a16z's new fund-raising of $15 billion: how can it be the "best story-telling" vote

the key to raising $15 billion is that it is no longer just an investment, but a "super broker" connecting capital, founders, talent and markets。

Original title: a16z: The Power Brokers

Source: Not Boring

This post is part of our special coverage Syria Protests 2011

The author presses: this paper focuses on a 16z, which takes the opportunity of its new $15 billion fund to dig deep into its "non-traditional" core - the future of engineers' thinking and the potential of businesses (e.g. Databricks). The text incorporates performance data and classic cases, breaking down the evolutionary logic of its initial creation to manage over $90 billion in assets. If you want to understand how this "technology believer" is reshaping the rules of the industry, you can look into the text。

when a16z throws a pound of new $15 billion in information, the whole circle is once again shaken by it — someone flips out a few years of questioning his pattern and wonders where that money will go。

I TALKED TO ITS GP (GENERAL PARTNER) AND LP (LIMITED PARTNER) IN ORDER TO FIND OUT ABOUT THIS CONTROVERSIAL INSTITUTION, AND I TALKED TO THE FOUNDERS OF THE POST-INVESTMENT ENTERPRISE, WHO VALUED OVER $200 BILLION, AND WENT THROUGH THE RETURN DATA ON THE FUND SINCE ITS INCEPTION。

but i want to ask more than to argue "a16z is wrong": what are the smart people who used to make the right judgment? of course, i was an encrypted consultant for a16z, and i was on the same list of shareholders as the core person, not exactly an objective observer。

But I don't want to judge whether this $15 billion is worth voting -- the agency LP has already voted in real money, and the answer is ten years. I'd like to show you how a16z can be the best storyteller in the world. How does the future lie in its mouth

"I live in the future, and now it's over; my very existence is a gift, so walk away. I don't know

— Kanye West, Monster

"IT'S TOO LOUD TO SAY AND DO MORE IN POLITICS," "NOT TO AGREE WITH ONE OR TWO OF ITS RECENT INVESTMENT PROJECTS," "TO QUOTE THE POPE'S SOCIAL PLATFORM, IT'S TOO BAD" AND "THE FUND IS SO BIG THAT IT CAN'T OFFER A REASONABLE RETURN TO THE LP."

these sounds, a16z heard almost 20 years ago。

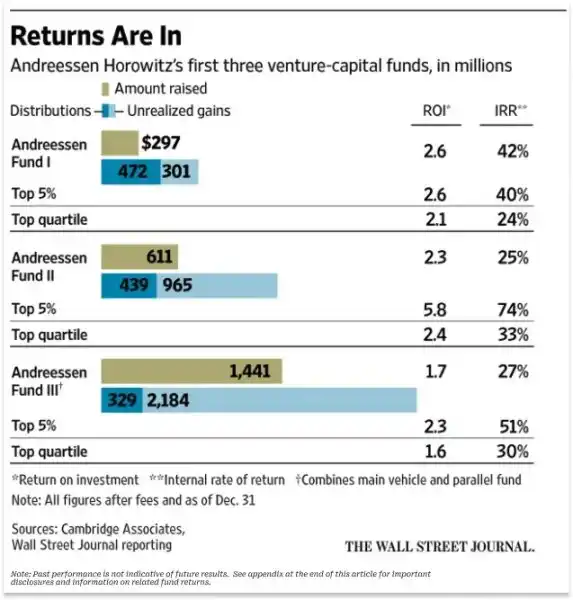

For example, in 2015, a New Yorker journalist, Tad Friend, had breakfast with Marc Andressen (a16z co-founder and general partner) to write " The Way Forward " . Prior to that, Friend had just heard from a peer-to-peer voice questioning that the a16z fund was too large and its shareholding ratio was too low [1], and that the total return of the top four funds would have to be 5-10 times greater, with their total investment portfolio valued at $240-48 billion。

Friend wrote, "When I tried to check this data with Andressen, he made an impudent gesture and said, "Bullshit." We have a whole set of models -- we're gonna catch elephants and fish."

