The first component of the concept of the forecast market has emerged

Robinhood took Kalshi, an ally who had become the strongest opponent。

Original Odaily Daily Planet (@OdailyChina)

By Azuma (@Azuma eth)

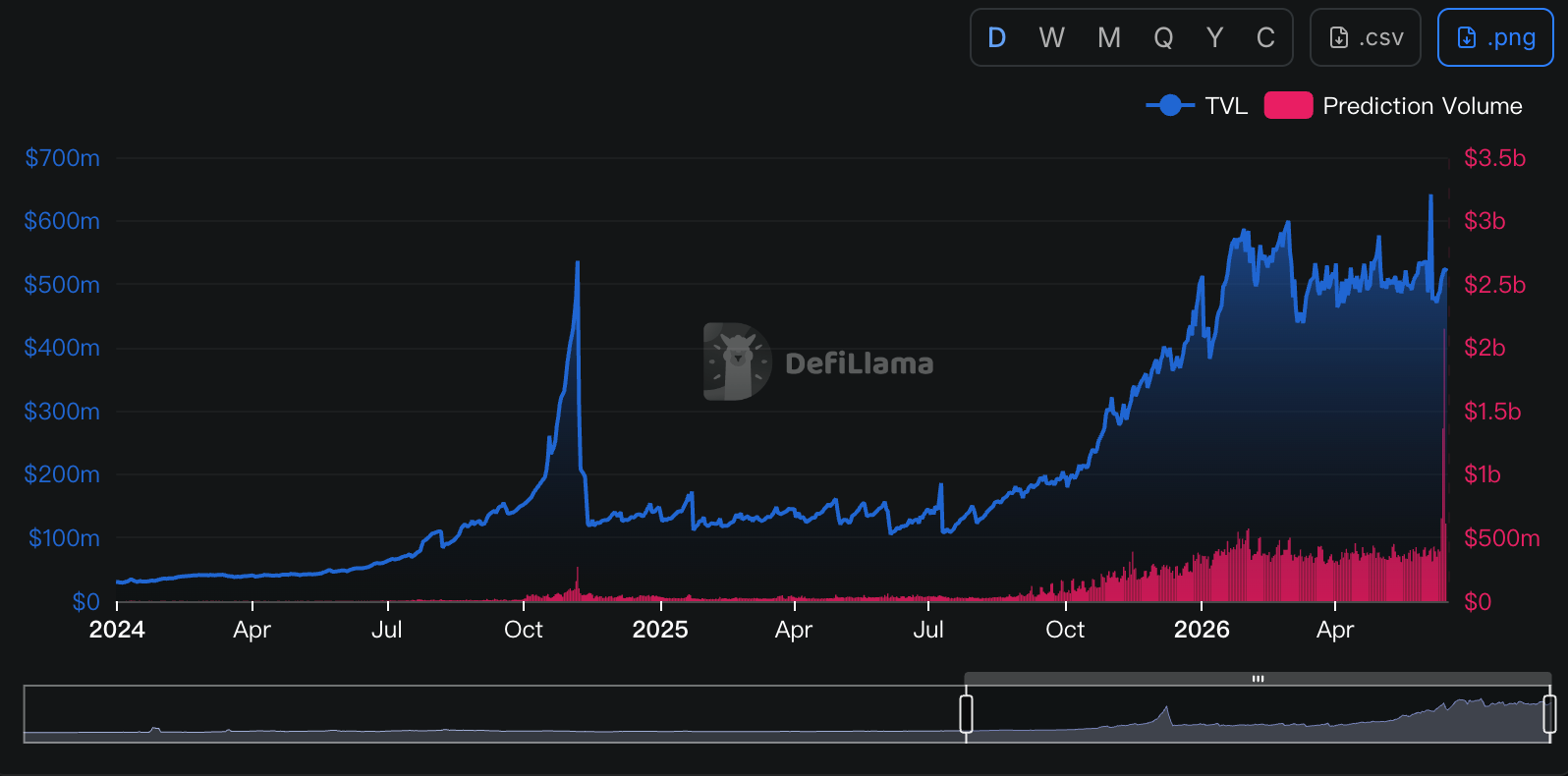

World Cup battles have been raging, and the market is forecast to grow in total Internet trade, but Kalshi, the industry leader, may not be in a good mood。

