AL REMODELS THE RISING LOGIC OF THE GLOBAL DISTRIBUTION OF CATTLE MARKETS BEHIND THE SEMICONDUCTOR SMILE CURVE

Four months up by 230%, how far can the semiconductor's "calculated neck" go

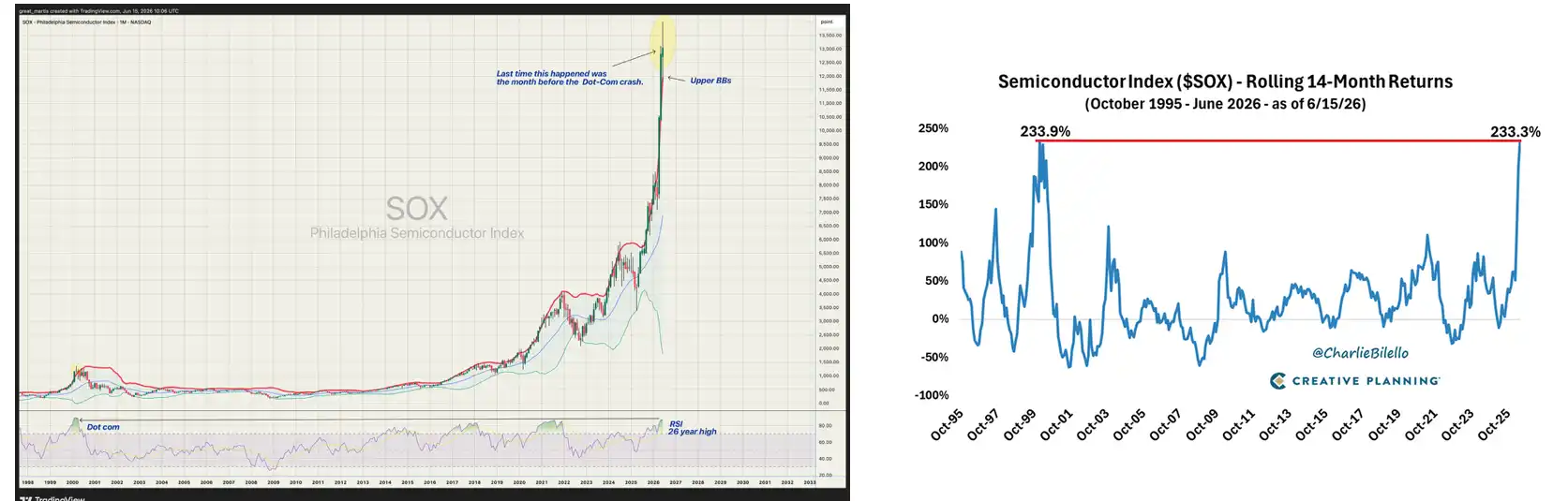

THE U.S. STOCK CLOSED IN THE MORNING, AND THE PHILLY SEMICONDUCTOR INDEX SOX BROKE 14000 POINTS FOR THE FIRST TIME, MAKING A RECORD HIGH。

IN HISTORY, SOX INCREASED BY OVER 230 PER CENT IN 14 MONTHS ONLY TWICE: FROM DECEMBER 1998 TO FEBRUARY 2000, AND FROM APRIL 2025 TO THE PRESENT。

THE RETURNS FROM THIS ROUND OF SEMICONDUCTOR CATTLE ARE CONCENTRATED AND SIGNIFICANT. THE YEAR-ON-YEAR INCREASE IN THE STORAGE OF THE TRIADS, SK HERCULES AND SAMSUNG WAS APPROXIMATELY 141, 186 AND 114 PER CENT, RESPECTIVELY. TSMC US SHARE ADR GREW BY MORE THAN 50% DURING THE YEAR。

On May 14th, the New York Times of the United States of America created a record of US$ 235.47. Broadcom, Marvell, and ASML have all updated or approached their respective breakaway tracks. The 52-week low point for the entire SOXX ETF is $148, the height is close to $369 and the amplitude is close to 150%。

