Young Waida needs money. Why borrow $20 billion

IN WEIDA PROPOSES TO ISSUE $20 BILLION IN BONDS TO TARGET LOW-COST LONG-TERM FINANCING WITH AA RATING CREDIT。

TL;DR

• In Weida proposes to issue at least $20 billion in bonds, but it is not a lack of money: free cash flows in the most recent fiscal season are about $48.6 billion。

THE KEY IS THAT AA RATINGS ALLOW IT TO USE LONG-TERM LOW-COST DEBT TO PRE-EMPT AI CAPITAL, SUPPLY CHAIN AND ECOLOGICAL INVESTMENTS。

• ASSOCIATED TARGETS: NVDA, GOOGL, META, AMZN, AI DATA CENTRE, ELECTRICITY, OPTICAL COMMUNICATIONS, LONG-TERM INVESTMENT CLASS BONDS。

This time, Yin Weida is the easiest to misread as a simple question: Why borrow money when there is so much cash on the books

ACCORDING TO DATA FROM THE COMPANY ' S MOST RECENT FINANCIAL SEASON, AS AT 26 APRIL 2026, FY2027 Q1, THE BRITISH BATTALION HAD COLLECTED $81.6 BILLION AND HAD A FREE CASH FLOW OF ABOUT $48.6 BILLION. AT THE SAME TIME, THE COMPANY ADDED $80 BILLION IN EQUITY BUY-BACK AUTHORIZATIONS AND INCREASED QUARTERLY DIVIDENDS FROM 0.01 TO 0.25 DOLLARS. IN OTHER WORDS, IT IS NOT A COMPANY WITH A TIGHT CASH FLOW THAT NEEDS TO SURVIVE ON THE BOND MARKET。

BUT THAT IS WHY THE MARKET IS PARTICULARLY SENSITIVE TO ITS PROPOSED ISSUANCE OF AT LEAST $20 BILLION IN ADVANCED PAPER. THE BOND PERIOD COVERS 2 TO 30 YEARS AND IS USED FOR GENERAL CORPORATE PURPOSES, REFINANCING, AI DATA CENTRES AND INFRASTRUCTURE, RESEARCH AND DEVELOPMENT, SUPPLY CHAIN ADVANCES AND STRATEGIC INVESTMENTS. FOR INVESTORS, WHAT REALLY DESERVES TO BE ASKED IS NOT “IS BRITAIN RICH” BUT: WHEN AI'S BIGGEST CASH COW ALSO BEGINS TO SYSTEMATICALLY USE LONG-TERM DEBT, IS AI ENTERING A NEW PHASE IN THIS ROUND OF CAPITAL EXPENDITURE NARRATIVE

At the heart of the matter lies not in the sudden need for money, but in the fact that it is transforming its cash flow and credit rating into another capacity for expansion。

The stronger the cash, the more qualified to borrow money

The first reaction of ordinary investors to “debt-making” is often a lack of money for companies. For mature large companies, however, borrowing is often not passive, but rather proactive in choosing a cheaper and less harmful form of financing for shareholders。

The proposed issuance by Ying Weida is an advanced paper (corporate borrowing), which essentially borrows money from bond investors and pays interest and principal due. The biggest difference between it and the increase in equity is that debt does not cut out corporate ownership. As long as the future returns generated by the company are higher than the cost of debt, the original shareholders can still retain more。

This is the contrast of the deal. In the recent fiscal season, Britain has had a free cash flow of approximately $48.6 billion, and single-season cash generation capacity is significantly larger than the proposed financing. At the same time, the company is making a major buy-back and increasing dividends, which suggests that the issue of debt cannot at least be simply understood as a “cash deficit”。

