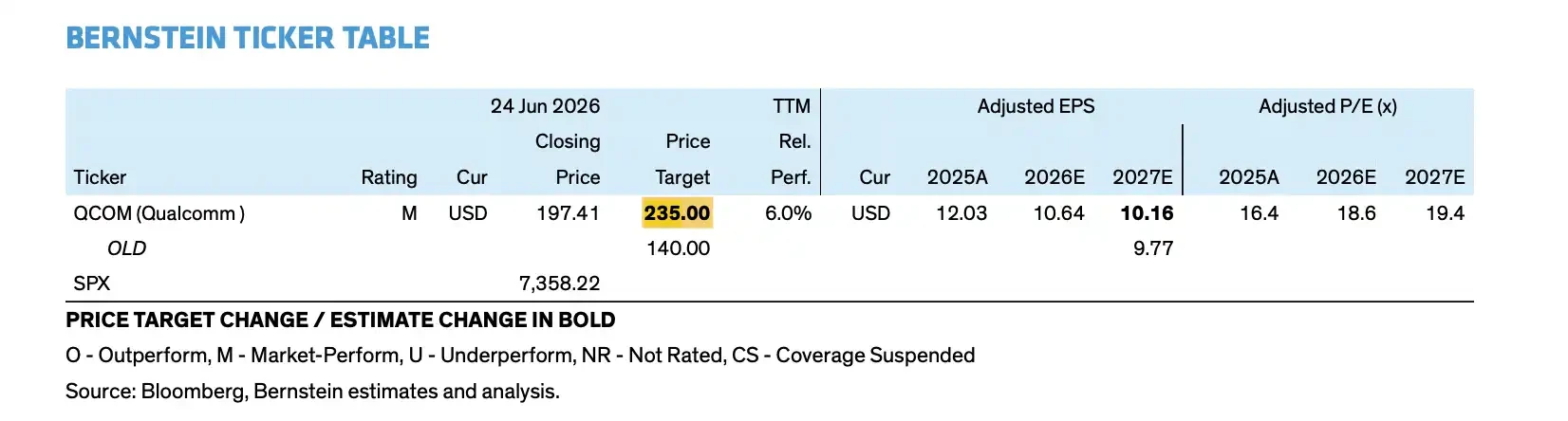

Bernstein raised the target to $235. Why is the rating still standing

LONG-TERM AI REVENUES ARE VALUED HIGH AND SHORT-TERM MOBILE PHONES AND COST PRESSURES REMAIN HIGH

TL;DR

- Bernstein raised the high-intensity target price from $140 to $235 but maintained the Market Perform rating。

- Chase FY2029 Target bet on data centres, cars and IoT, non-cellular income target approximately $40 billion。

- THE DOWNSWING IN MOBILE PHONE OPERATIONS, THE INCREASE IN OPEX AND THE UNCERTAINTY OF THE DATA CENTRE MĀORI RATE REMAIN CENTRAL CONSTRAINTS TO THE UNUPGRADED RATING。