GOLDMAN SACHS INCREASED THE 2026 DRAM SUPPLY AND DEMAND GAP FORECAST FROM 3.3 PER CENT TO 4.9 PER CENT IN APRIL, CALLING IT THE WORST STORAGE SHORTAGE IN 15 YEARS. HBM PRICES ARE EVEN MORE EXAGGERATED, WITH HBM3E STACKING OF ABOUT $300 PER UNIT AND UPCOMING PRODUCTION OF HBM4 ESTIMATED AT $500 PER UNIT. IN 2026, HERCULES HBM WAS ALREADY COVERED BY MICROSOFT, GOOGLE, AND INWEIDA, AND CLIENTS EVEN PAID THE DOWN PAYMENT IN FULL。

APPARENTLY, AI DATA CENTRES ARE BEING BUILT AT A MUCH FASTER RATE THAN THE CHIP PRODUCTION CAPACITY IS EXPANDING。

Cow City

Scarcity is the most profitable product。

THE CORE LOGIC OF THIS SEMICONDUCTOR CATTLE MARKET IS LARGELY UNDERSTANDABLE. WHOEVER'S STUCK IN THE NECK OF AI CAPITAL GETS THE HARDEST PRICING. ON THE OTHER HAND, WHO CAN BE REPLACED AND UNDERVALUED, EVEN IF THE DEMAND IS GREATER, THE STOCK PRICE WILL NOT RISE。

Light modules are typical of the latter. Photon Capital's April report noted that China's light module occupied seven of the top 10 seats in the world, but did not earn much, but rather chip companies. Middle and new euphemisms on 800G, 1.6T light modules, and cost control are already at a global level, crushing the profits of Coherent, Lumentum, these American stocklight modules. Demand doubles, and profit margins are depressed. One reason for this is that the assembly of light modules is not scarce。

And it's the hardest main line in the semiconductor of this round. It's basically because it's stuck in the neck and the more it's stuck。

HBM IS NOT AN ORDINARY DRAM. 3D STACKING, TSV SILICON PERFORATION, AND A DEDICATED CONTAINMENT PROCESS, EACH LAYER OF TECHNICAL BARRIERS IS THE RESULT OF MORE THAN A DECADE OF HEAVY ASSET INPUT. THERE ARE ONLY THREE COMPANIES WITH GLOBAL ENERGY HBM, AND HERCULES TOOK ABOUT HALF OF IT。

Interestingly, this logic is equally valid at the macro-national level。

AI’S TRUE WINNERS IN THE INFRASTRUCTURE OF THE DATA CENTRE ARE NOT “ALL SEMICONDUCTOR COUNTRIES” BUT COUNTRIES AND TERRITORIES THAT HAVE, IN THE PAST FEW YEARS OR EVEN DECADES, CREATED A SCARCE INDUSTRY CLUSTER AT AN IRREPLACEABLE LEVEL. SCARCITY IS THE FOCUS。

Every district has its own main track

It's very interesting to see it in the American stock community。

At the top of the value chain is the United States。

In Weida, AMD, ASI design of Chase, the EDA tool of Synopsys and Cadence, the AI network of Arista, the three main cloud manufacturers sold their calculations to the world. Google, Amazon, Microsoft are accelerating self-study. Both Mob and Marvell collectively took about 95 per cent of the customized ASC design market, and light Google spends about $8 billion a year on the TPU development。

The core nodes at the manufacturing end are on stage and in Korea, but they eat completely different meals。

And this side of the stage is built around TSMC and advanced seals. The 3 nm and 2 nm processes are global only for power generation. TSM3 three CoWos back-end factories are fully loaded, with a deadline of 52 to 78 weeks, and the Ingweidas have locked 60 to 70% of the CoWos capacity. TSMC is expanding monthly capacity from 35,000 by the end of 2024 to 130,000 by the end of 2026, nearly four times. But even with so much expansion, capacity is still tight. The server-supplier system, Honghai, Guangda, Latitue, is also measured with the arrival of the AI server。

