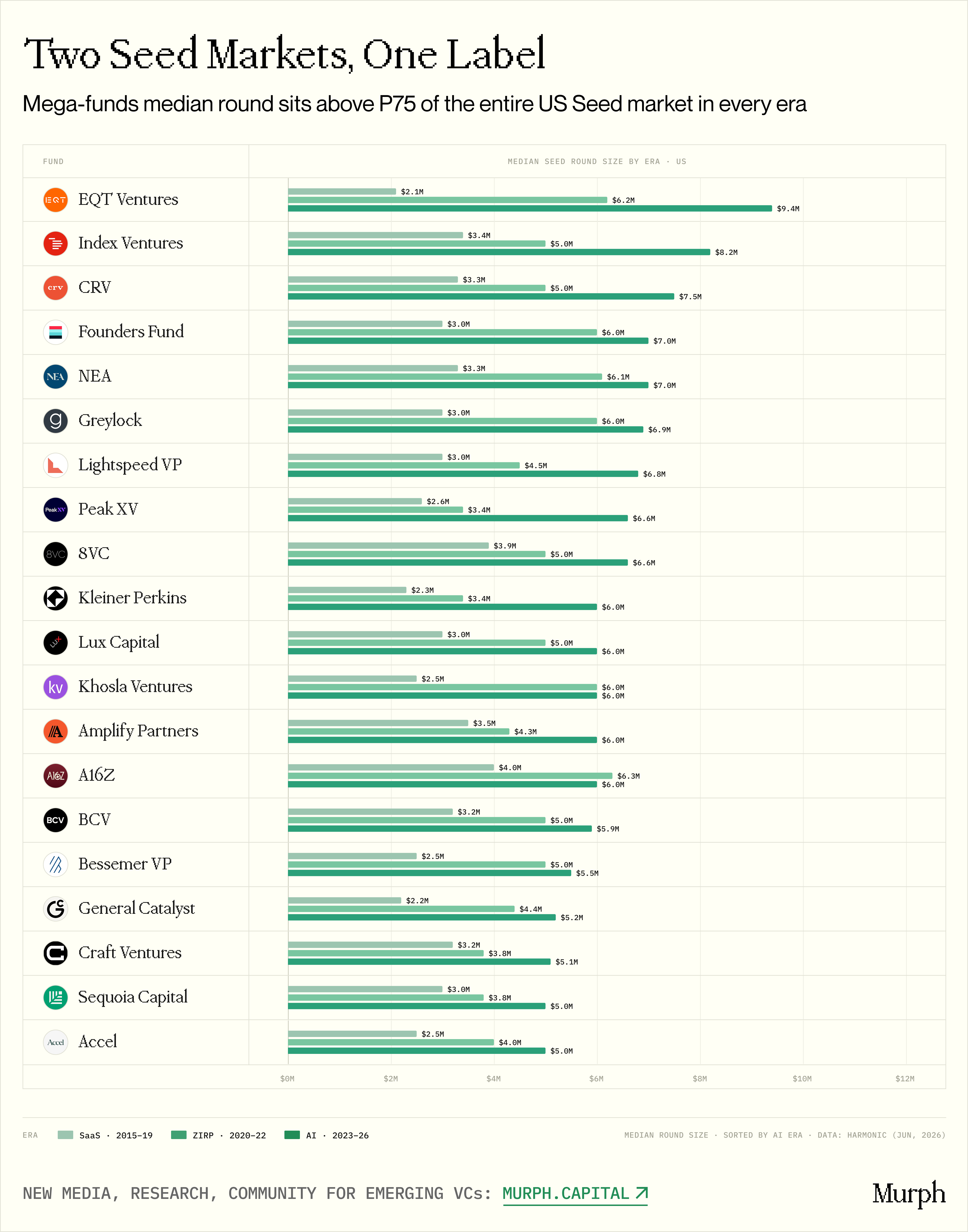

figure: medium number of seed wheels in which mega-funds participate vs. middle number in the united states seed wheel market

A central theme that we have previously highlighted is the fragmentation of the seed phase. The best way to look at this fracture is to look at the medium-rotation scale of each age and benchmark it against the “seed index” of the entire United States。

- I'M NOT SUREThe median number of American seed wheels with large funds on the shareholders' list is $6.2 million

- The market as a whole is only $1.4 millionI don't know. The gap is 4.4 times

The mega-funds do not participate at all in the "average" seed wheels, which systematically operate in the top four segments of the market。

It is even more interesting to note that the gap has remained stable in three macro cycles:SaaS 4.8 times, zero interest rate 4.5 times, AI 4.3 timesI don't know. Mega-funds have not accelerated inflation relative to the rest of the market, but they have existed at a completely different price level。

IN OTHER WORDS, THE 75TH PERCENTILE OF THE MARKET ($4.0 MILLION) IS THE ENTRY BASELINE FOR A LARGE FUND. THEIR MEDIUM ROTATION ($6.2 MILLION) IS FIRMLY ABOVE THE ENTIRE SEED ECOLOGY OF THE U.S. P75By definition, these giants are limited to 25 percent of the transactions in size. MediumI don't know。

But when we look at the medians and the averages together, things become more interesting。