The reason is not that Kalshi's own business data fluctuates, but because Kalshi's “suddenly” appeared before him as another enemy after Polymarket, who was once his most important ally。

- Odaily Note: Data from & nbsp;DefillamaI don't know。

Kalshi's most important traffic channel - Robinwood

Put the time back in March 2025。On the other hand, Kalshi announced cooperation with Robinhood, an online United States voucher, who would use the former to provide its users with forecasting market transactions, allowing users to bet on political, economic, sports events。

In terms of business models, this is a typical “requirement” - Robinhod, who is responsible for user access and distribution of transactions, has direct access to the mature products of Kalshi; and Kalshi, who is responsible for the bottom markets, arranging, clearing, and regulating compliance systems, has access to the huge bulk pool that Robinhod owns。

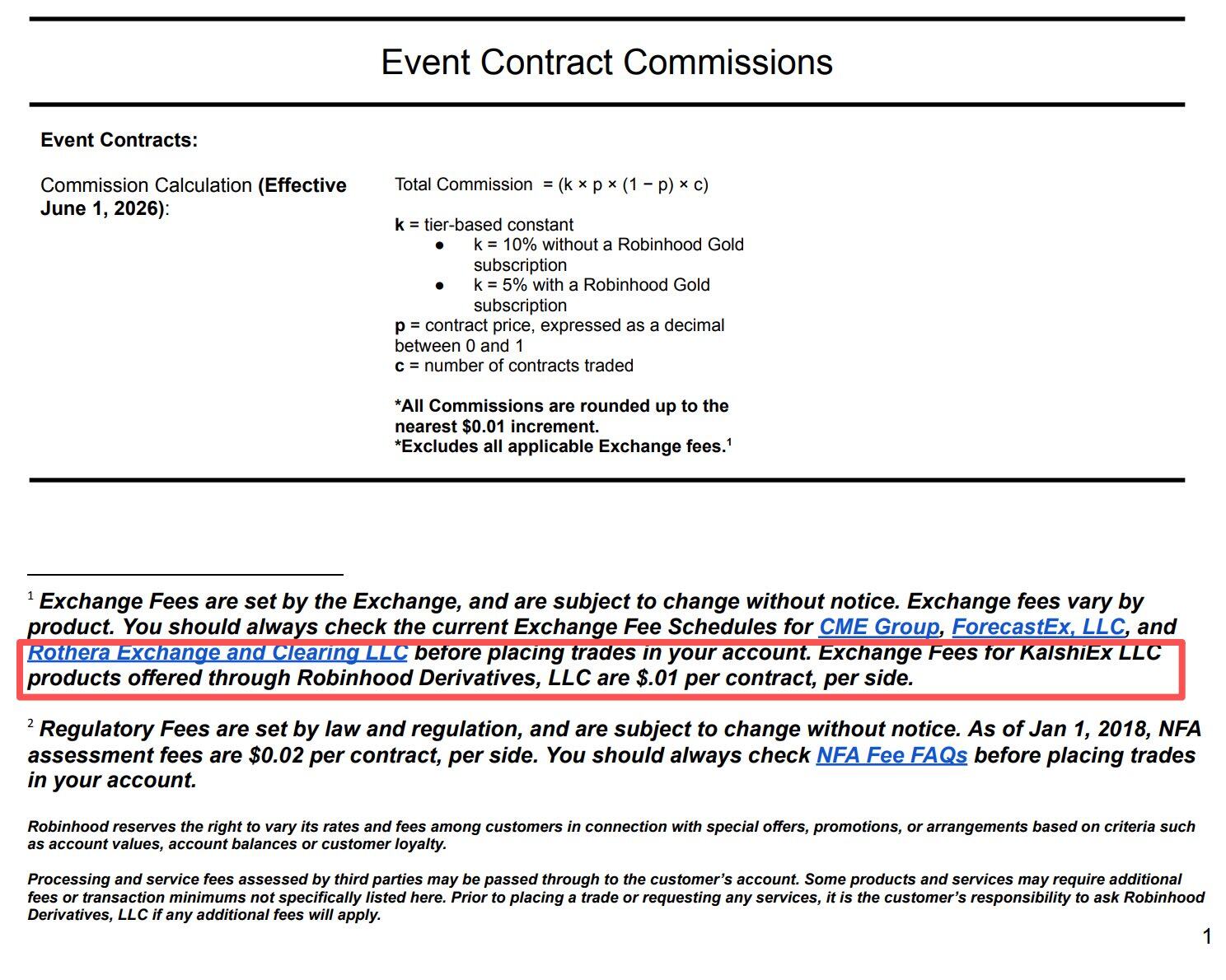

Subsequent stories also attest to the “win-win” outcome of this cooperation. Through Robinhod's channel end, Kalshi indirectly gained access to large quantities of users and running waterPiper Sandler, an analyst, has estimated that “transactions through the Robinwood channel account for about 25-35% of the total transactions of Kalshi”I don't know. These orders were eventually translated into the proceeds on the books of both parties - Robinhod would charge a separate fee of $0.01 per contract for each of the Kalshi contracts that were traded through that channel and then split with Kalshi (the exact proportion is not disclosed)。

THE Q1 FINANCIAL REPORT RELEASED AT THE END OF APRIL OF THIS YEAR SHOWS THAT THERE IS A LACK OF INFORMATION ON THE Q1 BUDGETThis year, Robinhood achieved 8.8 billion event contracts in Q1, leading to a 320 per cent increase in “other transaction revenue” over the same period, reaching $147 million。The projected market has become the brightest new engine in the Robinwood product line。

But recently, there have been some subtle changes in this relationship。

Robinhood's ambition: regaining the cake allocated to Kalshi

As the history of the Internet has proven on numerous occasions, it is not possible to find a solution to the problemWhen the channel has enough voice, it will not be content to do only the channel itself。Robinwood is no exception。

