Copper, 2026 gold

As long as you use the power, you can't leave the copper

Wen Qiang 6

Copper, will it become another gold of this age

In the past two years, the market has understood the AI infrastructure as a chip story. NVIDIA ' s GPU, TSM ' s capacity, HBM ' s good rate, CoWOS ' cover bottlenecks, almost all of the discussions revolve around silicone. But AI data centres don't buy GPU back and plug in and run. It also requires grid access, transformers, master cells, cables, liquid cooling systems, fibre-optic interconnections and large quantities of metals。

In the last one"THE GREAT FAMINE" OF OPTICAL AND COPPERWE'VE TALKED ABOUT ONE THING: AI'S NEED IS SINKING FROM CHIPS DOWN TO FIBER-OPTICS AND COPPER。

This article continues to talk in depth about copper narrative changes during the year. Why does the market think copper is getting like gold? Why did macro money start buying copper? Why are mining companies and commodity traders saying "copper is not enough"? Why is it no longer just the industrial metal used to judge the economic cycle

Dr. Cooper is not just a microcosm of the manufacturing cycle

There's an old saying in the English financial market, Dr. Copper, that the Chinese financial media sometimes translates "Dr. Copper." The name means that copper prices are like an ecologist who can diagnose global warming in advance。

The price of copper cannot be separated from manufacturing. In China, where much of the property is being built, manufacturing stock is being replenished and domestic electricity, cars, cables and pipes are in demand, copper prices rise. The cycle goes down, the copper goes down. Copper prices are in essence a microcosm of Chinese real estate, global manufacturing and trade cycles。

BUT TODAY THERE ARE NEW IMPACT VARIABLES FOR COPPER DEMAND: AI DATA CENTRES, GRID EXPANSION, NEW ENERGY VEHICLES, ENERGY RESERVES, MILITARY INDUSTRY, AND RE-INDUSTRIALIZATION ARE INCREASING THE STRUCTURAL DEMAND FOR COPPER。