Remember this picture, because next you might have similar questions, and it's probably the same reaction that Andrease has。

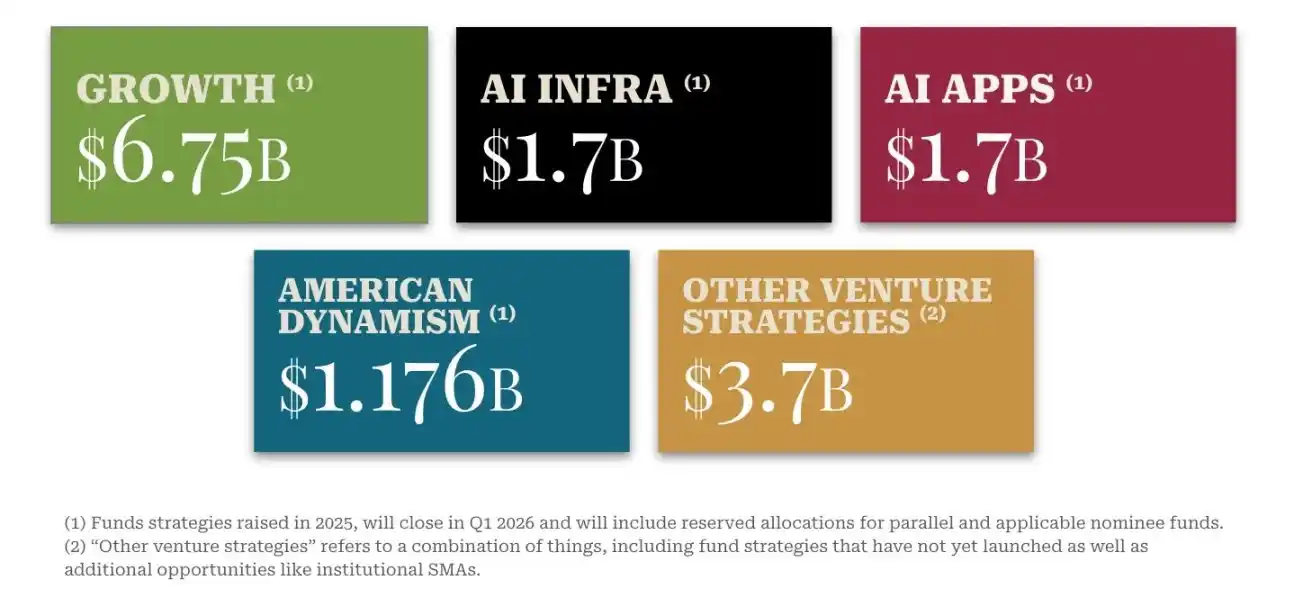

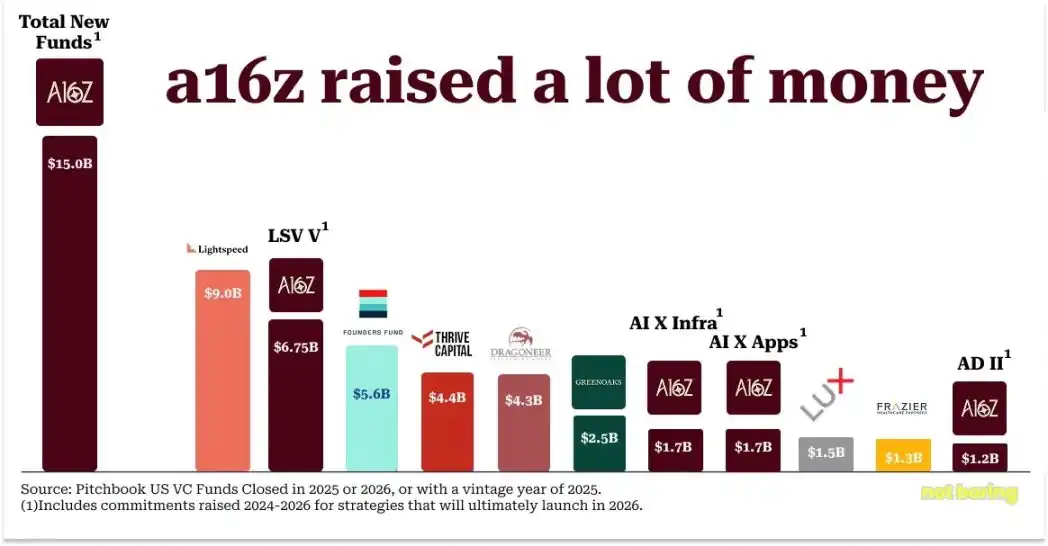

Today, a16z announces all its investment strategies to raise $15 billion, and the size of managed assets under its supervision (RUUM) is over $90 billion。