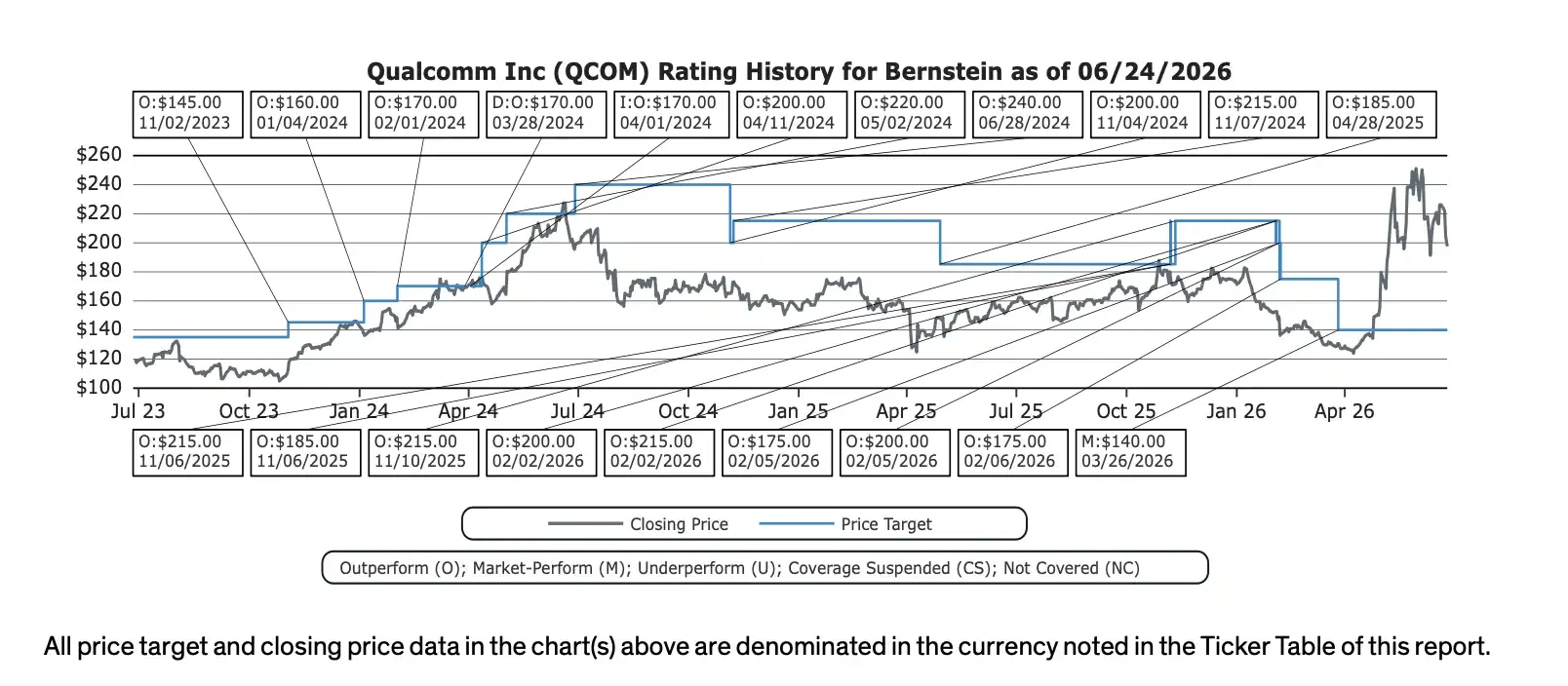

The target price went up, but the ratings didn't go up

After Invester Day in New York, he dropped a larger set of forward growth targets on the market. Bernstein subsequently increased the target price from $140 to $235 but maintained the markt Perform rating。

The increase in the target price is an indication that Bernstein's acceptance of the long story of Chase is growing. Instead of simply placing itself in the position of a mobile chip provider, the company is trying to enter the wider computing market such as the AI data centre, the car, Iot and personal AI devices. According to the official target of Chase, by FY2029 the company ' s non-cellular income will be about $40 billion, the data centre ' s income will be over $15 billion and the Non-GAAP EPS will be over $18。

HOWEVER, THE FACT THAT THE RATING WAS NOT INCREASED ALSO INDICATES THAT THE SELLER DID NOT CONSIDER THE STORY SUFFICIENTLY ESTABLISHED. THE REAL CONSTRAINT LIES IN THE TIME LAG: DATA CENTRES AND CAR OPERATIONS ARE MORE ADVANCED, MOBILE PHONE OPERATIONS ARE DOWN, APPLE REVENUES ARE OUT, OPEX INCREASES AND MĀORI RATE PRESSURES ARE MORE ADVANCED。

This explains why the target price of $235 does not amount to "buy in" signals. Bernstein acknowledged that the high-optimal far-term valuation ceiling had been lifted, but that the risk return had not been significantly tilted to the buy-in side, given that the current stock price reflected some optimistic expectations。

NEW STORY: FROM CELL PHONE CYCLE TO AI DATA CENTRE

The most important new story of this time is the data centre。

OFFICIAL CORPORATE TARGETS INDICATE THAT THE REVENUE FROM FY2029 DATA CENTRES WILL EXCEED $15 BILLION. COMPARED TO THE CURRENT DATA CENTRE REVENUE BASE OF ABOUT $30 MILLION, THIS MEANS THAT CHASE WILL ACTUALLY ENTER THE CLOUD MANUFACTURER AI INFRASTRUCTURE BUDGET IN THE COMING YEARS, NOT JUST IN THE MOBILE CHIP AND MARGIN CALCULATION MARKET。