As long as you have electricity, you can't leave copper。

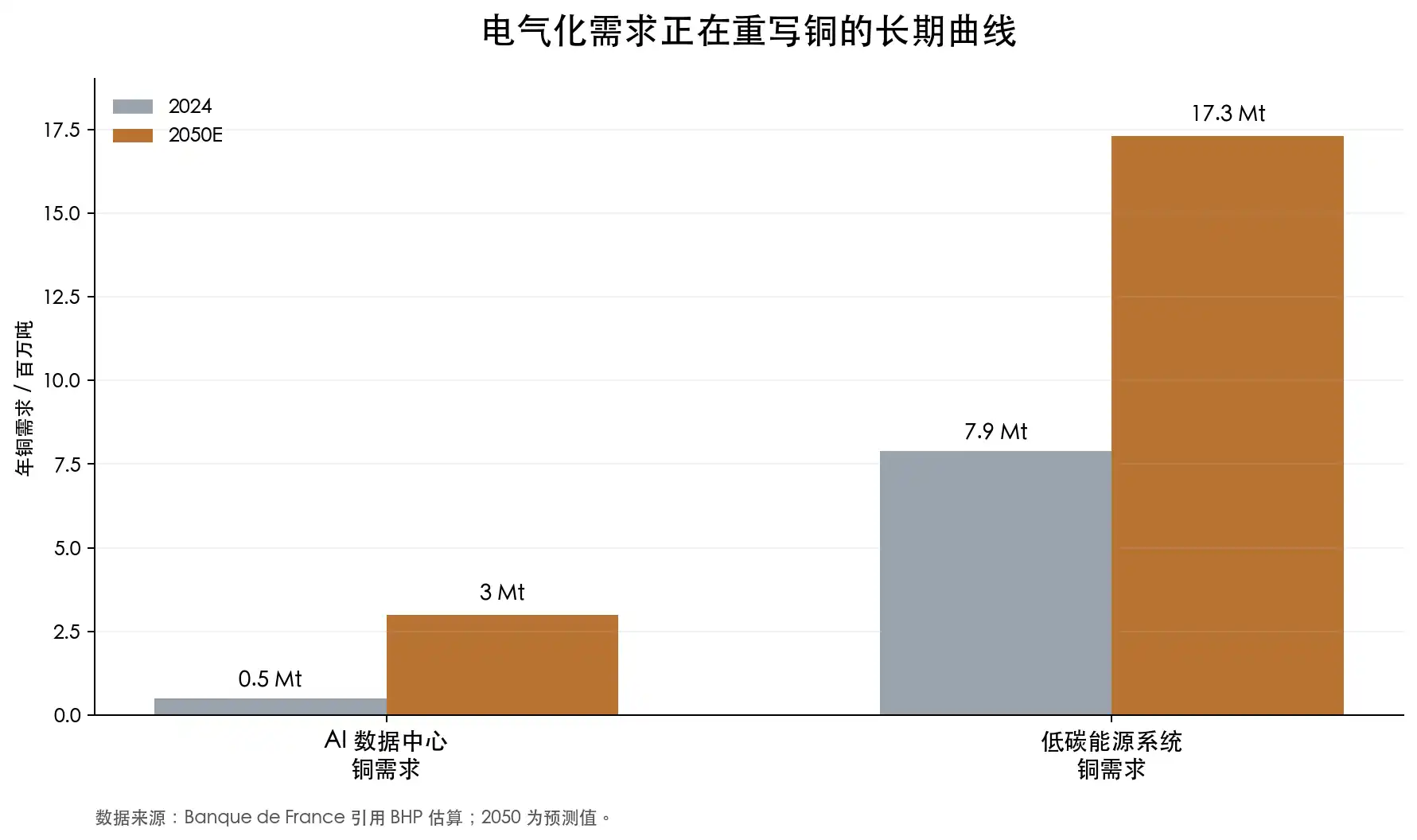

Banque de France quoted BHP in an analysis of the AI data centre and the copper market: the demand for copper in the AI data centre could grow from about 500,000 tons in 2024 to about 3 million tons in 2050. During the same period, demand for copper for low-carbon energy systems may have risen from 7.9 million tons to 17.3 million tons. The article also cites a specific case: the construction of the Microsoft Chicago data centre consumed 2177 tons of copper。

THIS FIGURE ALONE IS NOT PARTICULARLY LARGE IN THE GLOBAL COPPER MARKET. THE FOCUS, HOWEVER, IS NOT ON HOW MUCH COPPER IS SPENT IN A DATA CENTRE, BUT RATHER ON THE FULL RANGE OF POWER INFRASTRUCTURE REQUIREMENTS BEHIND THE AI DATA CENTRE, RATHER THAN SINGLE-POINT DEMAND. THE CLOSER THE GPU IS, THE HIGHER THE ARCTIC POWER, THE MORE THE DATA CENTRE LOOKS LIKE A HIGH-ENERGY PLANT. FOR PLANTS TO USE ELECTRICITY, IT REQUIRES GRIDS, TRANSFORMERS, CABLES, MAIN LINES, SWITCH EQUIPMENT AND COOLING SYSTEMS。

OF COURSE, ALL THE STORIES ABOUT COPPER CANNOT BE SIMPLY ATTRIBUTED TO AI。

The CEO Richard Holtum of Trafigura, the world’s mega-commodity trade giant, warned in 2025 at LME Week that data centres and defense are indeed hot, but that the demand for copper in the next decade still comes from traditional infrastructure, construction, urbanization, and consumer goods. He also mentioned that copper for air conditioners still exceeded that for data centres in that year。

THIS PERSPECTIVE ALSO GIVES US A NEW PERSPECTIVE: THE DEMAND FOR COPPER IS NOT ONLY SUPPORTED BY AI ALONE, BUT BY THE EXPANSION OF ALMOST ALL OF THE ELECTRICITY SCENES。

The biggest cow logic of copper is that it can't get out so fast

Many people have the first impression of copper as "industrial metal" and feel that as long as prices rise, the mines dig up and the supply comes up. But that is not the case。

LARGE COPPER MINES TYPICALLY TAKE MORE THAN A DECADE FROM DISCOVERY, EXPLORATION, RESOURCE IDENTIFICATION, RESEARCHABILITY, FINANCING, LICENSING, CONSTRUCTION TO PRODUCTION. THE IEA REPORT SHOWS THAT IT TAKES AN AVERAGE OF ABOUT 17 YEARS FROM DISCOVERY TO PRODUCTION. THIS MEANS THAT IF THE MARKET SUDDENLY FINDS THAT COPPER IS NOT ENOUGH IN 2026, A TRULY LARGE NEW SUPPLY MAY NOT APPEAR IN 2028, 2029, AND MANY SUPPLIES WILL WAIT UNTIL THE 2030S。

