Coding's betboard made money, but Polymarket's a bad place for arbitrage

More than half a month, 1600 knives, 30% plus earnings, but what this article is trying to say is not how to make money。

Two days agoI USED AI TO GET MYSELF AN INVESTMENT JOB. STATIONI've been sharing several tools from Coding: a cross-market asset panel, an investment profile, a personal content console, and a recently frequently used Pollymarket stakeout panel。

FOR MORE THAN HALF A MONTH, WITH A PRINCIPAL FIGURE OF ABOUT 1,600 KNIVES, 30% PLUS, THE REAL-TIME STATISTICS ON THE PANEL AND THE NET NET NET INCOME AT THE END OF THE DAY WERE BASICALLY THE SAME, ABOUT 6 U, OR JUST A FEW ERRORS SUCH AS HANGING ORDERS/MOBILITY INCENTIVES。

But what I'm trying to say here is, it's not "Polymarket is good for money," and it's not a arbitrage course。

On the contrary, after this round, it became increasingly clear to me that Polymarket was not a place for arbitrage。

First, what's going on with this panel

I was about to start rubbing this panel around May 21st。

The initial demand is simple and does not want to open more than a dozen of the bet pages each time to cut back the price of yes/no, or to fill it in with Excel。

Yeah, until then, I used Excel to write down sales, floats, settlement nodes, type of event, stupidity。

But the little partners who have actually played know that many of the investments on Polymucket are easily out of control because of the poor functionality of hand-filling: For example, at the outset, it may be a small purchase, with the result that the rate of loss moves and adds, after all, there is a lack of an intuitive feeling; at the same time, for example, an event in which a bet is made and the table data is not updated in a timely manner, it is easy to miss the window to stop losses/scaling, etc。

In the end, the whole process is too fragmented, and when there is no system, people can easily rely on emotions。

So the panel was built from the very beginning, so I put every single bet back into a unified framework, so that this feeling becomes a relative visualization and horizontally comparable information。

After several editions, I split into two Tabs"Handing the dashboard" plus "opportunity monitoring"。