A MORE LOGICAL EXPLANATION IS THAT, AT A TIME WHEN IT IS THE MOST CREDITWORTHY AND THE MARKET IS THE MOST WILLING TO LEND MONEY TO IT, YVETTE LOCKS IN A LONG-TERM FUND AHEAD OF SCHEDULE. FOR A COMPANY IN THE AI INFRASTRUCTURE EXPANSION CYCLE, DATA CENTRES, SUPPLY CHAIN ADVANCES, ECOLOGICAL INVESTMENTS AND R & D INPUTS ARE NOT SHORT-TERM PROJECTS. THEIR RETURN CYCLES MAY SPAN YEARS OR MORE. MATCHING LONG-TERM ASSETS WITH 30-YEAR OBLIGATIONS IS CLOSER TO MATURE CAPITAL MANAGEMENT THAN RELYING SOLELY ON SHORT-TERM OPERATING CASH FLOWS。

This is also the term “capital structure optimization”: companies use not only cash but also a modest mix of low-cost debt. As long as the money borrowed produces longer-term returns than interest costs, debt is not just a burden, but may also be a tool for capital efficiency。

AA RATINGS TURN BONDS INTO AI AMMUNITION

In Weida can do this if the bond market is willing to lend it at a sufficiently low cost. And the most important variable behind that is credit rating。

S&P Global Ratings recently upgraded the British Wida rating to AA for reasons such as the competitive advantage of AI demand, strong cash flow generation and robust balance sheets. AA ratings can be understood as high credit labels in bond markets: investors consider corporate default risks to be extremely low and are therefore willing to accept lower spreads and longer deadlines。

THAT IS CRUCIAL. DEBT IS NOT MERELY A “LOAN-TO-MONEY” DIMENSION, AND WHAT REALLY DETERMINES THE VALUE OF THE TRANSACTION IS “WHAT COST, HOW LONG TO BORROW, WHAT MARKET WINDOW TO BORROW”. THE BARGAINING POWER TO BORROW LONG-TERM FUNDS IS SIGNIFICANTLY ENHANCED WHEN A COMPANY IS AT A STAGE OF CREDIT ADJUSTMENT, RAPID EXPANSION OF CASH FLOWS, AND AI THEMES ARE STILL DOMINATED BY INSTITUTIONAL FUNDING。

And that explains why Ingweida acted at this point in time. It does not wait until cash flows weaken and expansion pressures increase. Rather, it reduces uncertainty about future financing ahead of time when the market best recognizes its credit quality. This is more attractive to shareholders than forcing them to finance in a worse environment in the future。

SEVERAL DIRECTIONS IN THE USE OF BOND FUNDS ALSO DESERVE TO BE SEEN TOGETHER: REFINANCING, AI DATA CENTRES AND INFRASTRUCTURE, RESEARCH AND DEVELOPMENT, SUPPLY CHAIN ADVANCES AND STRATEGIC INVESTMENTS. REFINANCING FAVOURS FINANCIAL MANAGEMENT, INFRASTRUCTURE AND SUPPLY CHAIN EXPANSION SAFEGUARDS, AND STRATEGIC INVESTMENT FAVOURS ECOLOGICAL LAYOUT. TOGETHER, THEY POINT TO THE FACT THAT THE CAPITAL NEEDS OF INGWEIDA ARE NO LONGER JUST AS SIMPLE AS "MANUFACTURING MORE CHIPS" BUT RATHER MAINTAIN THEIR POSITION IN THE WHOLE AI ECOLOGY。

YOUNG WAIDA SELLS THE CORE OF THE AI ERA AS A CALCULATOR, BUT IT ALSO NEEDS TO ENSURE THAT CLIENTS, SUPPLY CHAINS, INFRASTRUCTURE AND ECOLOGICAL PARTNERS ARE ABLE TO KEEP UP. THE MORE IMPORTANT THIS ROLE IS, THE MORE CAPITAL IS ALLOCATED TO PLATFORM COMPANIES, NOT JUST HARDWARE COMPANIES。

Borrowing is more in the interest of shareholders than selling shares

FOR NVDA SHAREHOLDERS, THERE IS ALSO A DIRECT IMPLICATION OF THIS DEBT: THE COMPANY, WHILE MAINTAINING SHAREHOLDER RETURNS, RESERVES AMMUNITION FOR LONG-TERM EXPANSION。