a16z several fund strategies raised in 2025 and corresponding scale of funding

In 2025, the market for wind investment was dominated by a small number of head agencies, while a16z raised more money than the second-and third-largest Lightseed ($9 billion) and Founders Fund ($5.6 billion)[2] combined。

in the worst investment environment in the last five years, a16z 2025 raised more than 18 per cent of total investment in the united states [3]. it usually takes an average of 16 months for a venture fund to collect, and a16z takes just over three months from start-up to admission。

If divided, a16z has four funds that can be part of the industry-wide fund-raising Top10 in 2025: the later wind investment fund LSV V ranks second, the AI Infrastructure Fund X ranks seventh alongside the AI Application Fund X, and the American Dynamic Fund AD II ranks tenth。

2025-2026 Comparison of the size of U.S. wind investment funding

it may be argued that so much money cannot be reasonably configured to achieve excess returns. but i guess the answer to a16z is probably, "bullshit." after all, they're always hunting elephants and chasing big fish

Today, the portfolio of all a16z funds covers 10 of the "Value Top15 Private Enterprises": OpenAI, SpaceX, XAI, Databricks, Stripe, Revolut, Waymo, Wiz, SSI and Anduril [4]。

in the past decade, a16z has invested 56 unicorn enterprises [5] through a flag fund, exceeding any institution in the industry。

ITS AI PORTFOLIO COVERS THE TOTAL VALUATION OF UNICORN ENTERPRISES, ACCOUNTING FOR 44 PER CENT [6] OF THE ENTIRE INDUSTRY, AND ALSO RANKED FIRST。

in 2009-2025, a16z led investments in the early rounds of 31 "finally valued businesses over $5 billion", 50 per cent more than the sum of the second and third institutions。

Not only do they have a full set of models, they now have more solid endorsements of performance。

as mentioned earlier, a16z has been questioned by peers about the $240-48 billion value of the combined valuation of the first four funds to meet the target. in fact, the total portfolio valuation of a16z fund 1-4 (based on withdrawal or the latest post-investment valuation) amounted to $85.3 billion [7]。

a16z total portfolio value of the first four funds

And it's just a withdrawal valuation -- Facebook alone, a company, and the market value has since increased by $1.5 trillion

there's a lot of drama going on: a16z, the next seemingly crazy bet in the future, and people who know how to do it say it's stupid, but a few years later, it's not stupid

In the wake of the 2009 global financial crisis, a16z raised $300 million in fund No. 1 and introduced the concept of "operational support platform for the founders". Ben Horowitz (co-founder and general partner of a16z) recalled: "We talked to a lot of people, who mostly said it was a stupid idea to stop doing it, and said it was a model that had been tried before, and it didn't work. Today, almost all of the head throws have similar platform teams。

In 2009, a16z took $65 million from this fund to buy Skype from eBay at $2.7 billion with institutions like Silver Lake Capital. At the time, "Everyone said it couldn't work out because intellectual property was too risky" -- after all, eBay was in a lawsuit with Skype's founder about technical belonging. Less than two years later, Microsoft bought Skype for $8.5 billion, and Ben, in a blog, recalled the challenges at the time [8]。