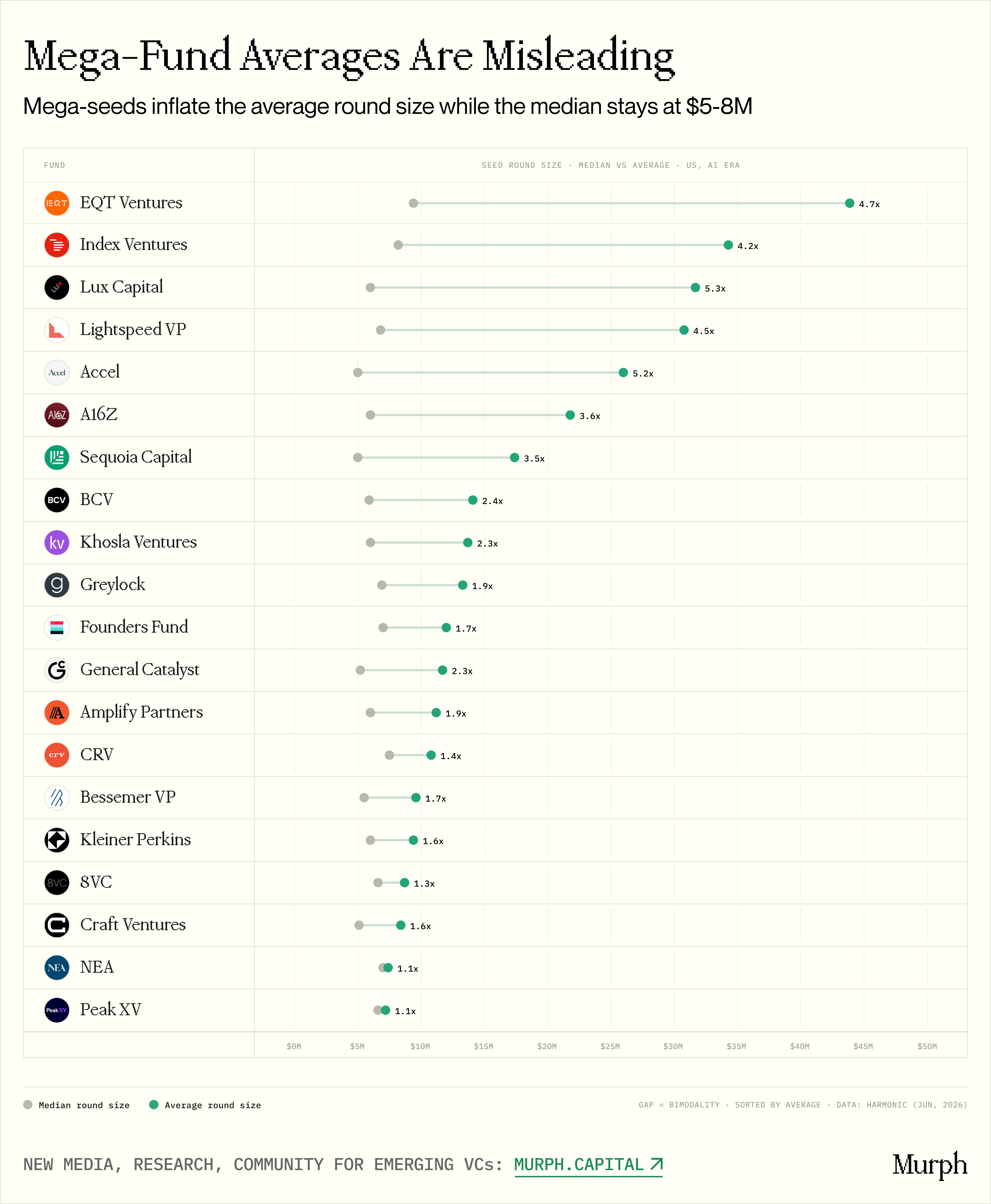

figure: median vs. averages by fund, showing two-track strategy

The median reflects a fund's “typical” transactions, with the average being significantly reduced by the anomaly. The difference between the two clearly represents how much of a fund's strategy is "two-tracked": Is it a radical double-engine model that plays superseeds at the same time, or does it work evenly at a single price level

From this perspective, the queue is clearly split into two categories。

Double track (over 3 times difference)

- Index (median 8.2 million, average 3.4.3 million, 4.2 value difference)

- Lux (6 million vs. 317 million, 5.3 times)

- Lightseed (6.8 million vs. 30.8 million, 4.5 times)

- Ascel (5 million vs. 26 million, 5.2 times)

- a16z (6 million vs. 21.8 million, 3.6 times)

- Sequoia (5 million vs. 17.4 million, 3.5 times)

These funds play on two tables at the same time: large-scale classic seed wheels ($5-8 million), plus highly selective super-seeds (more than $50-500 million), which bring the statistical average to heaven. The TechCrunch titles of the $100 million Seed Wheels! do not reflect everyday realities, and their typical transactions are actually four to five times smaller。

Mean mass (less than 2.5 times the price difference)

- Greylock (6.9 million vs. 13.3 million, 1.9 times)

- Founders Fund (7 million vs. 12 million, 1.7 times)

- CRV (7.5 million vs. 10.8 million, 1.4 times)

- 8VC (6.6 million vs. 8.7 million, 1.3 times)

- NEA (7 million vs. 7.4 million, 1.1 times)

The medians and averages of such funds are closely tracked and do not have the long end of a super-heavy cycle. They are deployed consistently within the $50-8 million price range, with no significant anomalies。

The two-track fund occupies the title and creates the illusion that the seed wheel has become more than $30 million in games. However, the data refuted this: even the most dual-tracked institutions, typical transactions fell steadily between $5 and $8 million. Superseeds are just long ends of distribution, not centres。

For EM, the real competitive pressure comes from the homogeneity - GC, Khosla, Bessemer, Greylock. These institutions are systematically implemented in regions of US$ 5-8 million and are not distracted by super-seeds. Two-track funds are more intimidating under the heading but less threatening in daily competition. They spend part of their time on superseed markets, which is where Em would never compete。

THE FRAGMENTATION OF SEED MARKETS HAS LITTLE TO DO WITH ABSTRACT ROUND INFLATION. WE ARE WITNESSING THE BIRTH OF TWO COMPLETELY INDEPENDENT ECOSYSTEMS UNDER THE SINGLE LABEL OF "SEED WHEELS": SUPER SEEDS (OVER US$ 2000 MILLION) BELONG TO A TWO-TRACK PLATFORM, AND TRADITIONAL SEEDS (US$ 3-8 MILLION) ARE PLACES WHERE GIANT FUNDS AND EM STILL COLLID. THE ONLY DIFFERENCE IS THAT THE NUMBER OF MULTISTAGE GIANTS CROWDED BETWEEN THE CLASSIC ZONES HAS DOUBLED。

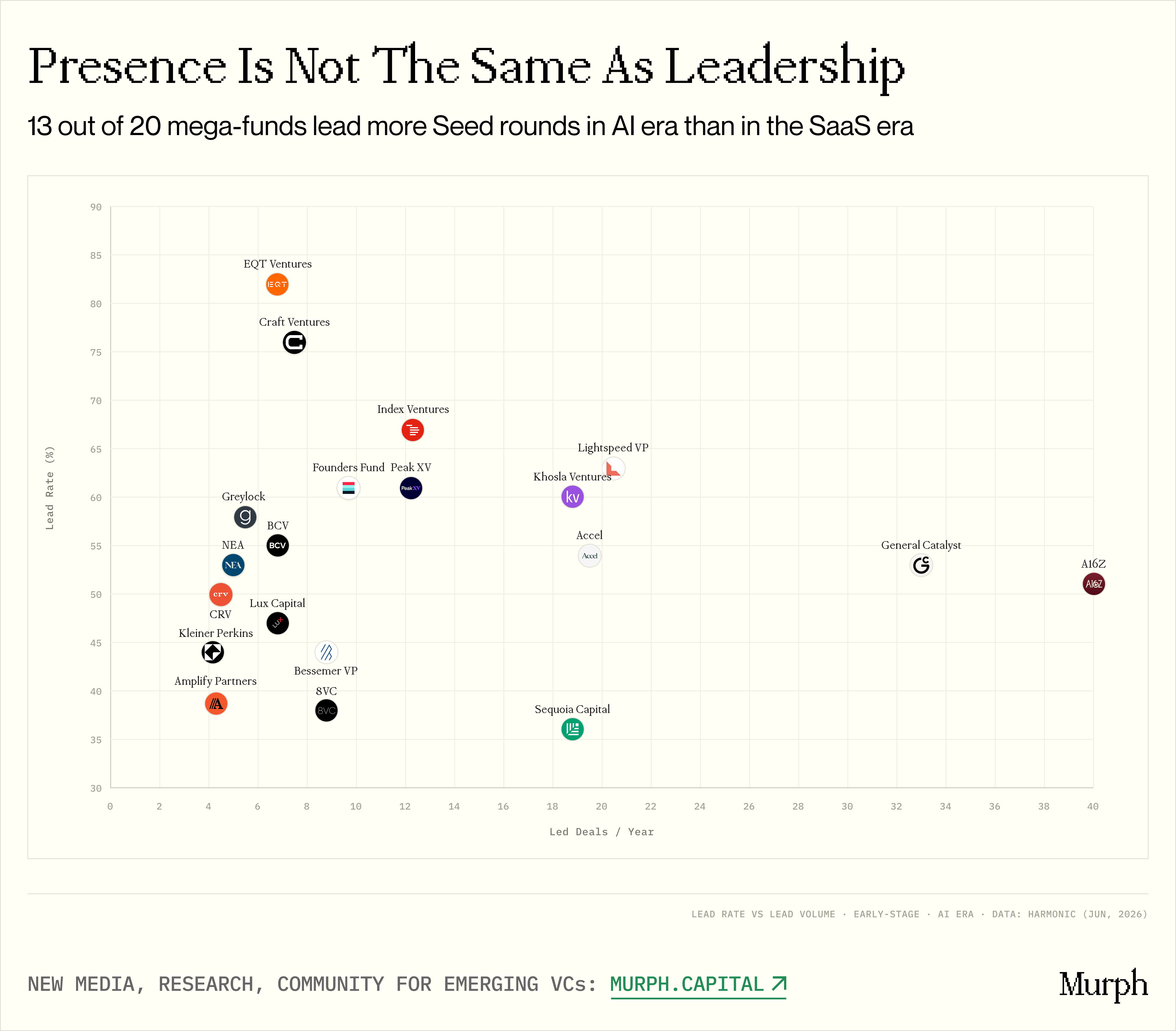

Who's pricing, who's riding

Figure: Comparison of the rates and number of investments by fund

Participation and ownership are two fundamentally different things。

A FUND INVESTED $500,000 IN A SIX-MILLION-DOLLAR ROUND OF CHECKS JUST TO FOLLOW THE INVESTORS, THE PASSENGERS ON THE SHAREHOLDERS' LISTS. IT IS THE PEOPLE WHO ARE MAKING VALUATIONS, SETTING TERMS, DECIDING WHO CAN ENTER THE JOINT VENTURE. IT WAS THE LEAD PARTY THAT FINALLY DECIDED EM AND THERE WAS NO ROOM。