Although collaboration with Kalshi has also brought considerable revenue to Robinhod, Robinhod no longer meets today's ploughing programme as the forecast market becomes one of the fastest growing new businesses on the platform。

In the model of cooperation between the two parties, Kalshi was responsible for providing markets and infrastructure, and Robinhod was responsible for providing a flow of users and orders, but as the cooperation continued to deepen, he was able to make a differenceRobinhood is beginning to find that what is really scarce is perhaps not the market itself, but a user portal that he is firmly in control。After all, for most Robinhod users, they don't care whether the order is eventually made at Kalshi or at other platforms -- the user sees a trading entrance in Robinhod App, not the infrastructure provider behind it。

In other wordsRobinhod has always had one of the most important resources for predicting the market -- distribution capacity。Now that the user belongs to himself, why would the order go to someone else

In fact, just as Robinhod was quick to verify the forecast of market demand with Kalshi, another set of plan B was launched later。

In November 2025, Robinhod announced the establishment of a joint venture with Wall Street Quantified Trading Giant, Susquehanna, and plans to acquire a derivative exchange under the supervision of CFTC, MIAXdx. According to official accounts, the joint venture would in the future operate an independent futures and derivatives exchange and clearing agency, and forecasting the market was one of its priority directions. While the outside world saw it more as an infrastructure investment, it was only with further disclosure that it became clear that the goal of Robinhood was far from just finding new partners for predicting markets。

In January 2026, the transaction was officially completed. Robinhod and Susquehanna gained 90% control of the MIAXdx while taking over a complete set of CFTC regulatory frameworks, including the qualifications of Designed Contractor Market (DCM) and Derivatives Clearing Organization (DCO). ThenMIAXdx was renamed Rogera Exchange and its liquidation agency was renamed Rogera Clearing。