In September 2010, Marc and Ben raised $650 million in fund No. 2, followed by large-scale late investments in businesses such as Facebook ($50 million, with a post-investment valuation of $34 billion), Groupon ($40 million, with a post-investment valuation of $5 billion), Twitter ($48 million, with a post-investment valuation of $4 billion) and a bet on the IPO window to be opened. The Wall Street Journal, in its book "The New Noble Silicon Valley " , wrote that its peers were dissatisfied with this, arguing that "the private trading of shares is not a matter for which to vote" (this is a common practice today, which is still very new and has not even been labelled a "secondary trading"). Benchmark's partner Matt Cohler once said, "Many and oil futures make money, but that's not what we should do. What happened? In November 2011, Groupon valued IPO at $17.8 billion; in May 2012, Facebook valued IPO at $10.4 billion; and in November 2013, Twitter first-day collections valued at $31 billion。

In January 2012, Marc and Ben raised $1 billion in fund 3 and $540 million in parallel opportunity funds. At this time, the challenge became the common "too big": a16z raised 7.5 per cent of total US investment in that year, while the industry was generally underperforming. The 2014 Harvard Business School case study on a16z mentioned that a 2012 Kaufman Foundation report stated: "The return from windfall industry has been poor for more than a decade. According to Cambridge Association data, the average annual wind projection rate of return in 2012 was only 8.9 per cent, well below the 20.6 per cent of the generic 500 index. The legendary Bill Draper once said, "The consensus in the Silicon Valley industry is that too many funds are chasing too few really good businesses. This is still true today。

In 2016, the Wall Street Journal published an article by Acquired podcast David Rosenthal, who described it as "manifestly a black letter of peer approval" under the title "Andressen Horowitz (a16z) Fund returns lag behind the top of the wind." At that time, a16z's three funds were established seven years, six years and four years, respectively, and the article states that although Fund No. 1 was 5 per cent ahead of industry, Fund No. 2 was only 25 per cent ahead, and Fund No. 3 was not even 25 per cent ahead。

