Wall Street re-evaluates DeFi: Why is it 40 times UNI four years

Four years of waiting is more of a test of faith than 40 times the increase。

This post is part of our special coverage Syria Protests 2011

A report from a traditional bank ignited a slightly quiet DeFi track。

Geoff Kendrick, Director of Global Digital Asset Research, Standard Chartered Bank, released the first coverage report on DEX (Driven to Centralized Exchange) Uniswap on June 15, and gave a radical projection that would set the encryption market on its side: Uniswap’s governance token UNI prices will soar about 40 times by the end of 2030, touching $100 integer levels。

AT THAT TIME, THE UNI TRANSACTION PRICE WAS ONLY ABOUT US$ 2.6。

THE UNI, ONCE MOCKED AS THE “AIR GOVERNANCE CURRENCY”, IS BEING RE-PRICING WALL STREET AS A PRODUCTIVE ASSET WITH NETWORK EFFECTS. WHILE 40 TIMES AS TEMPTING AS FAR AS THE NARRATIVE IS CONCERNED, THE JOURNEY TO THE END MAY NOT BE AN EASY ONE。

UNI 40-FOLD-GROWING WALL STREET SCRIPT: FOUR NUMBERS, ONE MAIN LINE

In the deconstructive logic of Standard Chartered Bank, Uniswap is embedded in a valuation framework of deep world integration in traditional finance and chains。

RWA CURRENCYIZATION INDEX LEVEL AMPLIFICATION (340 BILLION)

The starting point for growth is the wave of RWA (real world assets). Standard Chartered Bank predicts that the magnitude of monetized assets in the global chain will increase exponentially, from about $340 billion today to $4 trillion by the end of 2028. Capital giants such as Fidelity and BlackRock are moving traditional assets such as stocks, national debt and IMF onto block chains, where the liquidity of monetized assets expands at a much faster rate than expected by the industry。

This amounts to the construction of a larger reservoir for DeFi track: assets are stacked first, followed by financial activities such as transactions, borrowing, pledges, etc。

DeFi penetration rate (3.5%-30%) leaps up TVL (37 times)

The chaining of assets is only the first step, and dead water becomes live water. In short, only the circulation of assets into the DeFi agreement can translate into the income and value of the agreement. Standard Chartered Bank predicts that only about 3.5 per cent of current monetized assets are invested in DeFi ecology, which will rise to 30 per cent by 2030。

With the growth of primary encrypted assets and the two-wheel drive of RWA in the chain, the overall DeFi TVL (total lock value) will increase 37 times from current levels in 2030 to about $2.7 trillion。

Cost switches provide price support (40 times)

The Uniswap, which is a mobile capital camp in the chain, will be the largest beneficiary of the flood, and its token currency, UNI, will receive nearly 40 times the increase from $2.6 to $100。

THE LONG-TERM PRICE PATH GIVEN BY STANDARD CHARTERED BANK IS US$ 6.5 AT THE END OF 2026 AND US$ 2027 AT THE END OF 2028 AND US$ 40 AND US$ 65 AND US$ 100 AT THE END OF 2030。

In the past, UNI was once referred to by the market as “air coin” because of its power to govern and its lack of capacity to capture cash flows. At the end of last year, Uniswap activated the cost switch, and UNI officially entered deflation。

According to the report, on 28 December of last year, Uniswap destroyed 100 million NIs and 5 million additional NIs in one time, bringing the total supply down from 1 billion to 895 million, and the flow of supplies down to 622 million. The contraction of this supply will support UNI prices。

In addition, Uniswap incurred agreement costs of approximately $21 million. The linear relationship between the cost and the volume of the transaction means that the cost switch will automatically trigger further destruction as a tokenized asset flows into the agreement. This means that UNI is moving from a “pure governance tool” to a “productive asset with deflation properties”, which directly narrows the gap between the valuation multipliers of a listed exchange such as Uniswap and Coinbase。

And it's worth mentioning that Geoffrey Kendrick also presented in his report a vivid business analogy: Uniswap compared to YouTube, and Coinbase compared to Netflix。

- Coinbase (Netflix mode):Centralized operations, heavy asset inputs, require high capital support, upscaling and compliance require layers of filtering, expansion costs are high, and asset classes are vulnerable to restriction

- Uniswap (Youtube mode):OPEN MOBILITY POOL ARCHITECTURE, WHERE ANY USER CAN BE A “CONTENT CREATOR” (MOBILITY PROVIDER). THE PLATFORM DOES NOT HAVE TO PAY HIGH COSTS FOR ASSETS TO GO ONLINE. THE NETWORK EFFECTS AND LONG-TAILING ADVANTAGES OF SUCH AN OPEN MODEL ARE DIFFICULT TO COMPARE WITH THOSE OF THE CENTRALIZED EXCHANGE (CEX) IN SUCH CONTEXTS AS STABLE CURRENCY TRANSACTIONS, LIQUID COLLATERAL DERIVATIVES, AND NICHE COINS。

The more prosperous the bilateral effect is, it's the moat that Uniswap has been able to hold on to for a long time。

More importantly, the Bank of Slags believes that Uniswap is by no means a simple “bulk DEX application”, which is essentially an integrated market infrastructure. Once RWA is expanded, traditional financial institutions are able to “insert” assets directly into Uniswap's liquidity pool. This function is beyond the reach of traditional financial markets。