Here we goRobinhod already has the core elements needed to operate independently to predict the market, and what is missing is a mature product for Kalshi, but it is clearly not difficult for Robinhod, who is experienced in the development of Internet products。

The World Cup

In June 2026, after half a year of accelerated development, the Rotha product evolved, and Robinhood finally made an almost inevitable move -- moving the order that originally went to Kalshi into a self-control system。

Robinhood specifically chose an excellent initial battlefield for Rotha -- the World Cup。In terms of forecasting markets, the World Cup is undoubtedly one of the most fluid trading themes, whether it is winning, winning or winning, and the relevant markets are able to attract large numbers of new users to the trade in a short time. For the new platform that is just beginning in Rotha, there is nothing better than a cold-starting scene for the World Cup。

According to the official announcement of RobinhoodDuring the World Cup, which is a total of 104 games, some of the event contracts will be channelled to Rothera for matchmaking and settlement, including the results of a single World Cup, the final World Cup championships, and the total number of goals in a single game。This is also the first time that Robinhood has imported forecast market orders into its own trading system on a large scale, compared to its previous total reliance on the Kalshi model。

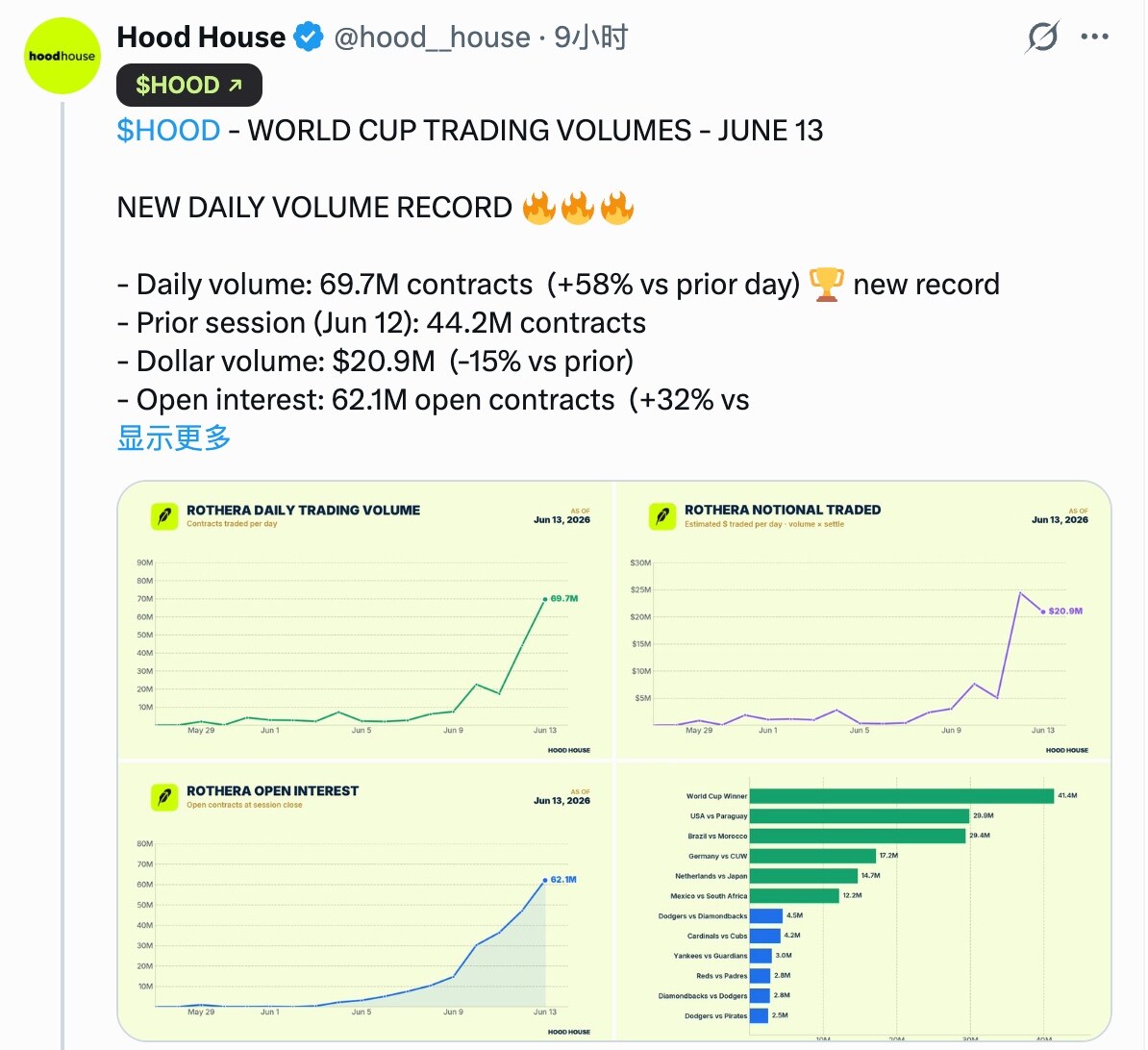

In terms of results, it is clear that Rothera seized this opportunity。According to data released by the tracking of Robinhood dynamic researched from the media, on 12 June, Rothera completed 44.2 million contractual transactions with a dollar equivalent of approximately $24.4 million; on 13 June, Rotha completed an additional 69.7 million contractual transactions with a dollar equivalent of approximately $20.9 million. While there is still a gap between these figures and the hundreds of millions of dollars in the hot market at Kalshi, this data performance has been sufficiently successful, considering that Rotha is in fact just a few days on the line。

For Robinhod and Kalshi, this means that the scales of cooperation between the two parties are already skewed。On the Robinhod side, the revenue from the fees that would have been shared with Kalshi can now remain more within its ecology; on the Kalshi side, this means that one of its most important growth engines has begun to show signs of relaxation。

And the World Cup, obviously, is just the beginning of the Rome encroaching on Kalshi. Looking further ahead, Robinhood will inevitably expand the reach of Rotha to more sporting events and economic, political and other topics, and those that originally flowed to Kalshi will be stopped by Rothera in turn。