IN ADDITION TO ITS STRONG CASH FLOW, THE RECENT FINANCIAL SEASON OF WEIDA HAS ADDED $80 BILLION IN BUY-BACK AUTHORIZATIONS AND INCREASED DIVIDENDS. REPURCHASES AND DIVIDENDS REPRESENT THE COMPANY ' S DIRECT RETURN OF CASH TO SHAREHOLDERS; DEBT PAYMENTS REPRESENT THE COMPANY ' S USE OF EXTERNAL LONG-TERM FUNDS TO SUPPORT FUTURE INPUTS. THE TWO, TAKEN TOGETHER, ARE NOT “ONE BY ONE”, BUT RATHER THE COMPANY IS TRYING TO MAINTAIN TWO LINES AT THE SAME TIME: TO REWARD EXISTING SHAREHOLDERS WITHOUT SLOWING DOWN AI EXPANSION。

If Young Wida chooses to increase stock financing, existing shareholders will be diluted. Even if the company continues to grow in the future, each share of interest will be diluted. In contrast, the cost of debt is clearer: interest and principal. This cost is more easily managed for a company with a very high level of free cash flow and high credit ratings。

OF COURSE, THAT DOES NOT MEAN THAT DEBT MUST BE GOOD. DEBT INCREASES FIXED EXPENDITURE AND INCREASES MARKET DEMANDS FOR EFFICIENT CAPITAL ALLOCATION. YOUNG WEIDA CAN ACCEPT THE DEBT TODAY BECAUSE THE MARKET BELIEVES THAT ITS FUTURE CASH FLOW WILL COVER INTEREST AND THAT AI INFRASTRUCTURE INPUTS WILL EVENTUALLY TRANSLATE INTO INCOME AND PROFIT. IF THESE TWO PREMISES CHANGE, DEBT BECOMES A VALUATION PRESSURE FROM AN EFFICIENCY TOOL。

SO, WHAT REALLY CHANGED THIS TIME WAS THE WAY INVESTORS LOOK AT BRITAIN. IN THE PAST, THE MARKET WAS MORE CONCERNED WITH THE GROWTH OF GPU DEMAND, MĀORI AND INCOME; NOW, IT IS ALSO CONCERNED WITH THE DISTRIBUTION OF CASH FLOWS: HOW MUCH IS SPENT ON BUY-BACKS AND DIVIDENDS, HOW MUCH IS SPENT ON SUPPLY CHAINS AND INFRASTRUCTURE, HOW MUCH IS SPENT ON ECOLOGICAL INVESTMENTS AND HOW MUCH IS TARGETED IN ADVANCE THROUGH DEBT。

THIS WILL COMPLICATE THE VALUATION ANCHOR OF THE NVDA. IT IS NO LONGER JUST A “PROFIT GROWTH STORY”, BUT IT IS ALSO BEGINNING TO FEATURE “CREDIT ASSETS” AND “LONG-TERM CAPITAL ALLOCATION PLATFORMS”。