THE SOUTH KOREAN STORY IS ALL ABOUT STORAGE. HERCULES TOOK ABOUT 50 TO 55 PERCENT OF THE GLOBAL HBM MARKET SHARE, WITH SAMSUNG ACCOUNTING FOR 19 TO 35 PERCENT, AND AMERICAN LIGHT ABOUT 5 TO 20 PERCENT. HBM IS NOT THE SAME AS ORDINARY MEMORY, WITH 3D STACKING, TSV SILICON PERFORATION, AND A DEDICATED SEALING PROCESS, EACH LAYER OF TECHNICAL BARRIERS BEING THE RESULT OF CONTINUOUS MONEY-THROWING BY KOREAN ENTERPRISES OVER THE PAST DECADE OR SO。

THE ROLE OF JAPAN AND THE NETHERLANDS IS ALSO IMPORTANT. THE TOKYO ELECTRONS MAKE SEMICONDUCTOR EQUIPMENT, ICCM AND SUMCO MAKE SILICONE COLLAGES, ODORS MAKE A BAF BASE PLATE MATERIAL. JAPAN HAD LONG BEEN OUT OF COMPETITION FOR CHIP TERMINAL PRODUCTS, BUT IT WAS IN A POSITION OF MATERIAL AND PRECISION PROCESSING, AND NO ONE COULD REPLACE IT TODAY。

AND THE NETHERLANDS IS EVEN MORE DIRECT, ASML MONOPOLIZING THE EUV CARVING MACHINE. MORGAN SIGNIFICANTLY RAISED THE TARGET PRICE TO 1,400 EUROS IN JANUARY, PREDICTING THAT 2027 WILL BE THE HIGHEST RATE OF GROWTH FOR ASML, WITH THE EPS INCREASING BY 57 PER CENT. THEY BASE THIS JUDGEMENT ON THREE DRIVERS: ADVANCED LOGICAL PROXY EXPANSION OVER EXPECTATIONS, LARGE-SCALE EXPANSION IN THE AREA OF DRAM STORAGE, AND OVERALL DEMAND PERFORMANCE BETTER THAN EXPECTED. BESI ALSO RECEIVED A LARGE NUMBER OF ORDERS FROM THE DUTCH SEALING EQUIPMENT COMPANY DURING THE OUTBREAK OF DEMAND FOR THE AI CHIP。

THE ENTRY POINTS IN CHINA AND EUROPE ARE DIFFERENT, BUT THE LOGIC IS SIMILAR, WITH COST ADVANTAGES OR DELIVERY CAPACITY BUILT AT A SPECIFIC POINT IN AI INFRASTRUCTURE。

Middle-intensity and new euphoria on 800G, 1.6T light modules and price controls are the global front. Photon Capital's analysis, however, also serves as a reminder of an important window of time: the high profitability of the current light module company, which comes from temporary pricing rights arising from 800G production-stage shortfalls. By the second half of 2026 to 2027, the volume of 1.6 T and the capacity of the second- and third-line manufacturers will have arrived at the price pressure at the end。

On the European side, Schneider Electric, ABB, Vertiv, the distribution and dispersion companies, received far more than expected orders in the context of the surge in electricity consumption in the data centre. Wedbush estimates that the AI infrastructure expenditure in 2026 was approximately $72.5 billion, an increase of 77 per cent over the same period, with electricity infrastructure being one of the fastest growing sub-items。