The data centre routes disclosed by Chase include custom ASCIC, AI reasoning accelerator, Dragonfly C1000 CPU, connection products and related software layers. The company also mentioned two unnamed Hyperscaler customers, who are expected to contribute more than $1 billion in customized silicon revenues each to FY2027。

Meta Cooperation is another important validation point. Chase and Meta announced a multi-generational cooperation between the data centre CPU, and Dragonfly C1000 CPU is scheduled to start production in the second half of 2028. Here, however, caution is needed: the official expression is that Chase will be one of the suppliers, with no disclosure of the amount, capacity or exclusiveness。

Cars and Iot form the second growth curve. According to the official target, FY2029 revenue from automobile operations reached $10 billion and IOT revenue exceeded $14 billion. The car was increased from $45 billion 18 months ago to $65 billion, and the company continues to bet on digital cabins, auxiliary driving and on-board connection。

The target price of $235 is in 2029 instead of next year

At the heart of Bernstein ' s upward adjustment of the target price was not the sudden improvement in the short-term performance of Chase, but the start of the valuation model to incorporate larger data centre revenues and more balanced business structures。

According to the Bernstein model, Chase FY2029 received about $64.8 billion, EPS about $18.12, and the basic proximity company, Non-GAAP EPS, exceeded $18. Data centres, cars and IoT provide companies with an opportunity to obtain higher valuation multipliers than in the past, when the market was mainly focused on the cycle of mobile phones。

THE TARGET PRICE OF $235 CORRESPONDS TO A HIGHER VALUATION FRAMEWORK. BERNSTEIN USED THE AVERAGE EPS VALUE OF FY2027/FY2028 OF APPROXIMATELY $11.75 WITH A 20-FOLD MARKET GAIN; THE PREVIOUS FIGURE FOR THE TARGET PRICE OF $140 WAS APPROXIMATELY 14 TIMES. IN OTHER WORDS, THE KEY TO THE INCREASE IN THE TARGET PRICE IS NOT THAT NEXT YEAR THERE WILL BE A SIGNIFICANT UPSWING IN PROFITS, BUT THAT THE MARKET WILL BEGIN TO BE WILLING TO PAY MORE THAN A FEW TIMES FOR HIGH-TECH AI DATA CENTRES AND DIVERSIFIED INCOME STORIES。

BUT THERE ARE ALSO DIFFERENCES. THE BERNSTEIN MODEL ASSUMES THAT DATA CENTRE OPERATIONS HAVE A GROSS DOMESTIC PRODUCT RATIO OF ABOUT 40 PER CENT, WHICH IS LOWER THAN THE AVERAGE OF EXISTING COMPANIES. EVEN WHEN DATA CENTRE REVENUE IS RELEASED, IT MAY NOT BE POSSIBLE AT AN EARLY STAGE TO INCREASE OVERALL PROFITABILITY. THE REPORT ESTIMATES THAT, AS THE BUSINESS STRUCTURE CHANGES, THE OVERALL HIGH-INTENSITY MĀORI RATE MAY DROP FROM 55.2 PER CENT TO 51.6 PER CENT OF FY2029。

Cell phone pressure first, data center still waiting

Chase wanted data centres, cars and Iot to prove that the income structure would change, but mobile phone business pressure did not disappear。

THE SELLER ' S REPORT AND MANAGEMENT ' S Q & A CALIBRATION INDICATE THAT FP2027 ANJO ' S INCOME FROM MOBILE PHONES IS EXPECTED TO BE EVEN OR SLIGHTLY LOWER. ADD APPLE INCOME TO EXIT, AND TOTAL HANDHELD EQUIPMENT INCOME COULD DECREASE BY $5 BILLION TO $6 BILLION OVER THE SAME PERIOD. HANDHELD OPERATIONS CONTINUE TO BE THE LARGEST SOURCE OF CURRENT INCOME FOR CHASE, AND THIS DECLINE COULD HAVE A DIRECT IMPACT ON THE PROFIT BASE OVER THE NEXT TWO YEARS。