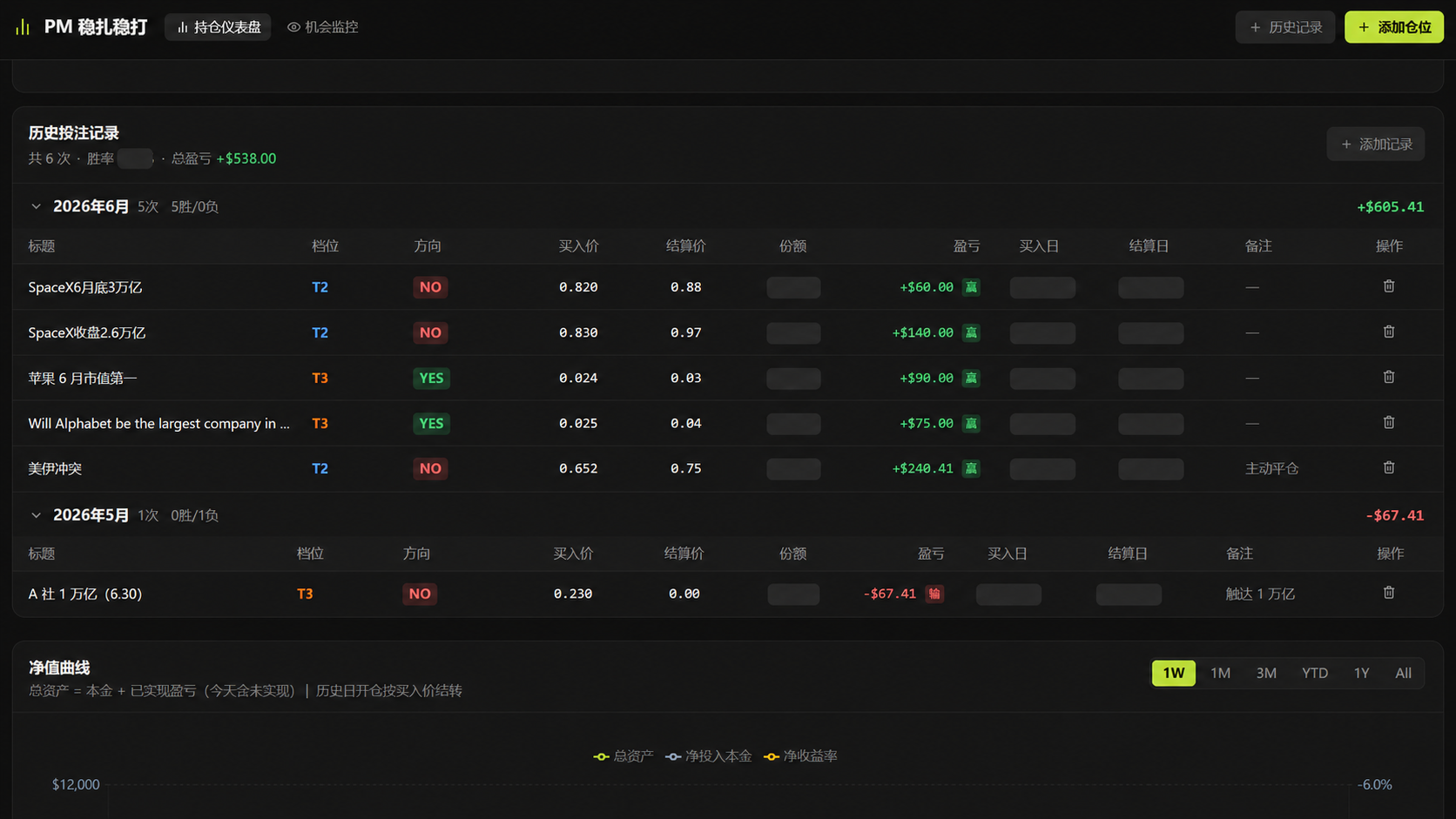

AS THE CORE OF THE ENTIRE PANEL, THE "CARRYING DASHBOARD" IS A DYNAMIC SYSTEM THAT CAPTURES REAL-TIME PM DATA AND RECALCULATES THEM INTO SEVERAL FUNCTIONAL AREAS (WHICH CAN BE COMPARED TO THE ORIGINAL MAP OF THE REFERENCE):

- General(a) Total principal (the plan, with little practical reference), principal investment, holding value, holding surplus, gross surplus (including closed) and a clear view of the account at first glance

- Tier slot share:This is the most central wind control module of the panel, and the most anti-intuitive and important area of the entire panel, I think

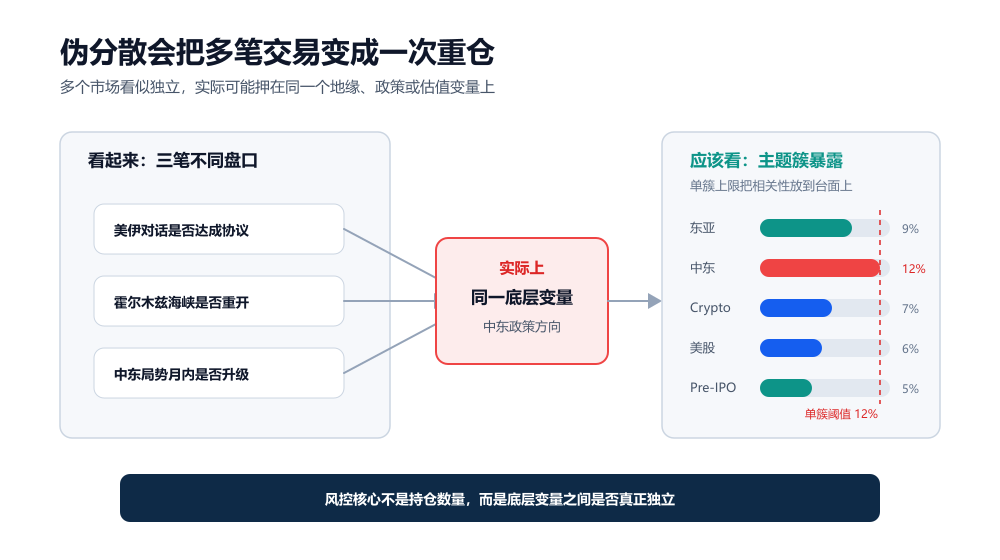

- Subject cluster exposure:I've labeled each of my notes as "themes" in East Asia, the Middle East, Cripto, U.S. stock, Pre-IPO (capable of self-defined additions and deletions), and the panel automatically aggregates the percentage of each cluster and sets a 12-per cent single-column ceiling threshold. It's mostly to counter the most hidden trap on PM - the false dispersion or the next chapter

- One note:The slotting, direction, purchase price, settlement price, share, profit or loss, date of purchase, settlement date, notes, etc., are clear and can be selected and screened in reverse in order