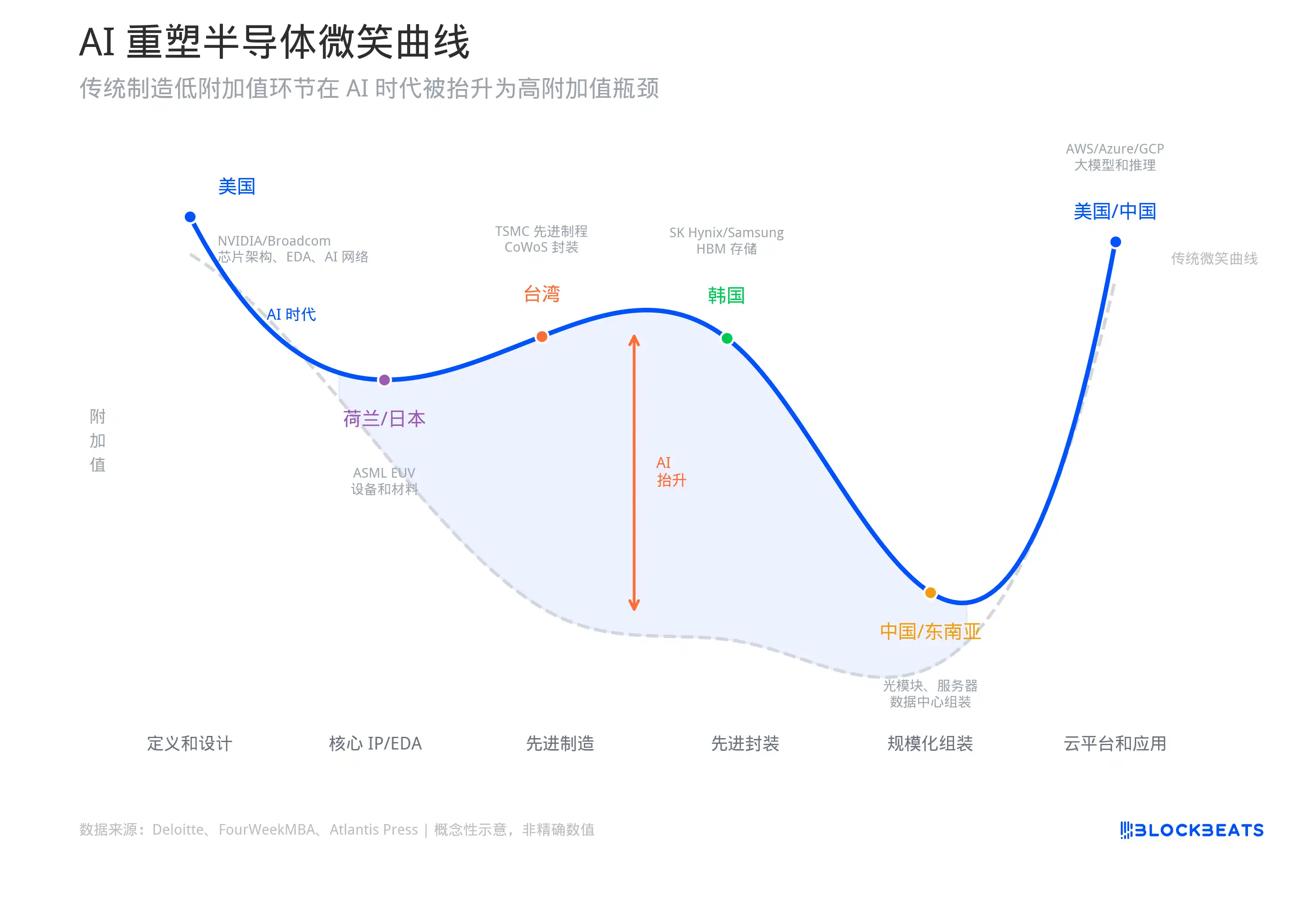

AI RESHAPING SEMICONDUCTOR SMILE CURVE

If this is summed up by a smile curve: the left-hand US is responsible for "definition and design," the middle China Taiwan, South Korea, the Netherlands, Japan is responsible for "manufacturing advanced chips", the lower China Taiwan, China, South-East Asia is responsible for "mass assembly" and the right US and China are responsible for "window platform, model, and customer entrance"。

The original of this curve was the founder of Acer, who used this model in 1992 to explain why PC assembly was the least profitable。