THE COMPANY IS ALSO MORE CAUTIOUS ABOUT ITS LONG-TERM ASSUMPTIONS ABOUT ANDRE MOBILE PHONES. FROM FY2026 TO FY2029, THE COMBINED GROWTH RATE OF ANDRE'S HANDHELD INCOME IS EXPECTED TO BE ABOUT 5 PER CENT, SIGNIFICANTLY LOWER THAN THE HIGH GROWTH PHASE OF THE PREVIOUS CYCLE. CHASE MAY STILL HAVE AN ADVANTAGE ON THE FRONT END OF THE ANDROID HIGH-END MACHINE, AI MOBILE PHONE AND RADIO FREQUENCY, BUT IT IS DIFFICULT TO FULLY OFFSET THE PRESSURE OF APPLE EXIT AND THE SLOWDOWN IN THE SMARTPHONE INDUSTRY。

THE COST END IS ALSO PRE-PRESSED. SY2027 OPEX WILL GROW IN DOUBLE DIGITS. IN ORDER TO ADVANCE THE DATA CENTRE CPU, AI ACCELERATORS, CUSTOM SILICON AND SOFTWARE ECOLOGY, COMPANIES NEED TO INVEST EARLY IN RESEARCH AND DEVELOPMENT, MARKETING AND CUSTOMER SUPPORT. REVENUE RECOGNITION USUALLY LAGS BEHIND INPUTS, WHICH MEANS THAT EPS PROJECTIONS AROUND EY2027 MAY INSTEAD HAVE A DOWNSIDE RISK。

THIS IS THE KEY TO HIGHER TARGET PRICES BUT UNCHANGED RATINGS: THE LONG-TERM STORY IS BIGGER, BUT THE PROFIT CURVE FOR THE NEXT TWO TO THREE YEARS IS NOT NECESSARILY BETTER. INVESTORS NEED TO ACCEPT TWO JUDGEMENTS AT THE SAME TIME: EY2029 EPS MAY BE RAISED BY AI DATA CENTRES, AND PROFIT PRESSURES AROUND EY2027 MAY BE MORE PRONOUNCED。

The disagreement is whether $15 billion of data centre revenues can be translated into real profits

The Bernstein report does not simply look at air highs, but rather reminds the market, while repricing highs, not to regard forward targets as performance already achieved。

In the next scenario, if data centre income is significantly below the $15 billion target and personal AI and computing business growth is more limited, Chase FY2029 EPAS may still reach about $15. This suggests that the basic drive of high-access is not fragile and that automobiles, IOTs, authorized operations and cost controls can still support a certain level of profitability。

HOWEVER, THE DIFFERENCE BETWEEN $15 AND OVER $18 EPS HAD A SIGNIFICANT IMPACT ON THE VALUATION. IF THE MARKET HAS ALREADY SET HIGH-THROUGH PRICING ON MORE OPTIMISTIC DATA CENTRE REVENUES AND HIGHER VALUATION MULTIPLIERS, COMPANIES WILL HAVE TO PROVE THREE THINGS: CLOUD-MANUFACTURING CUSTOMERS WILL BE ABLE TO SET UP AS PLANNED; DATA CENTRE PADDY RATES WILL NOT CONTINUE TO SLOW DOWN OVERALL PROFITABILITY; AND MOBILE-PHONE BUSINESS DOWNTURNS WILL NOT OVERPRESS EPS BEFORE NEW OPERATIONS MATERIALIZE。

As a result, the target price of $235 is not the conclusion that the "high-intensity AI transition has been successful" but rather the incorporation of long-term diversification prospects into new prices after valuation. It's really bigger than before, and it's more like a chip platform company that crosses mobile phones, cars, Iot and AI data centres。

Market Perform, however, cautions that there is still reason why the market should not be eager to treat Chase as an AI winner of certainty until mobile phone counterwind, data centre revenue release, and Maori rates are validated. What really needs to be tested next is not whether Chase can speak of the $15 billion data centre target, but whether it can be translated into income on time and eventually into a sufficiently good profit。