So, what percentage of all seed deals implemented by mega-funds are actually awarded

I broke them down into four types:

Faith leads - High lead pitch + High trade Volume

- Khosla (60%, 19 awards/year)

- Lightseed (63%, 21 handouts/year)

- Axel (54%, 20 awards/year)

It's the most dangerous group for Em. Deployment is radical and requires a lead. Lightseed, which systematically leads early pricing, receives 21 seed wheels per year, 63 per cent. If an EM fights for the same company, it's the right to vote。

Large — high trade volume, medium lead rate

- a16z (51%, 40 awards/year)

- General Catalest (53 per cent, 33 handouts/year)

- Sequoia (36%, 19 awards/year)

THESE GIANTS DOMINATE IN ABSOLUTE LEAD, EVEN WITH LOWER PERCENTAGE LEAD. THEY LEAD THE BEST COMPANIES IN THE PIPELINE, THE REST IN PASSIVE POSITIONS. FOR EM, THERE IS A DOUBLE THREAT: EVEN IF A LARGE FUND DOES NOT TAKE OVER, ITS PRESENCE ON THE SHAREHOLDERS ' LIST CAN SERIOUSLY AFFECT SIGNAL EFFECTS AND SUBSEQUENT FINANCING DYNAMICS。

Selected lead pitch - high lead, low trade

- EQT (82 PER CENT, 7 PER YEAR)

- Craft Ventures (76 per cent, 8 cases/year)

- Index Ventures (67 per cent, 12 cases/year)

- Founders Fund (61 per cent, 10 cases/year)

- Greylock (58 per cent, 6 per year)

The majority of the transactions were carried out by these funds, but with high discipline and low speed. Driven by pure conviction: if a ticket is spent, it is almost necessary to manage this round. The overall market volume is less threatening, but in any specific transaction into which they enter, they will almost certainly take the lead。

Networking - low lead rate

- 8VC (38%,9 YEARS)

- Amplify (39%, 4 years)

- Sequoia (36%, 19 cases/year)

- Bessemer (44 per cent, 9 per year)

THESE INSTITUTIONS CHOSE TO VOTE MORE FREQUENTLY THAN THEY DID. THEIR ROLE IN THE SEED PHASE REVOLVES AROUND NETWORKS, SIGNALS AND OPTIONS, RATHER THAN ESTABLISHING MARKET PRICING. FOR EM, IT'S THE LEAST THREATENING TYPE BECAUSE THEY RARELY SQUEEZE OUT THE LEAD。

One interesting finding: two of the largest funds in terms of absolute early activity, the lowest in the AI era: a16z 51% and Sequoia 36%. And in both cases, the lead was lower than in the SaaS era (a16z from 67% and Sequoia from 52%)。

The explanation is simple: when you make 77 or 51 deals a year, it's not physically possible to win every one. Some of the transactions naturally turn to the detection of bets, joint investments with and by others. In this volume, the volume of transactions and the yield are clear trade-offs。

But in absolute numbers, they still dominate the battlefield: a16z takes 40 early deals per year, GC about 33. This is more than half of the total early transaction volume on the list combined。

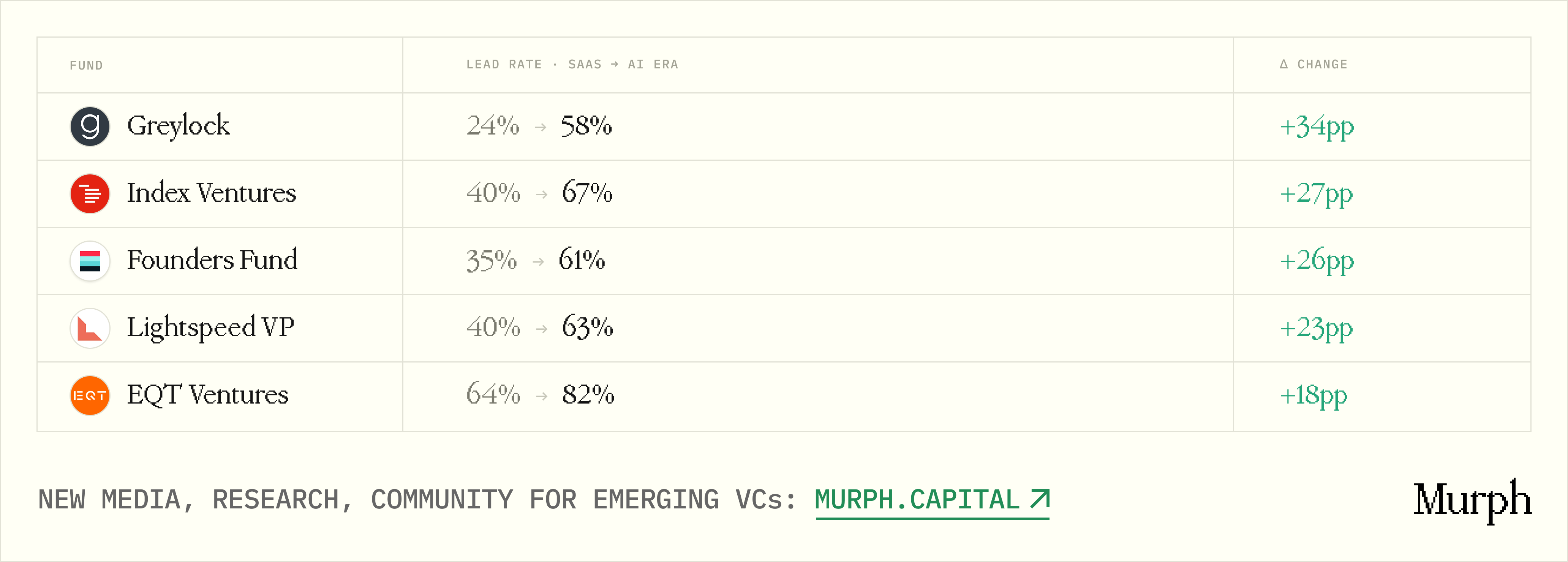

OVERALL, MOST AI-ERA FUNDS SHOW AN UPWARD TREND。13 out of 20 funds have higher AI-era investment rates than the SaaS:

Figure: Change in investment rates for funds in the SaaS era vs. AI era

Large funds are taking over more frequently. For example, Greylock, the SaaS era received only one in four seeds, and the AI era was over half. They moved from passive "invited" to active "I'll form this round."。

LP must keep this reality in mind when it comes to funds. Of course, EM likes to build up a logo of huge funds on PPT, with the addition of "we invest with xx." But this dynamic can actually serve as a key signal in defining what type of venture capital product the LP is subscribing to。

If LP asks, "How many rounds did you take last year?" How many of these rounds of other lead investors are huge funds?" If the answer is "we often invest together with a16z or GC," it is not a structural advantage, but a heavy reliance on mega-fund project flows. This is not necessarily a bad strategy, but once consideration is given to the larger rotational scale, the expansion of valuation and the diluted equity objectives resulting from a lack of pricing authority and the ability to take ownership, the bottom-up fund numbers have undergone dramatic changes。