a16z performance of the top three funds and comparison with industry head level

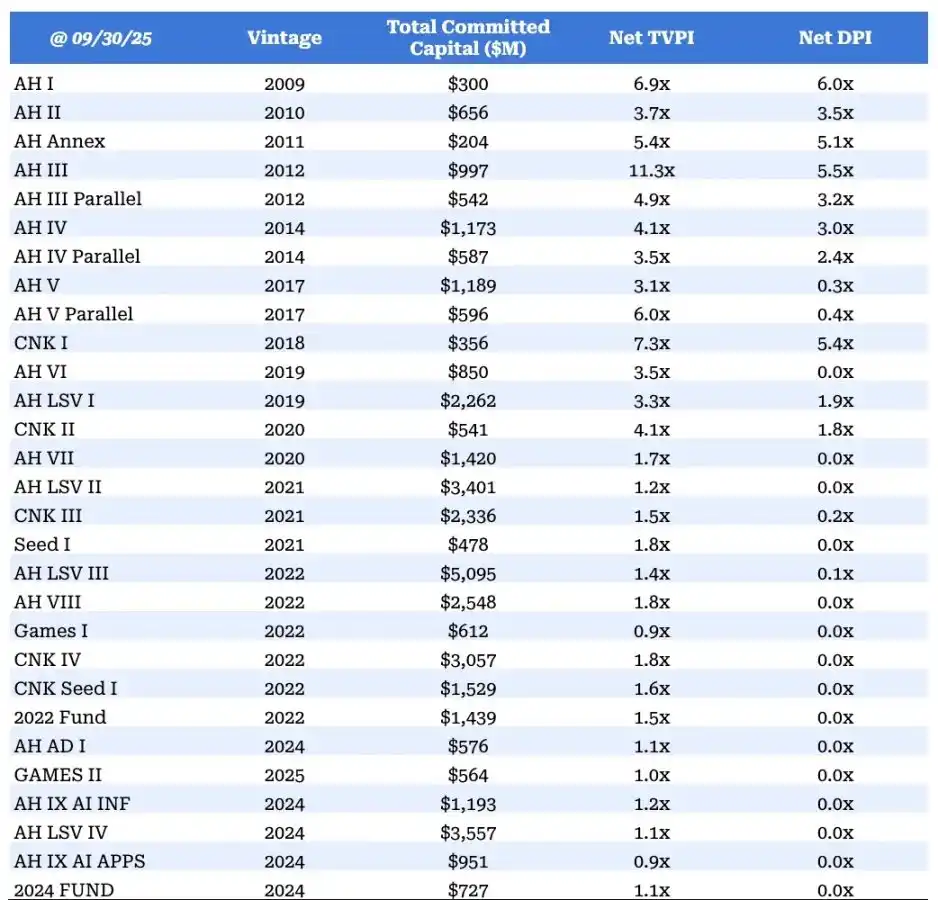

BUT NOW, LOOKING BACK, THIS 3RD FUND IS A LEGEND: AS OF 30 SEPTEMBER 2025, THE NET TVPI (MULTIPLIER OF THE TOTAL VALUE OF CAPITAL INVESTED) AFTER DEDUCTION OF COSTS WAS 11.3 TIMES; IF PARALLEL FUNDS ARE INCLUDED, THE NET TVPI IS 9.1 TIMES。

The portfolio of Fund 3 includes: Coinbase (with a total allocation of $7 billion for a16z LP), Databricks, Pinterest, GitHub and Lyft (although Uber was missed, one missed "offence" did not cover the "false" of multiple accurate investments). I think this fund is called "one of the most successful large investment funds in history." After the third quarter of 2025, the valuation of Databricks (currently a16z maximum hold) rose to $134 billion, which means that Fund 3 performance is still on the rise (assuming that the other hold has not depreciated). From Fund 3 and parallel funds alone, a16z has allocated $7 billion net to the LP and there are still nearly equal unrealized gains to be realized。

A significant portion of these unrealized gains came from Databricks. When the Wall Street Journal failed a16z in 2016, the big data company was still small, with a few months to estimate at $500 million. Today, Databricks accounts for 23 per cent of net assets (NAV) of a16z of all funds。

The name "Databricks" is often heard as long as a16z is contacted. It is not only the largest holder of a16z (perhaps the third largest project in the entire windfall industry) but also the living case of a16z's "best operating model"。

Databricks and a16z operating formula

Before talking about Databricks, there are several key points about a16z that need to be understood。

first, a16z was created and operated by engineers — not only the founders, but also the “founders of engineer origin”. this affects the design logic of institutions (for scale and network effects) and determines their criteria for choosing markets and enterprises。

second, at a16z, the "second in the investment industry" is probably the biggest "inventory crime". if the winner is missed early, there will be a vote later; but if the winner is second, the chance to vote for the winner will be completely lost — even if the winner is still alive。

third, once a16z identifies a company as a "racing winner", the classic operation is to "show far more money than the other side expected." this practice is often ridiculed in practice, but they persist。

these three points have not changed since the beginning of a16z。

In the early part of the 21st century, a16z was created a few years ago, when "big data" was the windfall, while the dominant industry's big data framework was Hadoop. Hadoop, using the MapReduce programming model developed by Google, assigns computing tasks to low-cost general server clusters rather than to expensive specialized hardware, which can be described as a "big data democratization" driver. Since then, a number of businesses around Hadop have emerged, and industry investment peaked in 2014: Claudera, established in 2008, raised $900 million, and the total financing of Hadoop-related businesses in 2008 increased five times more than before, to $128 billion; Hortonworks, which Yahoo split, was also IPO in the same year。

there's a lot of data coming in, but there's nothing going on。

a16z's "z" - Ben Horowitz - does not care about Hadop. Before becoming Chief Executive Officer LoudClaud/OpsWare, who was a computer proficient, he argued that Hadop would not be a mainstream structure: "Programming is complex, difficult to manage, and not adapted to future needs — MapReduce calculates every step by which intermediate results are written on disks, and for such an iterative computational task as machine learning, the speed is crazy. I don't know

So Ben chose to avoid the Hadoop heat. Jen Kha told me that at the time, Marc was still throwing up Ben:

"We must have missed it! "Marc was in such a hurry。

But Ben said, "I don't think this is the next structural change. # I don't know #

Then Databricks showed up and Ben said, "This may be right. And then, of course, he took it all. I don't know

Databricks was born just at the time and near the University of California at Berkeley。

During the Iranian revolution in 1984, the Ali Ghodsi family fled Iran and moved to Sweden. Parents bought Ali a Comodore 64 computer, which he designed for himself, and even got an invitation from a visiting scholar from the University of California at Berkeley。