Robert Friedland, founder and executive co-chair of the Canadian mining company Ivanhoe Mines, has repeatedly stressed this issue. He is one of the most famous coppers in the global mining ring, with a world class copper project in the Democratic Republic of the Congo, Kamoa-Kakula. His expression has been radical: the world has not yet realized how much copper it needs. For more than a decade, the world has not prepared enough new copper mines for the era of electrification。

THAT'S NOT HIS JUDGMENT ALONE. IEA DATA ALSO SUPPORT THIS DIRECTION。

THE AVERAGE GLOBAL LEVEL OF COPPER HAS DECLINED BY ABOUT 40 PER CENT SINCE 1991. DECLINING TASTE MEANS THAT MORE COPPER IS AVAILABLE FOR DIGGING A TON OF ORE IN THE PAST, AND THAT THE SAME TON OF COPPER IS NOW NEEDED FOR DIGGING MORE ORE, MORE ELECTRICITY, MORE WATER AND MORE WASTE STONES. IEA ALSO MENTIONED THAT ONLY 5% OF THE COPPER DEPOSITS DISCOVERED IN THE LAST 35 YEARS HAVE BEEN FOUND IN THE LAST 10 YEARS. NEW DISCOVERIES ARE LOW, OLD MINERALS ARE DOWNGRADED, PROJECT CONSTRUCTION CYCLES ARE LONGER AND CAPITAL SPENDING IS RISING. IEA ESTIMATES THAT, BASED ON THE CURRENT PROJECT PIPELINE, THE COPPER MARKET MAY FACE A 30 PER CENT SUPPLY GAP BY 2035。

So copper is not the type of asset that is "to come out when prices rise." Copper mining projects are increasingly like large-scale infrastructure projects: mining, licensing, community relations, water resources, environmental review and changes in tax policies in resource countries。

Chile, Peru, the Democratic Republic of the Congo, Zambia, Indonesia and Mongolia have important copper resources and different forms of political, tax, community or operational risk. The more the copper strategy, the more the resource countries are motivated to increase their share; the higher the price of copper, the easier it becomes for mining companies to face tax increases and renegotiations。

Smelting ends are also exposed to stress。

After entering the smelter, copper concentrates are processed into refined copper. The processing and refining fees charged by smelters to mines are known as TC/RC, i.e., processing charge and refining charge. Under normal circumstances, there is a sufficient supply of concentrates, a strong bargaining power of smelters and a high level of TC/RC, which falls when concentrates are strained and smelters rob raw materials。

IN 2026, AN ANOMALY WAS THAT THE PRICE OF COPPER WAS INNOVATIVE AND THE PROCESSING FEES FELL TO HISTORICAL LOWS. ACCORDING TO IEA, THE ANNUAL TC/RC BENCHMARK FOR 2026 FELL TO US$ 0 PER TON AND THE SPOT TC/RC HAS BEEN NEGATIVE SINCE 2024。

THIS IS MORE CRITICAL THAN SIMPLY LOOKING AT EXCHANGE STOCKS. BECAUSE COPPER BOTTLENECKS ARE NOT ONLY REFINED COPPER PRODUCTS, BUT ALSO MINES AND CONCENTRATES. UPPER RAW MATERIALS ARE TIGHT, AND MORE SMELTERS ARE USELESS. CHINA HAS SIGNIFICANTLY EXPANDED ITS COPPER SMELTING CAPACITY OVER THE PAST TWO DECADES, WITH IEA CLAIMING THAT CHINA ACCOUNTED FOR MORE THAN 90 PER CENT OF THE GLOBAL COPPER SMELTING PRODUCTION GROWTH SINCE 2005, AND ABOUT HALF OF GLOBAL COPPER SMELTING PRODUCTION BY 2025. THE VULNERABILITY OF THE SUPPLY CHAIN IS MAGNIFIED BY STRONG MIDSTREAM CAPACITY AND TIGHT UPSTREAM MINES。

The scarcity of gold comes from reserves, mining costs and monetary attributes. Copper, of course, is not gold, but when its new supply becomes slower, its resources become more concentrated and its strategic attributes become stronger, it also begins to have some kind of gold-like scarcity。