AND IF, IN TURN, THE ANSWER IS, "WE'RE ON THE RIGHT SIDE OF A HUGE FUND, OR WE'RE HERE LONG BEFORE THEY NOTICE IT," THAT'S THE REAL, DEFENSIVE ADVANTAGE OF EM。

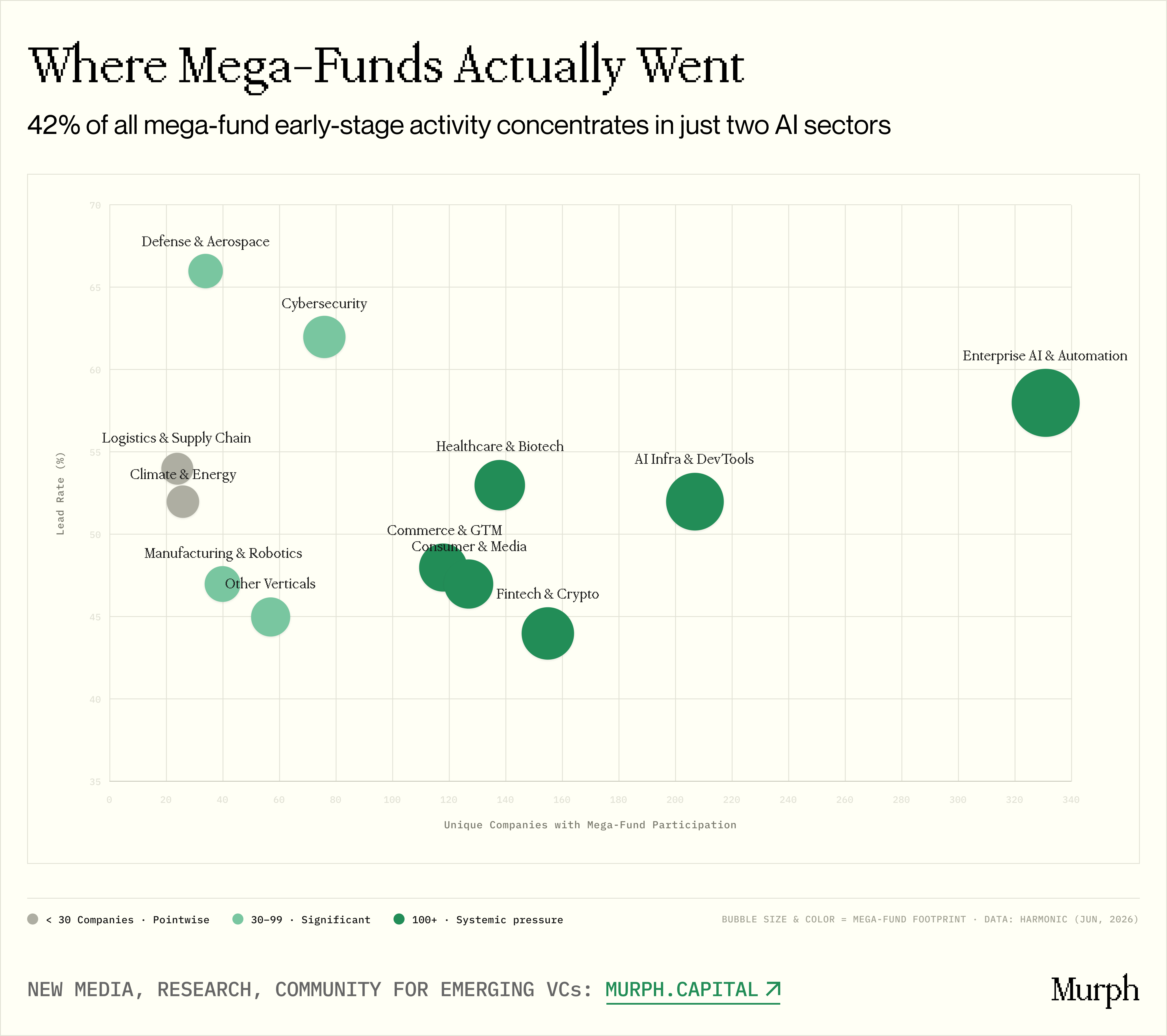

The most stressful places

Figure: Large fund early activities by track

THE ABOVE ANALYSIS OF TRADING DYNAMICS, ROUND INFLATION AND LEAD RATES DESCRIBES THE OVERALL PICTURE OF MEGA-FUNDS. BUT IN REALITY, AN EM RARELY INVESTS IN "SEEDS AS A WHOLE" AND THEY VOTE FOR A PARTICULAR TRACK, WHICH IS OFTEN THEIR CORE ADVANTAGE. SO THE NEXT LOGICAL QUESTION IS: WHERE IS THE GIANT FUND

From this perspective, their footprints are much more concentrated than the overall statistical implication。

I'm not surprisedENTERPRISE AI AND AUTOMATION, AI INFRASTRUCTURE AND DEVELOPER TOOL TRACKS LEAD THE LEAD RATE AND TOTAL NUMBER OF TRANSACTIONSi don't know. total & nbsp;538 companies, 42% of all early activity of the entire data setI don't know. Twenty mega-funds are all active in both tracks. There are three core drivers behind this:

Market size。 The cost of generating AI rose sharply from $1.7 billion in 2023 to $37 billion in 2025, a sharp increase of more than 20 times in two years. Enterprise AI already occupies 6 per cent of the global SaaS market, expanding faster than any software category in history。

Speed。& nbsp; AI is unprecedented in time dynamics. The growth model of the SaaS era is T2D3 (twice, triple, double, double), and the growth framework of the top AI primary company is Q2T3 (twice, four times, three times, three times). For the Fund, entry windows for the seed phase are closed faster. Reticent 12-18 months may mean missing the entire software class。

Performance anomalies。 Loveable reached $100 million ARR in eight months and doubled to $200 million in four months, exceeding OpenAI, Cursor and all other software companies in history. By May 2026, Sacra estimated that the annualized income of Loveable had exceeded $500 million. Cursor's estimate was $2.3 billion. Anthropic's annualized income accelerated from approximately $1 billion at the end of 2024 to $14 billion in February 2026, $30 billion in April and $47 billion in May, and absorbed $65 billion at $965 billion. All of these companies were either non-existent or completely invisible three years ago。

For AI's Em, that means almost every giant fund is hunting in your backyard. Infinite capital at hand, these giants are not subject to rotational pricing and can take over and maximize equity objectives. The survival of the new fund manager depends on in-depth field expertise, exclusive access to the network of high-density founders, and the ability of the founders to place a bet at a stage where they do not even have a pitch deck。

Another key detail is that the fastest-growing AI company (the so-called "AI Supernova") has an average Māori rate of only about 25 per cent, deliberately sacrificing unit economics for market share. The more traditional meteorite average is only about 60%, still well below the classic SaaS 70-85% benchmark。

THIS MEANS THAT THE COMPANY AI IS CURRENTLY A RACE TRACK WHERE REVENUE IS GROWING FAR BEYOND PROFITABILITY. INVESTORS ESSENTIALLY SUBSCRIBE TO FUTURE ECONOMICS RATHER THAN CURRENT PROFIT MARGINS. LARGE-SCALE FUNDS CAN EASILY WITHSTAND THIS STRUCTURAL BET WITH DEEP POCKETS AND LONG DURATION. BUT AN EM THAT MANAGES A $25-75 MILLION TOOL, IF UNIT ECONOMICS IN THE FUTURE DELIVERS LONGER THAN THE MARKET EXPECTS, IT WILL BECOME FUNDAMENTALLY VULNERABLE。