At Berkeley, Ali joined the AMPLab laboratory and worked with eight researchers, including the mentors Scott Shenker and Ion Stoica, to land the ideas of the doctoral student Matei Zaharia and develop a Spark - an open-source large data processing engine。

Spark is designed to "repeat the functions of a technology giant using a neural network without a complex interface." It created a world record of data sequencing, and Zahraia's paper received the best annual computer science paper. However, according to academic practice, they are almost unusable when they open the code free of charge。

Since 2012, these eight people have gathered to discuss and finally decided to form a company around Spark, named Databricks. Seven of them became co-founders and Shenker acted as resource persons。

Databricks, co-founder of Ali Ghodsi, sits in the middle of the front, Forbes

The team initially felt that it needed a little money, but not much. Ben, in an interview with Lenny Rachitsky, recalled:

When I met them, they said, "We need to raise $200,000." I knew at the time that they had Spark, and the competition was a Hadoop firm that already had huge financial support. And Spark is open-sourced, timeless. I don't know

Ben is also aware that, as a scholar, this team is "easy to meet a small target". He said to Lenny, "In general, if the professor could make a $50 million valuation, he would be a hero on campus. I don't know

So Ben gave the team a "bad news": "$200,000 check, I can't write." I don't know

"I can write a check for $10 million." I don't know

His argument is: "In order to start a business, you have to do it seriously and do it with all your energy. Otherwise, you might as well stay in school. I don't know

The team decided to drop out. This further increased investment, a16z leading the A round of Databricks, with a post-investment valuation of $44 million and a16z holding 24.9 per cent。

This first encounter — for 200 thousand Databricks and 10 million for a16z — lays the tone for cooperation between the two parties: once a16z votes for you, it will be “full faith in you” and push you to “target larger targets”。

When I asked Ali about the impact of a16z, his attitude was very clear: "I don't think that without a16z — especially without Ben-Databricks — there is no such thing as a 16z. I don't think we can make it now. They really believe us. I don't know

In the third year of the company's existence, only $1.5 million was collected. "We couldn't be sure of our success at the time," Ali recalled, "The only person who really believed that this company would be worth a lot in the future is Ben Horowitz. His confidence is stronger than that of all of us, and, indeed, much stronger than my own. He deserves high praise for that. I don't know

It's great to have faith, but when you have the ability to make it self-fulfill it, it's worth more。

In 2016, for example, Ali was trying to work with Microsoft. In his view, the market's demand for "access to the Azure cloud platform for Databricks" was extremely urgent, and that cooperation should have been logical. He asked a few of his partners to help out, hoping to get in touch with Microsoft CEO Satya Nadella — they did help, but they all ended up “drowning in the process of the CEO's assistant。

Subsequently, Ben personally established a formal channel of communication for Ali and Satya. "I received an e-mail from Satya, in which he said, "We are very interested in working together in depth," and Ali said, "He also copied his deputy and his subordinate. In a matter of hours, 20 e-mails were received in my inbox. The senders were Microsoft employees who had tried to reach out to them, but they all said, "When can we meet and talk about this?" That moment I realized, "This is different, this cooperation will work. I'm sorry