BUT 30 YEARS LATER, AI DATA CENTRES ARE REWRITING THE SHAPE OF THIS CURVE。

The value chain analysis of FourWeekMBA and a paper by Atlantis Press this year point to the same conclusion: AI has raised the middle of the traditional smile curve. TSM's advanced sealing of CoWos, Hercules' HBM stacking, and ASML's EUV carving machines, which are among the least profitable "intermediate parts" of the traditional manufacturing smile curve, have become the most scarce resources in the AI era, with profit margins and pricing rights no less than at the design and application end。

ACCORDING TO THE PAPER, THE MĀORI RATE BETWEEN 2023 AND 2024 WAS 72.72 PER CENT, NET INTEREST RATE 48.85 PER CENT. HOWEVER, THE MĀORI RATE FOR Q1 IN 2026 ALSO REACHED 66.2 PER CENT WITH A NET INTEREST RATE OF 50.5 PER CENT. THE PROFIT MARGIN GAP BETWEEN THE DESIGN AND MANUFACTURING ENDS IS NARROWING, UNPRECEDENTED IN THE HISTORY OF THE SEMICONDUCTOR INDUSTRY。

THE TRADITIONAL SMILE CURVE CONSIDERS THE MANUFACTURING CHAIN TO BE THE LEAST PROFITABLE. AI HAS TURNED THE MOST DIFFICULT MANUFACTURING LINKS INTO THE MOST SCARCE RESOURCES。

MORGAN'S MARCH ASIA SEMICONDUCTOR REVIEW SUMMARIZED A SIMILAR CONCLUSION: THE AI CYCLE BETWEEN 2023 AND 2024 WAS CONCENTRATED ON GPU, AND BETWEEN 2025 AND 2026 DEMAND BEGAN TO SPREAD TO A WIDER INDUSTRIAL CHAIN, WITH STORAGE, ADVANCED SEALING, CUSTOMIZATION ASIC, AND DATA CENTRE NETWORKS ALL WORKING。

Each turn of the bottleneck pushes a group of previously neglected companies onto the front desk, while allowing the largest increase in the previous round to enter the digestive period。

How far can a cow go? Open view game

Let's hear it first. Wedbush's Dan Ives directly shouted on CNBC in May that NASDAQ would look at 30,000 points in the coming year on the grounds that the demand for AI chips is still far greater than supply. Goldman Sachs gave a more specific figure, with global AI capital spending of about $76.5 billion in 2026, rising to 1.6 trillion in 2031。

MORGAN WROTE CLEARLY IN THE ASIA SEMICONDUCTOR STUDY RELEASED IN MARCH: AI IS STILL EXPANDING AND THE SEMICONDUCTOR INDUSTRY IS ENTERING A NEW STRUCTURAL DEMAND CYCLE。

MULTIPLE JUDGEMENTS ON STORAGE ARE MORE RADICAL. GOLDMAN SACHS RECENTLY REDUCED THE DRAM SUPPLY AND DEMAND GAP FORECAST FROM 2026 TO 2028 TO A DEEPER DEFICIT ZONE, REVISED FROM THE PREVIOUS -2.5 PER CENT TO -5.9 PER CENT ALMOST DOUBLED IN 2027. THEIR JUDGEMENT IS THAT THE LIFE CYCLE OF THIS ROUND IS DIFFERENT FROM THAT OF THE PAST, THAT THE DEMAND FOR AI SERVERS IS MORE VISIBLE, THAT SUPPLY GROWTH IS STUCK TO A LONG-TERM LOCK-IN AGREEMENT, AND THAT THE PRICE RISE WILL LAST LONGER THAN THE MARKET EXPECTED。

Goldman Sachs even gave Kioxia an upward adjustment in business profits projections for the three years 2027 to 2029, ranging from 16 to 48 per cent, on the grounds that the high profits could last two to three years. It is very rare on Wall Street to judge a company that is engaged in the storage of such a strong-cycle business as a “high-profit business lasting three years”。