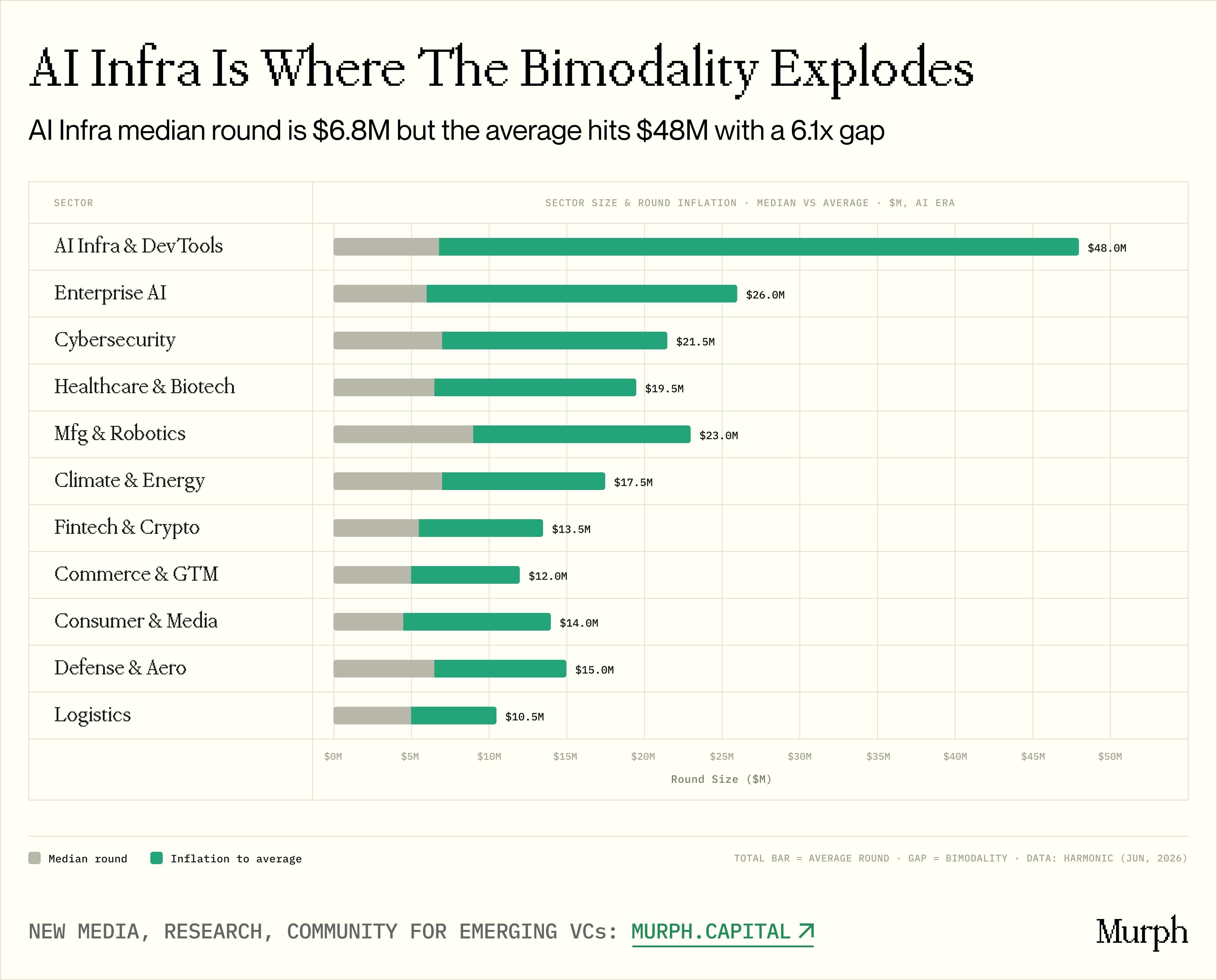

figure: median number of rounds in size of tracks vs. average

AI INFRASTRUCTURE AND DEVELOPER TOOLThe rotational structure deserves special attention. The two-track behaviour observed at the Fund level was most acute in this track:Medium rotation $6.8 million, average of $48 million7 times the difference。

This large margin indicates that the track is filled with over $100 million of superseeds, raising the statistical average. This is the hotbed of the 50 million-dollar seed wheel heading, which creates a highly distorted and typical trading image for bystanders。

In contrast, the price difference for Comerce & GTM is only 1.4 times and Healthcare 2.0 times. The further away from the AI core, the more equal the rotational pattern。

The conduct of the two tracks was disproportionate to the actual size:

Cybersecurity:& nbsp; only 76 companies, but with a high rate of & nbsp;62 per centthe highest of all major tracks. & nbsp;Medium rotation of $7 million(One of the highest data concentrations) large funds dominate pricing in nearly two thirds of transactions。

Defence and aerospace: smaller footprint (34 companies), but a record 66%i don't know. but & nbsp;Only 12 of the 20 mega-funds are activeThis means that a small number of high-faith players have focused their bets rather than systemic pressure at the platform level。

Some of the tracks are relatively uncrowded:Climate and energy(26 companies, 12 active funds)Logistics(24 companies, 13 active foundations) and traditional tracks such as PropTech, EdTech, Legal, HR。

EM, WITH DEEP EXPERTISE IN THESE TRACKS, COMPLETELY ESCAPED THE PLATFORM. THE OPPONENT IS NOT 20 LARGE PLATFORMS, BUT 8-12 INSTITUTIONS, PRICING 2-3 TRANSACTIONS PER YEAR, COMPLETELY DIFFERENT GAMES。

THIS IS AN IMPORTANT PRACTICAL REVELATION FOR THE LP: THE CORRECT INTERPRETATION OF THE EM QUESTION HAS TO TURN TO THE SPECIFIC COURSE IN WHICH THEY ARE INVOLVED, BECAUSE THE CHOICE OF THE COURSE DETERMINES THE NATURE OF THE COMPETITION AND WHAT KIND OF DIFFERENTIATION IS REQUIRED TO WIN。

Is this a premium on the seed rotation of a giant fund

Figure: Mega-fund support vs. Market-wide seed rotation to B rotation rate

SO FAR, THE WHOLE STUDY HAS SHOWN ONLY ONE SIDE OF THE COIN: THE GIANT FUND HAS INVADED THE SEED SHIP, DOING MORE TRADING, TAKING MORE FREQUENT INVESTMENTS, OPERATING IN THE PRICE RANGE OF EM。

But there's one question that we've pushed to the present, and it's probably the most critical question of the whole study: is this really working

Yes, mega-funds write larger cheques, participate 4.4 times larger than the median in the market, direct 40-50 per cent of their transactions early and take over half of the seed trade. But if their company survival rate at the seed stage is not higher than the market average, then all we paint is valuation expansion, with no real value。

IN TURN, IF A LARGE FUND-SUPPORTED SEED COMPANY MOVES TO ROUND B SIGNIFICANTLY HIGHER THAN THE MARKET, THE NARRATIVE TURNS AROUND. IN THAT SCENARIO, MEGA-FUNDS ARE NOT JUST TAKING OVER SEED WHEELS, BUT MAKING THEM BETTER. LP SHOULD ASK: "WHY NOT CONCENTRATE CAPITAL ON LARGE-SCALE SEED-COVERED FUNDS AND DOUBLE IT IN SUBSEQUENT ROUNDS TO CAPTURE THE ENTIRE MARKET LIFE CYCLE IN ONE INSTITUTION?"