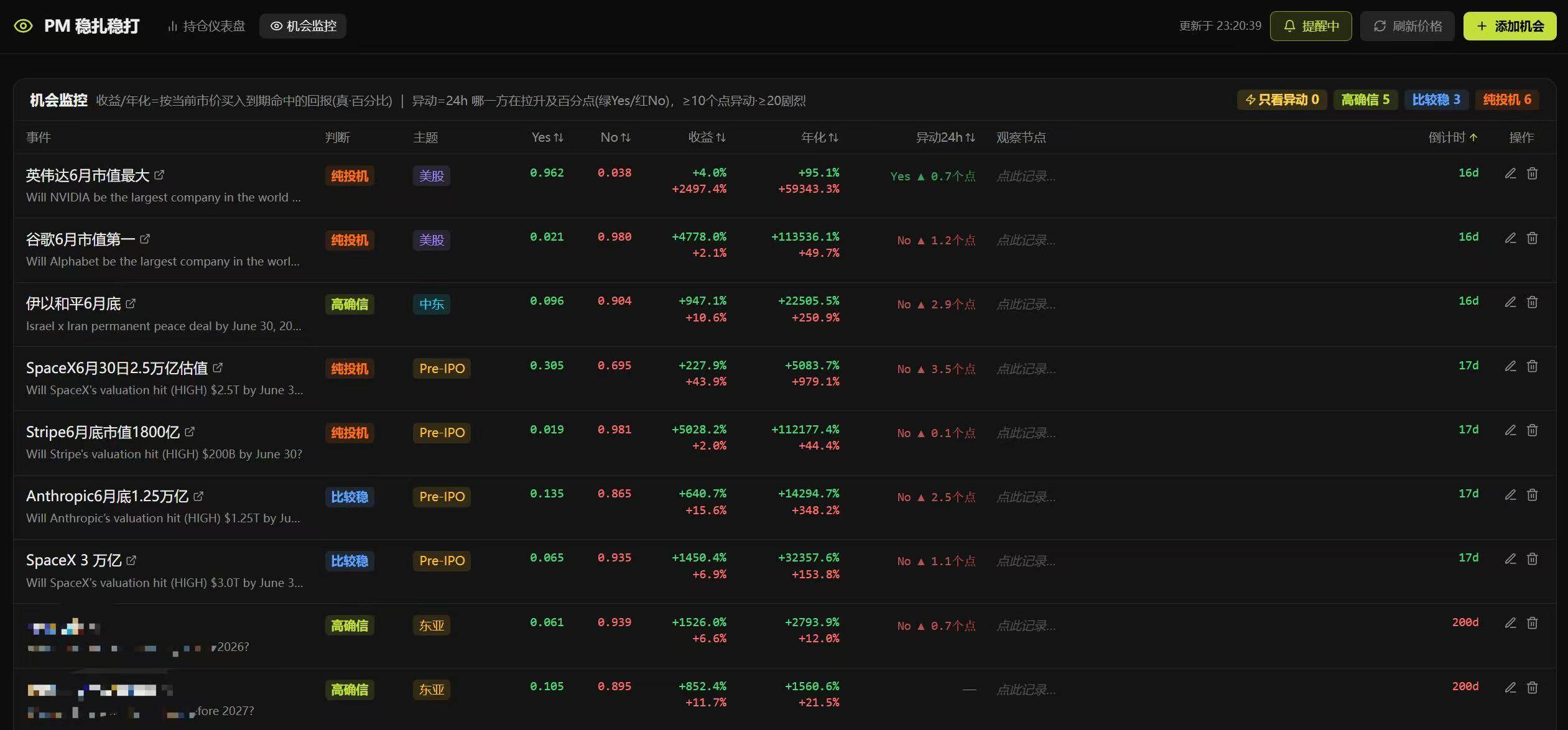

"opportunity watch" is a watchlist, and i'll put my interest in the market, but i haven't put any money in it yet。

Each market will record several key fields, including the event name (with a direct jumper of the trade page), T1/T2/T3 stratification, current yess/no prices, earnings, annualized earnings, agitation (which can be defined as a threshold of more than 20 per cent within 24 hours, e.g. a window alarm if the web page is open), the observation node that I set, and the countdown time when the input expires。

There are two small designs that I myself am satisfied with: firstly, a suitable PM interface was found, where the web link to the input event was thrown directly into the analysis, which automatically indicated yes/no options, the corresponding price, and the classification of different options under the same event, significantly reducing the problem of manual recording; and secondly, the Tier attribution of the same note was automatically reset with the remaining days。

Shortly before the Anthropic release of Mython, there was a marked price variation in the watchlist, which could largely be judged to be a high probability certainty event, at which point about 10 points of return could be eaten — an opportunity that would be difficult to catch without the watchlist。