MORGAN'S ATTITUDE IS MORE INTERESTING. THEY WERE ALSO SHOUTING "DRAM WINTER" IN 2024, PREDICTING PRICES FALLING FROM Q4 IN 2024. AS A RESULT, IN 2025, THE DIRECT TURN TO SUPERCYCLICAL THEORY IS PROJECTED TO INCREASE THE PRICE OF DRAM BY 62 PER CENT IN 2026, AND THE PROFITS OF HERCULES AND SAMSUNG WILL EXCEED AGREED EXPECTATIONS BY 30 TO 50 PER CENT。

But the noise is not small, and it's not small。

Michael Burry publicly warned in May that the semiconductor pattern was similar to the last months of the Internet bubble from 1999 to 2000. SOX grew 65% during the year, 10% per week, SOXX ETF 60% higher than the 200-day average, and this technical stretch is rarely sustained in history. SEC ' s holdout disclosure shows that he purchased a large number of drop options for SOXX, QQQQ, Weidar, Palantir and Oracle, with expiry dates in January 2027, with market rights far below current equity prices。

In June, an article dedicated to breaking the AI foam risk was published by Man Group, one of the world's largest listed hedge funds. Their central point is that the financial architecture around AI has become too large, overleveraged and over-reliant on a few interrelated players。

IN PARTICULAR, THEY NOTED THAT A LARGE NUMBER OF AI DATA CENTRE CONSTRUCTION WAS FINANCED THROUGH PRIVATE CREDIT, WHICH WAS SECURED BY “HARDWARE THAT DEPRECIATED RAPIDLY LIKE MOBILE PHONES, NOT LONG-TERM ASSETS LIKE BUILDINGS”. THE FIRST WAVE OF DEFAULT MAY OCCUR BETWEEN 2027 AND 2028, WHEN THE INITIAL LEASE EXPIRES, AND THE GAP BETWEEN FINANCING ASSUMPTIONS AND REALITY BECOMES INEVITABLE。

Looking forward, several points of time warrant our attention。

ON JUNE 24TH, THE FISCAL DAY, THE FORWARD-LOOKING DIRECTION OF HBM DEMAND AND DISTRIBUTION OF CAPACITY WILL DETERMINE THE DIRECTION OF THE STORAGE PLATE THROUGHOUT THE SUMMER. THE NEXT FINANCIAL REPORT FROM INGWEIDA IS EQUALLY CRITICAL, AND IF THERE IS EVEN A SLIGHT SLOWDOWN IN THE DEMAND FOR THE AI CHIP, THE ENTIRE PLATE WILL BE RE-PRICING。

A little further away, the timeline for the release of capacity is a real watershed. Hercules' M15X plant is expected to release by mid-2027, and Yongin's new plant advanced to February 2027. Three-star P5 factory started production in 2028. Idaho Fab 1 of the beautiful light is expected to contribute in mid-2027。

TOGETHER, INDUSTRY CAPACITY WILL INCREASE BY 20 TO 30 PER CENT BETWEEN THE SECOND HALF OF 2027 AND THE FIRST HALF OF 2028. THE PROBLEM IS THAT HBM DEMAND IS GROWING AT A COMPOUND RATE OF OVER 40%. SUPPLY CHASE DOES NOT CATCH UP WITH DEMAND, DEPENDING ON IF AI CAPITAL SPENDING SLOWS DOWN BEFORE THAT。

THE LAST VARIABLE IS GEOPOLITICS. THE HIGHER THE CONCENTRATION OF THE SEMICONDUCTOR SUPPLY CHAIN, THE GREATER THE IMPACT OF THE BLACK SWAN. TSMC, A COMPANY THAT ACCOUNTS FOR MORE THAN 90 PER CENT OF THE WORLD ' S ADVANCED PROGRAMME, IS EFFICIENT IN CATTLE MARKETS AND SYSTEMIC RISK IN CONFLICT SETTINGS. THE EASE WITH WHICH THE TAIWAN STRAIT, THE US-CHINA EXPORT CONTROLS, AND THE DEGREE OF CO-OPERATION IN THE JAPANESE MONEY CONTROL OF EQUIPMENT ARE BEING DISCUSSED AT A GOOD TIME, BUT THE RATE OF PRICING CHANGES FASTER THAN ANY FUNDAMENTALS。