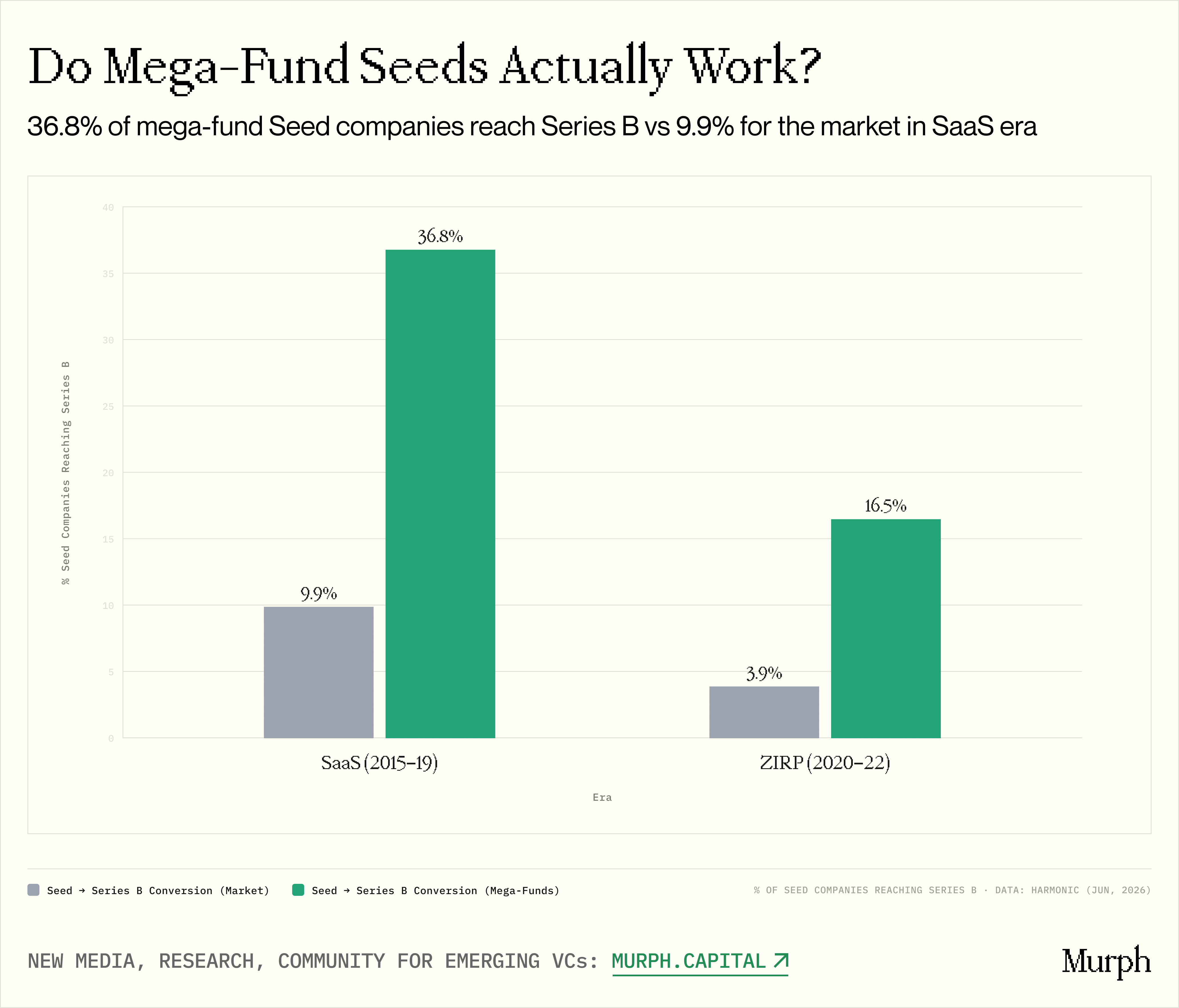

FOR THAT REASON, WE HAVE CALCULATED A STRAIGHTFORWARD TARGET: WHAT PROPORTION OF COMPANIES THAT HAVE INTEGRATED SEED WHEELS AT A GIVEN TIME HAVE COME TO ROUND B? TWO SETS OF COMPARISONS:Market as a whole& nbsp; vs. & nbsp;There's at least one large fund seed company on the shareholders' listI don't know。

We focus on the SaaS era and the zero interest rate age (the AI age companies are too young). The results are clear but nuanced。

- SaaS age:of the 60,110 companies that have integrated seeds9.8% WENT TO ROUND BI don't know. There are 940 families with huge fundsThat's 36.7%, 3.7 timesI don't know。

- Zero interest rate age:& nbsp; trend:Market 3.9 per cent, mega-funds 16.5 per cent, and gap increased to 4.2 timesI don't know。

THE ABILITY OF MEGA-FUNDS TO CONVERT SEED WHEELS INTO B IS 3.7-4.2 TIMES HIGHER THAN THE MARKET AVERAGE. MORE IMPORTANTLY, THE GAP IS WIDENING. THE QUALITY SCREENING OF MEGA-FUNDS HAS BECOME MORE VALUABLE IN AN OVERHEATING ENVIRONMENT IN WHICH MARKET-WIDE CONVERSION RATES FELL SHARPLY IN THE ERA OF ZERO INTEREST RATES。

But before we conclude, we have to dismantle why the conversion rate is so high. There are several structural drivers that can be collectively described as powerful signal effects:

- ELITE A WHEEL PROJECT STREAM:& nbsp; Top A Round Investors Actively Seek Investment with Institutional, Heavy Seed Recipients

- Internal and investment capability: mega-funds have deep pockets to buy A or B from within their seed portfolio

- Brand-driven talent acquisition:& nbsp; Top Engineers have seen labels for "Sequoia investment" or "a16z investment" with significant reductions in recruitment friction

- Media distribution advantages: Larger PR Leveraging leads to more active contacts with potential business clients

IT IS THEREFORE IMPORTANT TO RECOGNIZE THAT A LARGE PART OF THE CONVERSION RATE IS NOT THE RESULT OF THE "RIGHT" OF A LARGE FUND, BUT OF A LARGE FUND THAT HELPS COMPANIES BECOME THE RIGHT CHOICE. FOR LP, THIS IS A CLEAR SIGNAL: THE VALUE ADDED BY MEGA-FUNDS IN THE SEED PHASE IS NOT JUST "SELECTION SHARES," BUT THE REAL "PLATFORM OR PRODUCT"。