Why does macro finance start to like copper

Copper formerly belonged mainly to commodity traders and mineral analysts. It is also now increasingly attracting macro-finance。

Stanley Druckenmiller, for example, was one of the most famous macro investors in the United States, managing quantum funds with Soros and later creating Duquesne Family Office. He is characterized by large-cyclical, back-to-back confidence transactions, so the market is concerned about what he thinks about AI, the dollar, bonds and bulk commodities。

In a recent interview with Morgan Stanley, he mentioned that his portfolio has been driven mainly by AI in the past few years, but has now moved towards a more macro- and geopolitical positioning. He mentioned the possession of copper, the downside of the dollar and the possession of gold as a geopolitical hedge。

HIS LOGIC IS THAT LARGE COMMODITIES DENOMINATED IN UNITED STATES DOLLARS BENEFIT IF THE DOLLAR IS WEAK. THE EXPANSION OF FISCAL DEFICITS, CONTINUED GOVERNMENT INVESTMENT, RISING GEO-RISKS, AND THE PURCHASE OF GOLD. IN THE SAME CONTEXT, THE RETURN OF ELECTRICITY GRIDS, MILITARY INDUSTRIES, AI DATA CENTRES, ENERGY SYSTEMS AND MANUFACTURING WILL BRING PHYSICAL ASSET DEMAND, WITH COPPER AT THE CROSSROADS OF THESE DIRECTIONS。

Druckenmiller represents a macro-finance perspective and a more radical expression in the commodity trade。

Pierre Andurand is the most typical of them. He was the manager of a well-known European hedge fund for large commodities, trading energy in the early years, co-founding BlueGold Capital and later creating Andurand Capital. In an interview with Financial Times, he gave a very radical judgment that copper prices could run to $40000 per ton in the coming years。

Jeff Currie's point is also worth mentioning. Jeff Currie, a long-time research director for Goldman Sachs, joined Carlyle, was one of the most influential people in Wall Street’s commodity research. He has long spoken of "copper is the new oil" meaning that copper could play a fundamental resource role similar to that of oil in the old energy age. In 2024, he called copper one of his highest confidence deals。