Uniswap is the traditional funding preferred interface, but is being attacked by an emerging DEX and polymer

Wall Street's long-term filter is good enough, but back to the real encryption market, the real situation of Uniswap is not as good as the linear growth reported。

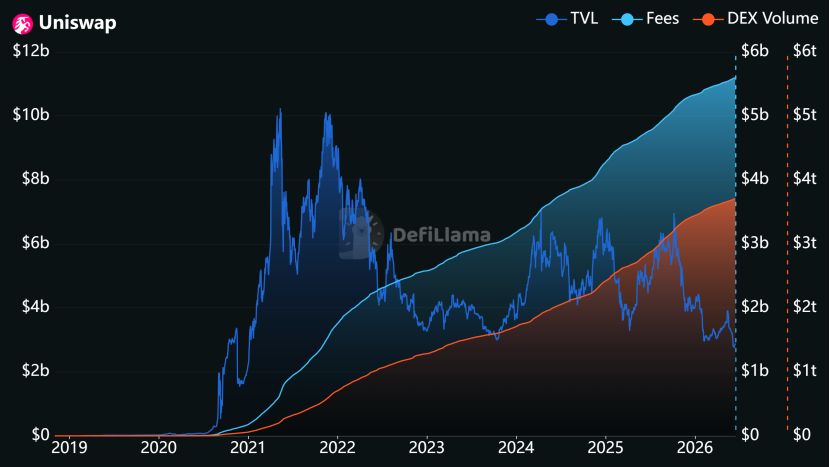

Since its inception in 2018, the cumulative volume of transactions has exceeded $3.7 trillion, with cumulative costs of $5.6 billion and TVL about $2.88 billion。

In terms of market share, Uniswap's DEX throne remains strong。Uniswap ' s trading volume and liquidity depth are dominant, with no rivals presenting a substantial threat, both in the ETA network and in the larger L2 ecology。

More important signals come from the institutional side。In February of this year, Belet's monetized money market fund, BUIDL, announced that UniswapX was on the line to provide transactions and strategically buy UNI coins. With the popularization of UniswapX, it has significantly closed the gap between the experience of DEX and CEX by introducing characteristics such as lower routers, no Gas trading, and resistance to MEV (miners can extract value), making it the preferred entry point for traditional finance。

Last Friday, June 12, Fuda deployed its stabilization currency FIDD liquidity to Uniswap. The agreement ' s centralized liquidity model is the most efficient pricing mechanism in the current chain. Once RWA assets are chained up on a large scale, Uniswap is expected to become a “news haven” in the chain, with a say in asset pricing。

Wall Street water, flowing up the chain. And Uniswap, the tap. Wall Street agencies are using Uniswap as a chain interface for compliance assets, and UNI is also moving towards the pricing logic of "link-up road infrastructure"。

Despite the enticingness of the $100 finish roll, the two major mountains on the way to the peak of Uniswap may cause this forward cheque to be substantially delayed or even frustrated。

- EMERGING DEX TRAFFIC HIJACKING WITH POLYMERS (COMPETITIVE RISK):The Solana faction, Jupiter, Raydium and others, DEX, with Meme fanaticism and extremely low transaction costs, encroached on the bulk flow. At the same time, 1inch, CowSwap, and other polymers hold users at the front end, turning Uniswap into a “back-end mobility pool” in some ecosystems, and the brand premium and the user's mentalities continue to weaken。

- Landing delays in monetization (macro-risks):Standard Chartered Bank's valuation is highly dependent on the assumption that “DeFi TVL reached $2.7 trillion in 2030”. If global legislation on monetization does not go as far as expected, or if there are large-scale security incidents, systemic risks, the rate of RWA penetration will slow significantly and the delivery cycle of this grand narrative may be seriously delayed。

RETURNING TO THE MOST INTUITIVE PRICES, UNI CURRENTLY HAS LESS THAN $3 IN TRANSACTION PRICES, DOWN BY MORE THAN 92 PER CENT FROM ITS PEAK IN MAY 2021。

The cost switch brought deflation, but no reversal of prices. The blight of the market on DeFi narratives, the depletion of liquidity and the high macro-interest rate have placed high pressure on the UNI valuation。

However, this may be the source of the “40-fold space” in the eyes of the Slags Bank: from the low base。

For the first time, Standard Chartered Bank covered UNI and offered a target price of $100, which was more windward than the price itself. In fact, it doesn't matter whether or not the prediction is accurate, but what matters is that Wall Street's perception of DeFi is changing: From the early years of the “wild growth, speculative bubbles” to rational business judgements about “capital efficiency, network effects, value of cash flows”。

It should be noted that Wall Street research tends to be longer than macro-logic but shorter than micro-risk. For the investors in it, 40 times the end point is tempting, but the road to 2030 is bound to be thorny。

WHETHER OR NOT THE UNI CAN REALLY CARRY THE $4 TRILLION IN TOKENIZATION DIVIDEND DEPENDS ON HOW WELL IT MOVES BETWEEN THE DECENTRE PRINCIPLE AND THE GLOBAL REGULATORY COMPLIANCE OF THE REAL WORLD。

Four years of waiting is more of a test of faith than 40 times。