THE AI FINANCING TEMPLATE FOR LARGE TECHNOLOGY COMPANIES IS IN SHAPE

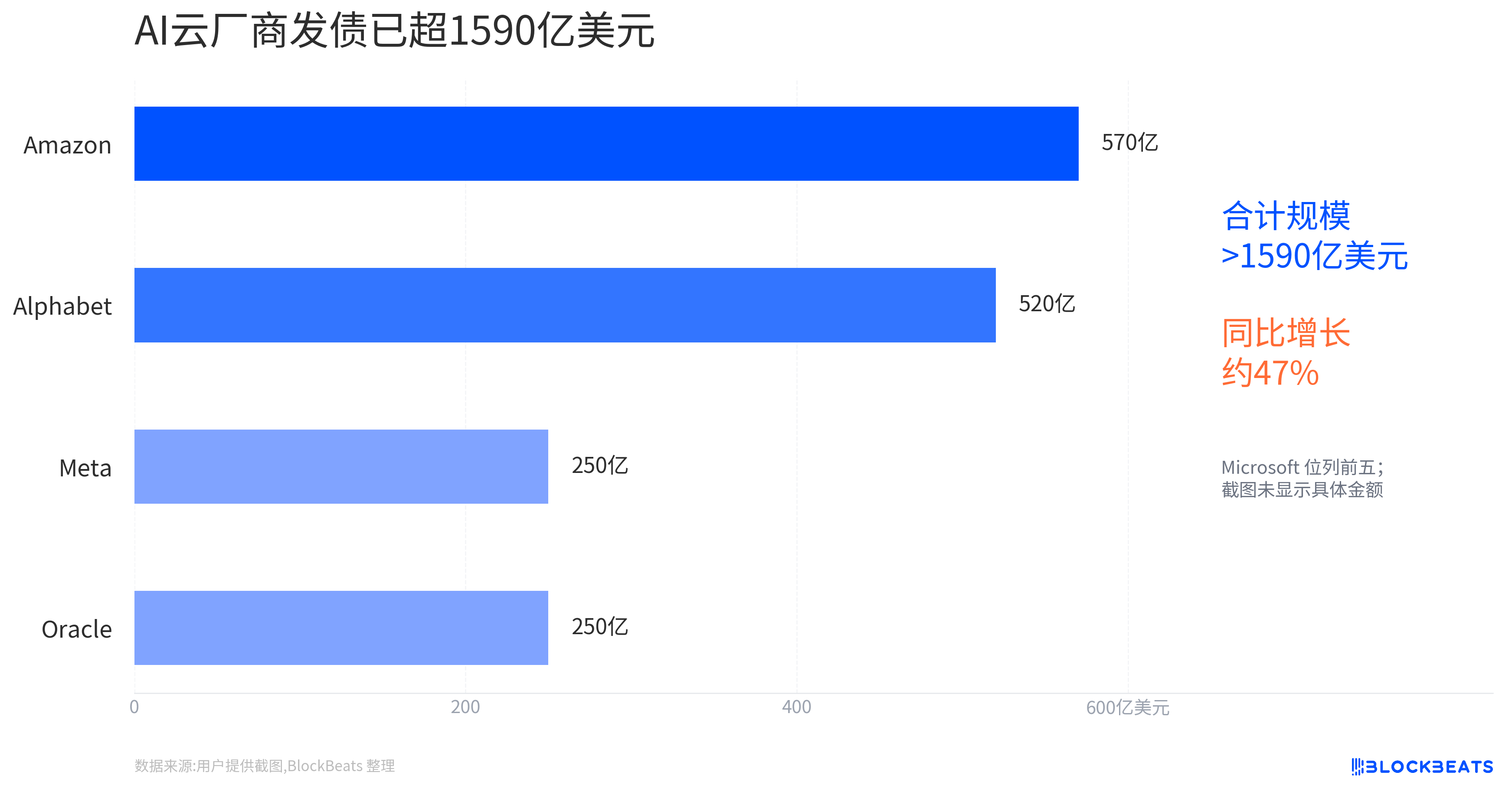

Young Waida is not the only company to do this. Alphabet completed $20 billion in bond issues in February 2026, with the same series of terms and orders reportedly exceeded $100 billion. Large technology companies, such as Meta and Amazon, also use debt financing as one of the tools to support infrastructure expenditures in AI input cycles。

THESE CASES CANNOT BE SIMPLY DESCRIBED AS “LACK OF MONEY FOR TECHNOLOGY GIANTS”. MORE PRECISELY, AI INFRASTRUCTURE HAS EVOLVED FROM A SOFTWARE GROWTH STORY OF LIGHT ASSETS TO A HEAVY ASSET CYCLE INVOLVING DATA CENTRES, ELECTRICITY, CHIPS, NETWORKS, SUPPLY CHAINS. WHICH COMPANIES HAVE ACCESS TO LOWER-COST, LONGER-TERM FINANCING CAN HAVE GREATER SWING SPACE IN THIS EXPANSION。

This has two implications for market pricing。

First, debt financing has extended the sustainability of AI Capex (capital expenditure). As long as the bond market is willing to pay, large technology companies will not have to rely entirely on current cash flows to pay for long-term construction. This supports demand expectations in the areas of data centres, electricity, light communications, semiconductor supply chains, etc。