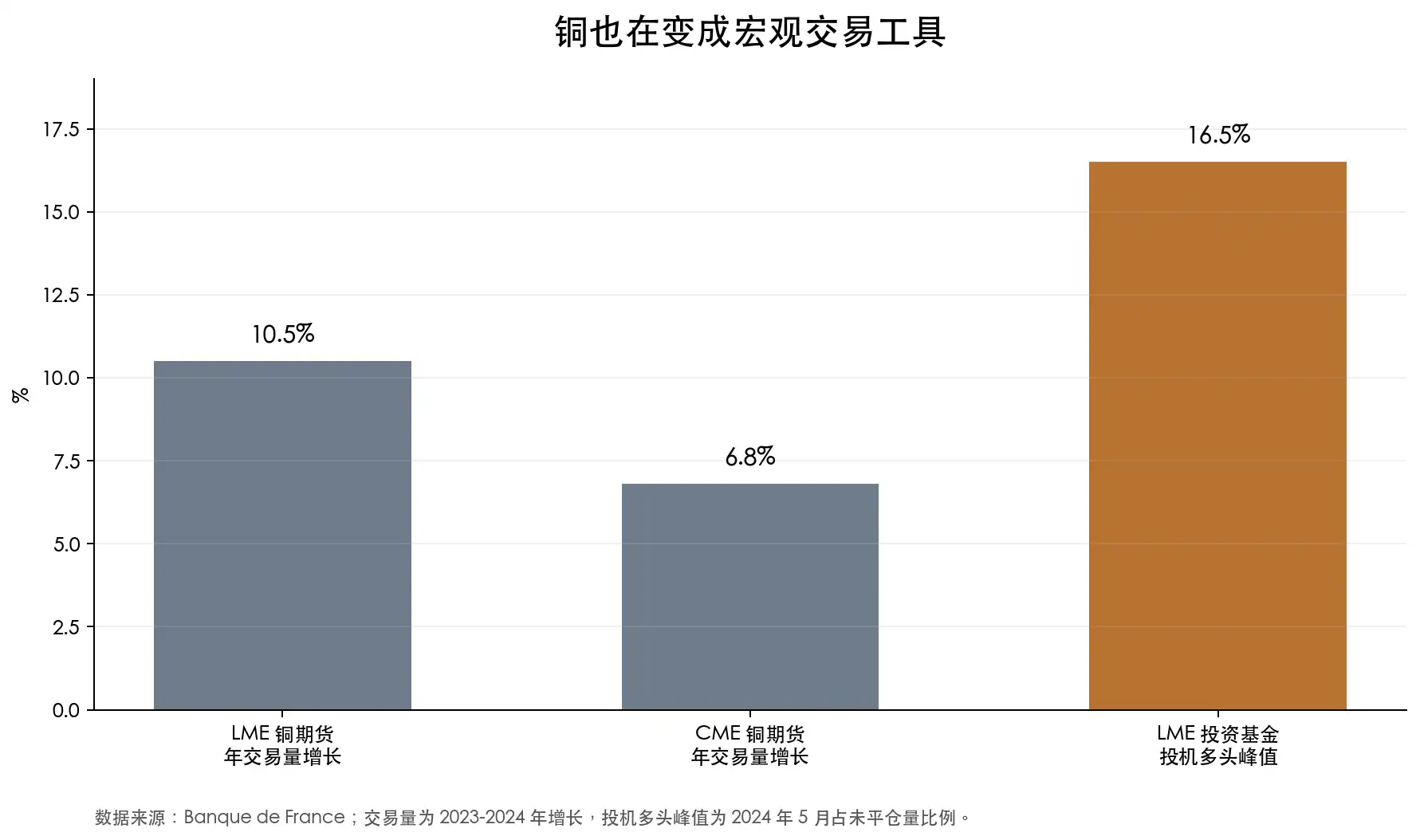

The data also show that funds are coming in。

Banque de France mentioned that, between 2023 and 2024, the annual turnover of LME copper futures increased by 10.5 per cent, the annual turnover of CME copper futures by 6.8 per cent, and that, of the LME copper futures, many investment funds speculated on 16.5 per cent of the balance in May 2024. This is not a simple physical repository, but rather a financial fund that uses copper as a macro-trading tool。

Copper mining stock: leverage of copper

Gold shares tend to increase price volatility in gold cattle. A similar amplifier properties exist in copper cattle。

The increase in copper prices is a cost pressure for end-users, but it may be an expansion of profitability for already productive mining companies. For example, the price of copper rose from $900 to $12,000 per ton, and if the cost of cash for the mine did not rise simultaneously, a significant portion of the additional $300 would enter the profit statement directly. And that is why copper stocks are naturally leveraged. The price of copper has risen for a while, and the profits of the miners may increase more; the price of copper has fallen and profits will contract faster。

The market has traded this leverage in the last two years。

In the case of Unit A, from June 2024 to June 2026, the Loyang molybdenum industry was the most typical high-flexible sample. Its core focus is on the Democratic Republic of the Congo ' s copper and cobalt assets, in particular Tenke Fungurume and KFM. The Loyenne molybdenum industry experienced an increase of approximately 129 per cent over the past two years, at a peak of close to 260 per cent, based on the crude ex-register price. This is not the performance of the ordinary cycle, but rather the re-pricing of copper resources abroad。

Companies such as the Jiangxi copper industry, the copper mausoleum, and the Yunnan copper industry are more likely to reflect fluctuations in copper prices and smelting properties. The copper sector in Jiangxi grew by about 82 per cent, with the highest increase exceeding 200 per cent; in the copper mausoleum, by approximately 77 per cent, with the highest increase of about 159 per cent; and in the Yunnan copper sector by only about 29 per cent, with the highest increase exceeding 130 per cent。

All of these stocks reflect the other side of the copper stock: when it comes, it is flexible, and when it comes back, it is violent。

LOOKING BACK FROM THE TOP, IT'S MORE INTUITIVE. THE YUNNAN COPPER INDUSTRY RETREATED BY 45 PER CENT FROM THE REGION, THE JIANGXI COPPER INDUSTRY BY 41 PER CENT AND THE LOYANG MOLYBDENUM, THE NORTHERN COPPER INDUSTRY AND THE PURPLE GOLD INDUSTRY BY MORE THAN 30 PER CENT. COPPER STOCKS ARE NOT COPPER PRICES PER SE, BUT ARE THE RESULT OF A COMBINATION OF COPPER PRICES, COSTS, INVENTORIES, TC/RC, PROJECT PROGRESS, RISK AND EQUITY MARKET SENTIMENT IN RESOURCE COUNTRIES。