Since Robinhod and Kalshi have never made public their share of the traffic, we are unable to know the exact number of the value of this interceptionBut considering that Robinhod has achieved $147 million in projected market-related revenues in Q1 alone, it is clear that the Q2 World Cup and the more distant mid-term elections could lead to larger-scale trading, in unit terms, which could be worth hundreds of millions of dollars。

Who controls distribution, who controls everything

Robinhod and Kalshi's move from allies to rivals once again explains a logic that has been repeatedly tested on the Internet market - Products are easy to make and traffic difficult to find; whoever controls distribution controls everything。

Over the past few years, it has been widely accepted in the market that Kalshi ' s core moat comes from regulatory licences, exchange qualifications and liquidity. So, whether a coupon like Robinhod, or a variety of media, community and traffic platforms, is essentially just a channel and a portal for Kalshi. I don't knowThe presence of Rothera attests to the fact that the product itself may not be the most important element in a time of serious homogenization. Really scarce, always users。

Where users are, liquidity is where it is; where it is, markets are where it is. When Robinhood has access to tens of millions of retail users, he is well placed to direct them to any trading place. For users, they do not care whether the order is finally made in Kalshi or in Rothera, and it doesn't matter who set the deal behind it or settle it, as long as the experience is not clearly different。

If the theme of the market industry for the last few years is the market struggle between Polymarket and Kalshi, then the theme for the next few years may turn into a channel war。Robinhood Incubation is essentially a reverse integration initiated at the market level in the direction of channels; and similar storytelling rates will continue to occur as more and more platforms with entry points become aware of the strategic value of forecasting markets. Whether it be an exchange, a voucher, a social platform or a media platform, it can become a new forecast market entry。

And when the entrance begins to take control of the market and the channel begins to have pricing rights, the ultimate winner in the market industry is probably not the platform for arranging orders, but the one closest to the user, who controls distribution。

This is true of the Internet age, as is the mobile Internet age. This time, there was no accident。