SECOND, DEBT FINANCING WOULD ALSO MAKE INVESTORS MORE INTERESTED IN THE RETURN CYCLE. IN THE PAST, THE MARKET WAS WILLING TO PAY HIGH VALUATIONS FOR AI INPUTS BECAUSE OF THE FAST GROWTH RATE. BUT WHEN THE INVESTMENT BECOMES HEAVIER AND THE FINANCING BECOMES LONGER, THE PROBLEM BECOMES: WHEN WILL SUCH INFRASTRUCTURE YIELD SUFFICIENT RETURNS? IF AI REVENUE AT THE END OF THE APPLICATION DELIVERS SLOWER THAN EXPECTED, OR COMMERCIAL RETURNS FALL IN UNIT CAPACITY, THE MARKET WILL REVISIT WHETHER THE EXPANSION OF THESE DEBT SUPPORT IS TOO RADICAL。

THE SPECIAL THING ABOUT YVETTE IS THAT IT IS UPSTREAM OF THE AI CAPITAL EXPENDITURE CHAIN. THE MORE CLIENTS INVEST, THE BETTER IT WILL BE; BUT IF THE RETURN ON INVESTMENT ACROSS THE INDUSTRY IS CALLED INTO QUESTION, IT WILL BE DIFFICULT FOR IT TO STAY OUT OF THE WAY. AS A RESULT, THIS DEBT PAYMENT HAS STRENGTHENED BOTH MARKET RECOGNITION OF ITS CREDIT AND CASH FLOW AND HAS EMBEDDED IT DEEPER INTO THE AI LONG-TERM CAPITAL EXPENDITURE NARRATIVE。

It's a test of whether pricing and returns are set together

The most important qualification to be retained is that it remains “a minimum of $20 billion to be issued” and that the size of final issuance, interest rates, spreads and order book strength are still to be confirmed. Only when the transaction is completed will the market be able to judge more accurately how much of the money bond investors are willing to pay at a lower cost。

IF FINAL PRICING SHOWS STRONG DEMAND AND LONG-TERM SPREADS ARE KEPT LOW, IT IS FURTHER EVIDENCE THAT INGWEIDA IS TURNING AA CREDIT INTO A TOOL OF EXPANSION. IT CAN MAKE MONEY NOT ONLY FROM ITS CLIENTS' AI EXPENDITURES, BUT ALSO FINANCE ITS LONG-TERM LAYOUT ON CAPITAL MARKETS AT LOWER COST。

BUT THE MORE IMPORTANT VALIDATION IN FOLLOW-UP IS NOT IN THE BOND ITSELF, BUT IN THE NEXT PHASE OF THE FINANCIAL AND CAPITAL EXPENDITURE DATA. INVESTORS NEED TO SEE WHETHER BRITAIN WILL CONTINUE TO MAINTAIN STRONG AND FREE CASH FLOWS WHILE ADVANCING AI INFRASTRUCTURE, SUPPLY CHAIN ADVANCES, ECOLOGICAL INVESTMENT AND SHAREHOLDER RETURNS. IF THESE VARIABLES ARE COMPATIBLE, DEBT IS THE AMPLIFIER OF CAPITAL EFFICIENCY。

IN TURN, THE MARKET ' S UNDERSTANDING OF SUCH DEBT WILL CHANGE IF THE RETURN CYCLE ON AI INFRASTRUCTURE INCREASES IN THE FUTURE, OR IF COMPANIES INCREASE THEIR DEPENDENCE ON EXTERNAL FINANCING TO SUSTAIN EXPANSION. THE QUESTION THEN IS NO LONGER “IN THE ABSENCE OF MONEY”, BUT “IN THE RETURN OF AI'S LONG CYCLE OF INVESTMENT, WHETHER IT IS SUFFICIENT TO SUPPORT TODAY'S EXPECTATIONS THAT LOW-COST FINANCE WILL BE FORTHCOMING”。