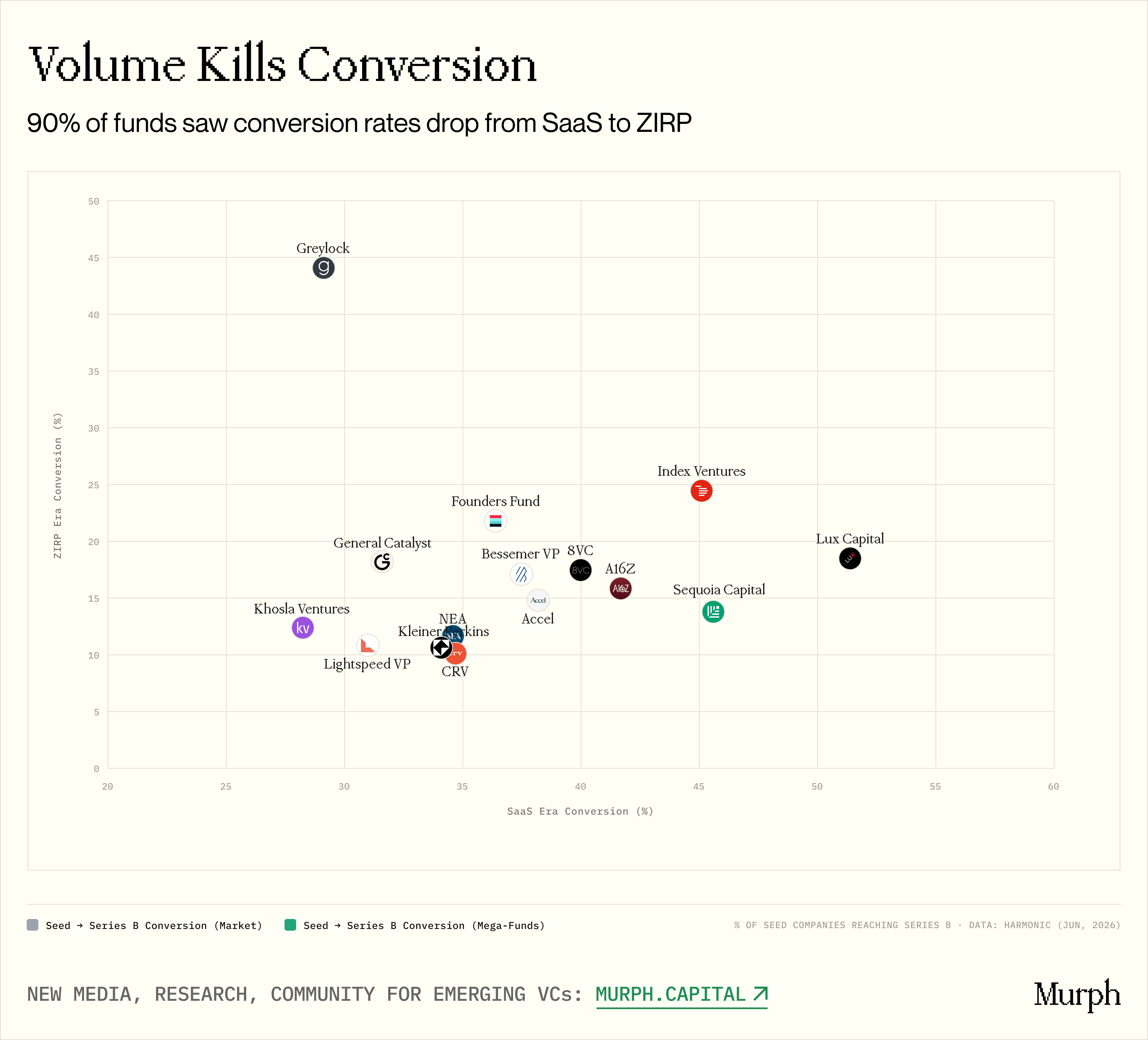

Figure: Seeds from the era of SaaS vs. the era of zero interest rates to B rotation rate

But there's another side to the coin. As we go beyond aggregate data and look at each institution, a disturbing pattern emerges: 15 of the funds (more than 10 seeds per age) with sufficient sample size14 people have gone down from Saas to zero interest rateI don't know. Decline in 10 to 25 percentage points:

- Lux: 51% → 19%

- Sequoia: 46% → 14%

- a16z: 42% → 16%

- Index: 45% → 25%

Direct relevance: The most volatile fund in the era of zero interest rates, and the worst decline in conversion rates. Sequoia tripled the volume of transactions (20 to about 50 per year) and the conversion rate fell from 46 to 14 per cent. Lightspeed was applied four times (12 to 42 times per year), and the conversion rate fell from 31% to 11%。

The only exception is Greylock, and instead the conversion rate jumped from 29% to 44%. Not by chance: Greylock is the only institution that has kept the volume of transactions almost flat in the era of zero interest rates (11.0 to 11.3 per year). Fewer deals produce higher hits. Trade volume discipline is directly equivalent to portfolio quality。

This set of conversion data simultaneously validates and complicates our entire narrative。

ON THE ONE HAND, IT PROVES THAT MEGA-FUNDS DO PRODUCE TANGIBLE RESULTS IN THE SEED PHASE. 3.7 THE MULTIPLE CONVERSION RATE PREMIUM IS NEITHER ACCIDENTAL NOR FALSE. EARLY COMPANIES SUPPORTED BY MEGA-FUNDS DO SURVIVE AND GROW BETTER. IT IS A STRONG ARGUMENT FOR LP THAT BRANDS, NETWORKS AND PLATFORM RESOURCES BRING MEASURABLE VALUE。

ON THE OTHER HAND, THE VOLUME AND QUALITY OF TRANSACTIONS REMAIN IN TENSION. TODAY, IN THE AI ERA, THE SEED TRADE OF MEGA-FUNDS IS BREAKING RECORD. IF THE PATTERN OF ZERO INTEREST RATES WERE REPEATED, CONVERSION RATES WOULD INEVITABLY BE ERODED. THE ONLY QUESTION IS HOW MUCH IS ERODED. AI ARE THE PLATFORM EFFECTS AND SIGNAL ADVANTAGES OF THE TIMES OF THESE GIANTS SUFFICIENT TO OFFSET THE DILUTION OF THE PACE OF MASS DEPLOYMENT

There will be definitive answers after 3-5 years. But historical data provide a sober warning: mega-funds have proven that they can win with low trade volumes. They have yet to prove that this can be done on a scale。

IT IS IN THIS GAP — BETWEEN THE PROVEN PAST AND THE UNVERIFIED PRESENT — THAT THE REAL CHANCE OF GETTING READY TO DO LESS BUT DO BETTER EM EXISTS。

Risk index

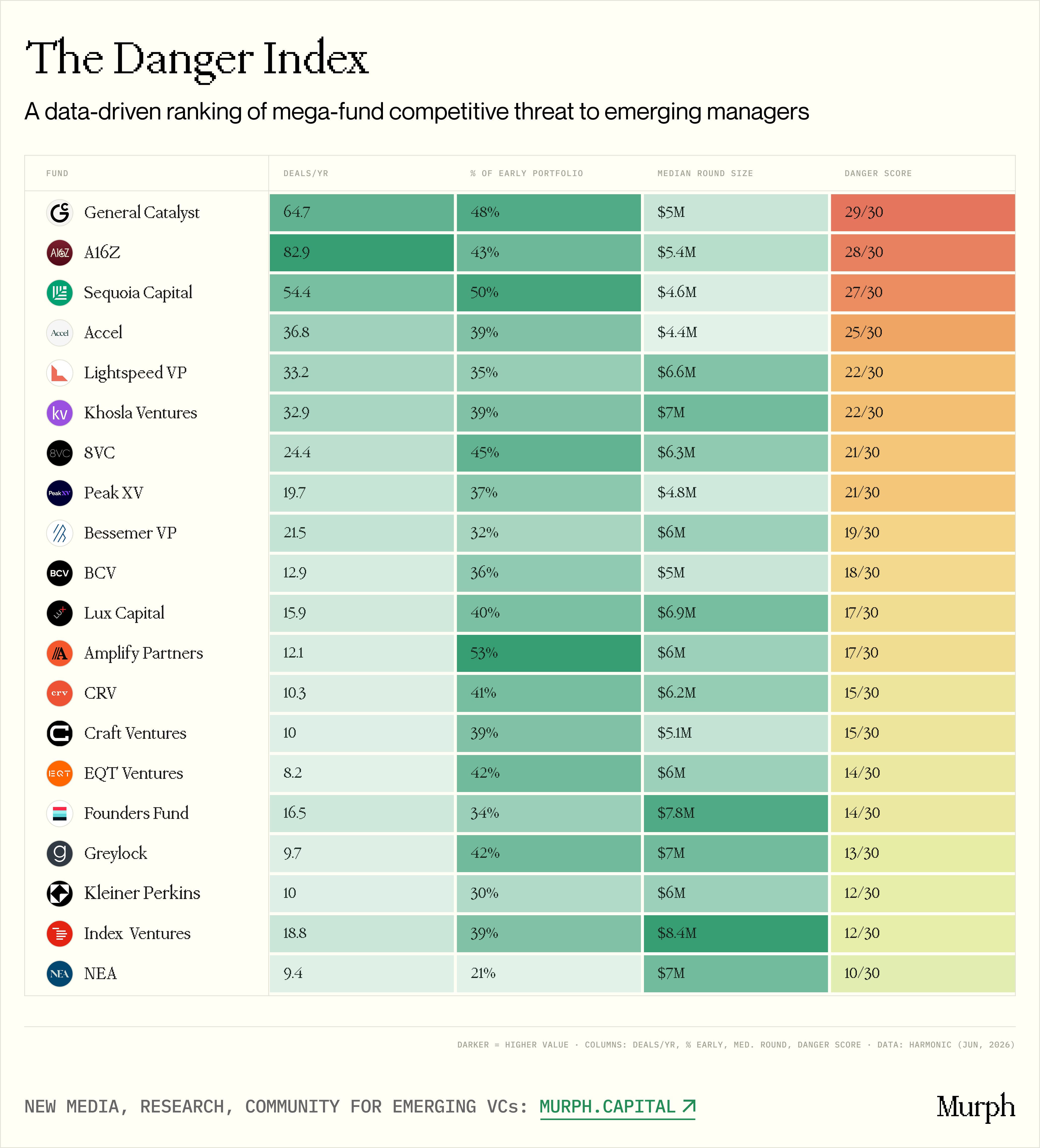

Figure 20 Risk index ranking of large funds for emerging managers

In conclusion, we did a controversial thing: we built a risk index。

THIS IS A DATA-BASED RANKING THAT MEASURES WHICH MEGA-FUNDS POSE A REAL COMPETITIVE THREAT TO EM. WE ANCHOR THREE PILLARS:

Volume of transactions: Number of transactions of an absolute early age. The higher it gets, the more EM hits them in practice。

Strategic commitments: % of total fund investment activities at an early stage. forty-five per cent indicates that this is a core strategy with dedicated teams and institutionalized processes. 20 per cent, indicating that it is a by-product and that the fund may be reduced at any time to a later stage。

Price overlap: Medium scale of participation of the Fund. This may be the most critical factor. In the 8-10 million-dollar rotation, large funds competed mainly with other multistage giants. But huge funds operating between $4-50 million, directly competing with EM -- this is the sweet zone where $50-100 million seed money deploys capital。

Each factor is 0-10 points, and the final hazard score is three points, full of 30。

The result was unexpected. Four agencies fell into the first tier (the greatest threat):General Catallyst, a16z, Sequoia and AckelI don't know。

- THESE FOUR UNITS SIMULTANEOUSLY COMPLETE 37-83 EARLY TRANSACTIONS EACH YEAR, ASSIGNING 39-50 PER CENT OF TOTAL INVESTMENT ACTIVITY TO THE SEED PHASE AND OPERATING BETWEEN THE US$ 4.4-54 MILLION ROTATIONAL SUBSECTORS - DIRECTLY HIT EM TERRITORY。

- Intuitively, GC ranks ahead of a16z, although a16z has a higher absolute volume of transactions (83 vs. 65). The difference is that GC is perfectly synchronized with three risk vectors: high speed, the highest early deployment ratio of this ladder (48 per cent), and a median rotation of $5 million - just at the centre of EM pricing sweet areas. a16z is slightly higher (5.4 million median) and early concentration is slightly lower (43 per cent). The gap is delicate but statistically meaningful。

- Sequoia's third place was unexpected. It's the lowest of the top five funds (36 per cent), and it's far ahead of the pitch. But the middle wheel was only $4.6 million - the lowest of the large platforms. It systematically buys cheaper wheels (measured by mega-funds)。

- On the contrary, Index Ventures unexpectedly fell down to the third stage, despite maintaining an annual lead rate of 19 and 66 per cent. Reason? Medium rotation of $8.4 million. Index operates entirely above the traditional Em zone。

- The same structural logic applies to the Foundations Fund (7.8 million medians) and Greylock (7 million medians), all firmly on the third stage. They have clear early footprints, but they don't fit into most EMs for survival price ecology。

THE DANGER INDEX IS NOT AN EM DEATH SENTENCE. WE SEE IT AS A MAP OF MINED AREAS。

It condensed the entire macro study into a high-risk issue of integrity: "What is the platform of the First Plateau hunting in your exact price range and track?"

If the answer is "GC and a16z, both of them are in AI software, both of them are in four to six million rotations," then EM has to make it clear to LP: What concrete advantage is it that you can win two institutions that make 150 seeds in your backyard each year

If the answer is, "Without the first team of giants, I'll take the $2-3 million climate technology," it's a completely different conversation. The risk index shows that institutional pressure on that track is structurally lower and that deep-field expertise can itself serve as a highly defensive advantage。

Core elements

- On average, mega-funds increased from 10.6 early transactions per year in the SaaS era to 23.9 in the AI era. There are only 3 smaller families. This is structural change, not cyclical。

- SEED WHEEL VALUATIONS ARE SHARPLY DIFFERENTIATED. THE 90TH PERCENTILE OF Q1 IN 2026 REACHED $93.7 MILLION, NEARLY DOUBLING IN FOUR YEARS. THE 25TH PERCENTILE ROSE ONLY FROM 18 MILLION TO $22.7 MILLION OVER THE SAME PERIOD。

- THE MEDIAN NUMBER OF SEED WHEELS WITH MEGA-FUNDS IN AI WAS $6.2 MILLION, THE MARKET AS A WHOLE WAS $1.4 MILLION, AND THE GAP OF 4.4 TIMES REMAINED STABLE IN THREE TIMES。

- Of the 20 funds, 16, the early AI-era allocation was at an all-time high. Typical mega-funds rose from 20-30% in the SaaS era to 35-50% today。

- Thirteen of the 20 funds now have more seed wheels than in the SaaS era. Greylock went from 24% to 58%. Passivity and attitude are being replaced by structured lead。

- 42% OF THE EARLY ACTIVITIES OF THE MEGA-FUND WERE CONCENTRATED ON TWO TRACKS: ENTERPRISE AI AND AUTOMATION, AND AI INFRASTRUCTURE AND DEVELOPER TOOL. ALL 20 FUNDS ARE ACTIVE ON BOTH TRACKS。

- The ratio of seed companies supported by mega-funds to round B is 3.7-4.2 times greater than the market as a whole. But of the 15 funds with a sufficient sample, 14 experienced a sharp drop in conversion rates from SaaS to zero interest rates — the biggest drop was precisely the best。

- Greylock, the only fund that has actually increased its conversion rate, kept its trade volume even in the era of zero interest rates. Trade volume discipline is equivalent to portfolio quality。

- The Hazard Index includes GC, a16z, Sequoia and Accel in the first tier - the only four funds that simultaneously meet high speed, 39-50% early configuration and below the median rotation of $5.5 million, falling directly in the EM ' s price-fixing sweet zone。

- The traditional tracks of climate and energy, logistics, PropTech and EdTech remain structurally uncrowded. – There are only 8-13 mega-funds active (20 AI tracks), with a much lower rate of participation than the average of the product。

Conclusions

The invasion of early markets by mega-funds is not a temporary anomaly of a technology cycle, but a permanent recalibration of the operating methods at the bottom of the venture capital。

As multi-stage giants continue to absorb tens of billions of dollars in the head of seed ecology, they attempt to defeat them in their high-speed, deep- pocket games as a mathematical dead end. However, the data reveal a critical crack in their seemingly perfect armour — the inescapable tension between large-scale deployment and the quality of portfolio transformation。

IN THE AI ERA, EM'S REAL ADVANTAGE IS NO LONGER TO TRY TO BE A BIG INSTITUTIONAL TRADING MACHINE, NOR IS IT A POPULAR CATEGORY FOR BLINDLY CHASING THE FIRST STAGE PLATFORM FOR PRICING RULES. RATHER, IT IS STRICT DISCIPLINE IN THE CHOICE OF TRACKS, PATIENT BUY-OUT OF THE COMPLEX ECONOMICS OF FUTURE UNITS THAT ARE OFTEN OVERLOOKED BY MEGA-FUNDS, AND THE COURAGE TO REMAIN SMALL, FOCUSED, AND DEEP-SEATED WITH THE FOUNDERS UNTIL THE MULTI-STAGE PLATFORM HAS NOT NOTICED THEM。

IN AN INCREASINGLY PURE-SCALE WIND TO THE ECOLOGY, EM'S ULTIMATE COUNTER-MEASURE IS TO TAKE OVER THE PREMIUM OF ABSOLUTE DISCIPLINE, NOT TO MATCH THE VOLUME OF DEALS WITH GIANTS。