In America, the most typical copper unit is Freeport-McMoRan, code FCX. It is one of the core copper producers in the United States, with assets such as Morencia in the United States, Cerro Verde in Peru and Grasberg in Indonesia. For global finance, FCX is almost one of the most common US stock tools for copper-priced openings. Marketwatch data show that on June 2, 2026, the FCX touched the 52-week height of 72.09 dollars, but on June 5, it fell by 9.07 per cent on a single day, with more than 12 per cent retreating from the heights in a few days。

Southern Cooper, code SCCO, is another representative of a high-quality copper unit. Its assets are mainly in Peru and Mexico, with high copper exposure and high profitability. IBD mentioned earlier this year that SCCO had a 55 per cent rise during the year and had a record high. Compared to FCX, SCCO is more like a more pure and profitable copper mine asset, but it also cannot escape copper prices and resource country risks。

If investors do not want to be held in a single company, they can also look at the copper mine ETF. Global X Cooper Miners ETF, an ETF that tracks global copper mining。

However, copper stocks are much more complex than copper。

The value of a mine depends not only on the price of copper, but also on the grade of the mine, the cost of cash, the shelf life, capital expenditure, the country in which it is located, tax policy, labour relations, environmental permits, transport conditions and managerial enforcement. Copper prices can raise the entire valuation of the plate, and eventually there will be a significant split between companies。

Resource country risk is particularly important. Many quality copper mines are located in Chile, Peru, the Democratic Republic of the Congo, Zambia, Mongolia and Indonesia. Resource endowments do not represent stable returns for shareholders. The greater the value of copper, the greater the Government ' s recalculation; the larger the project, the harder it is to address community, environmental, water and infrastructure issues。

Cost inflation also eats profits. When copper prices rise, energy, equipment, labour, steel and financing costs often rise together. A seemingly beautiful development project may have left little benefit to shareholders because capital expenditure was over-budgeted, production was delayed, licences were blocked。

Early copper mining companies are more risky. They refer to future reserves and future production, but each step from resource volume to allowable reserves, from researchable to financing, from licensing to construction, may fail. The long-term logic of copper does not mean that each copper unit can be realized。

Thus, copper mining shares are better suited to be understood as a leverage expression of copper price logic than a simple alternative to copper prices themselves. They can provide greater flexibility and lead to greater retreats. What is really worth studying are low-cost, long-lived, well-defined production paths, robust balance sheets and politically manageable companies。

THIS IS ALSO PART OF THE “GOLDIFICATION” OF COPPER: THE SCARCE LOGIC OF COPPER GOES BEYOND MERE SPOT AND FUTURES MARKETS AND IS BEING REPACKAGED BY STOCK MARKETS, ETFS AND SPECULATIVE FUNDS. THE INCREASE IN COPPER PRICES IS A ONE-TIER DEAL, AND THE INCREASE IN COPPER STOCK IS ANOTHER. THE FORMER REFLECTS THE COMMODITY ITSELF, WHILE THE LATTER REFLECTS HOW MUCH IMAGINATION THE MARKET IS WILLING TO PAY FOR THIS CHRONIC SHORTAGE。

The "gold" of copper is just beginning

The world needs more electricity, and more electricity means more copper。

Of course, copper doesn't really turn into gold. It does not have purely monetary attributes like gold, nor does it emerge from economic cycles. The global economic slowdown, the weakness of manufacturing industries and the cooling of risky assets all suppressed copper prices. Copper is still subject to fluctuations, and may even fluctuate sharply。

But the change is that the bottom logic of copper is different from the past。

In the past, copper prices have fallen sharply, often at a time when demand has weakened and oversupply has increased. Today's supply side is not that easy. The ageing of mines, declining grade levels, longer licensing cycles, smelting of raw materials and redistribution of benefits by resource countries make it increasingly difficult for copper to be simply treated as a common cycle。

It may still be industrial metal, but it is no longer a microcosm of the industrial cycle。

The "gold" of copper is just beginning。