II. THE MATHEMATICAL EXPECTATIONS TRAP FOR PM, AND THE T1, T2, T3 DESIGN PRINCIPLES

This is a brief introduction, and I'd like to say more about a reflection that comes after my reading。

THAT IS, THERE IS A BIG STRUCTURAL TRAP IN A BINARY MARKET LIKE PM, WHICH IS UNFRIENDLY TO PLAYERS WHO LIKE A "SINGLE SILO" BUT RATHER SUITABLE FOR A DECENTRALIZED CONFIGURATION THAT IS USED TO "OPEN A SUPERMARKET AND BUY A BUNCH OF THEM."。

I'll try to make my thinking clear

assuming that the price of a bet is 0.80, i.e., that the market believes that it has an estimated 80% probability that it will happen, if i judge that the event is real, q is 0.90, it means that the expected rate of return on the bet can be roughly calculated:

EV = q / c - 1 = 0.90/0.80 - 1 = 12.5%

THIS LOOKS GOOD, BUT PM'S NOT A BOND, THIS 12.5%If you're wrong, the loss is not 12.5%, but 100%。

So I'm not just looking at the expected rate of return in the panel, but I'm looking at two things at the same time:

- one is the gap between my own probabilistic judgment and market prices, i.e. q-c (i set an automatic stop-point target, which is the median purchase price and 100), which is the core of whether edge actually exists

- The other is the impact on the general account of a single warehouse at zero once the matter is wrong

THE SECOND REASON IS ALSO THE SOURCE OF THE T1, T2, T3 LAYERS REFERRED TO IN CHAPTER I。

In short, I have three categories:

- T1 HIGH: FOR ME, COMFORT ZONES ARE RELATED TO EAST ASIA AND TO SOME GEOPOLITICS, AND I FEEL THAT THERE IS POOR INFORMATION IN THE EAST AND THE WEST, WHICH IS REPEATED

- T2 is relatively stable: there are some perceptions that the present apparent implied probability is higher than actual yes or no pricing

- T3 PURE SPECULATION: THE ONE WITH A HIGH RATE OF COMPENSATION, AND THE ONE THAT CANNOT BE TAKEN FREQUENTLY, PREFERABLY IN REACTION, WHICH RETURNS TO A CERTAIN PRICE AND THUS TAKES SHORT-TERM GAINS

BUT IT ALSO NEEDS TO BE NOTED THAT T1 HAS HIDDEN COSTS, ESPECIALLY ON LONG-TERM MARKERS, SUCH AS A T1 RATING OF 18% STATIC RETURNS, BUT AFTER 180 DAYS, IRR MAY BE 3-4% ANNUALIZED, RATHER THAN LEAVING THE MONEY BEHIND, AND DURING THIS PERIOD THE PRINCIPAL IS LOCKED, AND YOU MISS THE LATER HIGH IRR OPPORTUNITY。

SO I'M GOING TO BREAK UP A FEW MORE SLOTS INSIDE T1 (PART OF PURE PERSONAL THINKING, NOT SHARING, DOWN) IN THE SHORT RUN, AND IN THE LONG RUN T1-A CAN HIT MORE, AND IN THE LONG RUN T1-C, WITH TOO MANY LOW IRR LONG-TERM TARGETS, IT'S HIDDEN FINANCIAL EFFICIENCY LOSSES。

T2 has edge, but leaves room for "misjudgement" with a single cap of 8-10 per cent, which means that, even if this is a total loss, the total account loss is within 10 per cent, without prejudice to the opportunity to remain engaged in follow-up。

THE T3 RATE IS GOOD, BUT TO OBSERVE WITH THE SMALLEST SPACE, RATHER THAN RELYING ON IT TO EARN A LOT OF MONEY, IT IS TO FIGHT BACK, TO EAT SHORT-TERM RETURNS — TO ALLOW ITSELF TO KEEP TRACK OF HIGH-COST EVENTS AND TO DEVELOP A SENSE OF SUCH EXPOSURE。

In general, the ceiling is essentially to give "I may have misjudged" room at a cost。

There is a counterintuitive but particularly important point here, which is that there is a high level of certainty that it is not equal to a high level of space。Even if you think that there's a 95% probability, as long as there's a 5% probability of zero, the position must be limited。

For an extreme example, assuming you're making 10 successive bets that you think the odds are 95%, each sounds stable, but as long as they're independent of each other, the probability of at least one mistake is about 1-0.95 ^10 ≈ 40%

I've done so much, I've always had that mistake。

IT'S JUST AN EVENT OF INDEPENDENCE, AND IN REALITY, THERE'S A LOT OF PM MARKETS THAT ARE NOT INDEPENDENT, AND THEY'RE OFTEN RELEVANT, LIKE "DOES THE AMERICAN-IRANIAN DIALOGUE AGREE?" WHETHER OR NOT THE STRAIT OF HORMUZ HAS REOPENED "THE SITUATION IN THE MIDDLE EAST DURING THE MONTH" APPEARS TO BE THREE SEPARATE MARKETS, BUT THE BOTTOM VARIANT IS ALMOST THE SAME — THE GEO-POLICY DIRECTION OF THE MIDDLE EAST — WHERE, ONCE JUDGED WRONG, THE THREE WERE BLEEDING SIMULTANEOUSLY。

It is also the greatest help to me, not to increase the chances of winning, but to limit myself to making mistakes. The core value of this panel is not revenue statistics, but wind control。

Three. After this round, my real opinion of Polymarket

It's more than half a month of depthPolymarket wasn't without a chance, but it was never the kind of arbitrage that many people imagined。

We used to play arbitrage on the chain, mostly with clear rules, and prices being locked in the wrong, but Polymarket, unlike you, tested your logical understanding of a change in the direction of a given bet (which feels difficult to express in words)。

For example, the political and economic dynamics associated with East Asia and the fact that Chinese users may indeed have a certain information gap advantage are worth exploring, but that does not mean that you will win. Pollymarkett ultimately settles not by "the reality you understand" but by market rules and by assigning data sources (UMA manipulations are also frequent)。

Besides, you think something is nailed to the Chinese language, and it doesn't mean the definition in the English rules, especially when the rules for each bet are set, there are often some text traps。

So according to my actual experiencePM DOES NOT HAVE THAT MANY ARBITRAGE OPPORTUNITIES, MAINLY DUE TO POOR INFORMATION AND FRAGMENTATION, AND MAY ENCOUNTER BLACK SWANS EVEN WITH HIGH CONFIDENCE。

Once it's met, it's nothing。

As a friend said, "I don't want to get lucky if it's only a 1% zero chance."。

Because of these mathematical expectations, it's negative in the long run。

SO I NOW UNDERSTAND PM MORE CONSERVATIVELY:

- First, if you don't act as a stabilizer of earnings, even if you're a highly convinced input, especially if you win several times in a row, don't feel like you've found the ATMAfter you win in a row, it makes you think you can judge everything

- Second, don't equate a high-winner with a good deal, a 90 per cent-winner event, and if the market price is already 0.95, it could be a negative one; in turn, a 40 per cent-winner event, if the market gives only 0.20, could have a positive expectation

- Thirdly, it's particularly important not to lose sight of the tail risk, as many people see that 10%, 20% of the returns are stable, but as long as the transaction is wrong, it's not a traditional low-risk gainFROM THIS PERSPECTIVE, I DON'T EVEN THINK THAT THERE'S ANY LOW-RISK OPPORTUNITY ON PM, AND EVERY ONE OF THEM IS HIGH-RISK;

- Fourth, don't pretend to be dispersing, buy a number of different sets, which is not necessarily to be divided, as mentioned above. Whether or not the Strait of Hormuz is reopened, "The situation in the Middle East escalates during the month", which appears to be three separate markets, but the bottom variable is almost the same

SO I'D RATHER SEE PM AS A TRAINING GROUND FOR JUDGMENT。

It coincides with the political, economic, technological and financial information that I like the most in my day-to-day life, turning the judgment into something that can be given positive feedback。

THESE CAPABILITIES, OUTSIDE THE PM, ARE EQUALLY USEFUL。

By the way, in addition to this PM vending panel, I used Codex to develop a private market valuation dynamic monitoring panel, mainly to track the evolution of valuations in the private market by unicorn companies - Anthropic, Openai, Stripe, Kraken, etc. - and the relationship between these changes and the corresponding PM notes。

Polymarket is essentially an expected market, and there are times when signals in the private market have changed, but PM prices have not moved; sometimes PM prices have moved ahead, and real data have not kept pace, and the mismatch between the two is something that deserves constant observation。

Of course, this is not a risk-free arbitrage, the private market valuation itself is not fully transparent and may differ from one data source to another, but as an observation framework, it is interesting to find an opportunity to write separately。

Summary

The whole story was never "I made 30% of the panel, you can."。

I think it's more useful to have a tool to help youTurning sense into framework, turning framework into disciplineMany times, many people, making money, doesn't mean they've found the secret, it's the right round of judgment。

The difference is important。

It is also suggested that you can start trying Vibe Coding without necessarily having to experience it with Claude Code, with Codex and even Kimi's recently launched Kimi Work, and that if you open up something that is not convenient for overseas subscriptions, then you can share some of the silk slides I use myself。