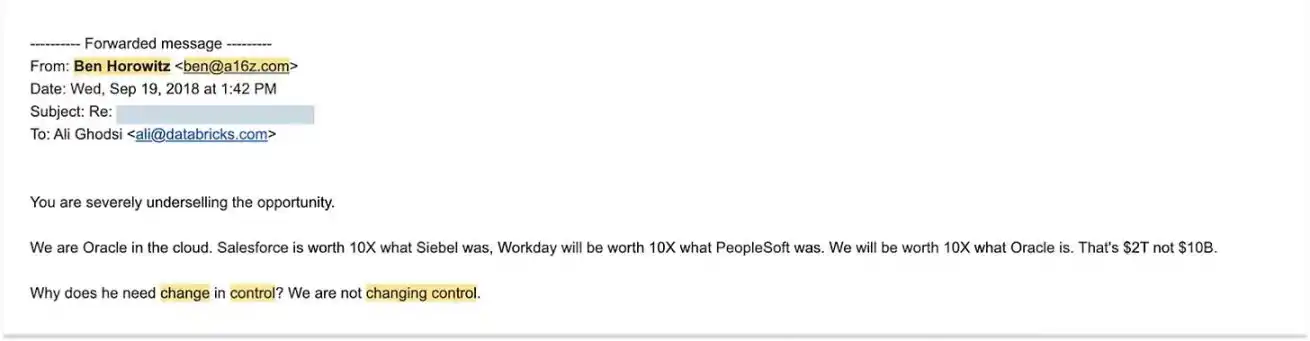

In 2017, for example, Ali was trying to recruit a senior sales manager to accelerate the growth of company operations. The supervisor proposed to add a "change of control clause" to the contract. — In essence, if the company is acquired, the shares he holds can be realized more quickly。

So Ali asked Ben to help convince the supervisor that the Databricks valuation was "at least $10 billion." Ben, after communicating with the supervisor, sent Ali an e-mail:

Ben Horowitz email to Ali Ghodsi, 19 September 2018, provided by Ali Ghodsi

"You seriously underestimated this opportunity。

We'll be Oracle in cloud computing. Salesforce's valuation is 10 times that of Siebel, and Worldday's valuation is 10 times that of PeopleSoft, and our valuation is 10 times that of Oracle - which means our target is $2 trillion, not $10 billion。

Why does he need a change of control clause? We will not have a change of control at all. I don't know

This is perhaps one of the most vocal corporate e-mails in history, particularly given that the Databricks ' collection rate (annualized) was $100 million, valued at only $1 billion, while the company ' s operating rate now exceeds $480 million, reaching $134 billion。

"They can see the full potential of one thing," Ali told me, "When you're in it, every day dealing with day-to-day business, it's all a challenge — the inability to negotiate, the repression of competitors, the imminent depletion of funds, the fact that no one knows your company, the fact that people are still leaving their jobs — it's hard for you to look at things like that in the long term. But they will appear at the board meeting and tell you, "You will conquer this world." I'm sorry

They were right in their judgement, and that belief paid them well. In summary, a16z participated in all 12 rounds of Databricks financing, of which 4 were awarded by a16z. It is precisely because of investment targets such as Databricks that the fund AH 3 from which a16z originally invested is doing so well; at the same time, Databricks is one of the central drivers of the larger “late-stage venture capital fund 1, 2, 4” to generate gains。

"First and foremost, they really care about the company's mission," Ali says, "I don't think Ben and Marc will be the first to see it as an investment that seeks a return, and the return on investment is only a minor one. They are the believers of science and technology, and they want technology to change the world. I don't know

If you can't understand Ali's assessment of Marc and Ben, you can never really understand a16z。

what is it

a16z and non-traditional venture capital funds. On the face of it, it is clear that the company ' s fund-raising exercise was the largest venture capital since the $98 billion Vision Fund in 2017 and the Vision Fund II in 2019.[8] This is completely incompatible with the characteristics of traditional investment. But even so, the soft money vision fund is essentially just a "fund", not a16z。

Of course, a16z raised funds and needed to generate returns for investors. It must be extremely successful in that regard, and it has so far done a remarkable job. Not Boring has a 16z return data on the Fund to date, which we will share below。

but first, we need to be clear: what is a16z

a16z is a "technology faith community". all it has done is to promote the birth of more advanced technologies and thus to build a better future. the company firmly believes [9]: "technology is the glory of human ambitions and achievements, the vanguard of progress, and the means of realizing human potential. all actions are based on this core belief. it has strong confidence in the future and is committed to that belief by betting on the resources of the company as a whole。

a16z is an "institution". it is a business and a company, built on the goal of scaling up and improving itself in the process of scaling up. i believe that many of the features of the institution are not available in the traditional fund, as described below. i believe that the positioning of the "institution" fund is precisely the most contradictory aspect of the venture industry's self-awareness: the industry provides the most scalable products (money) to the most scalable firms (tech start-ups), but the industry itself is considered “not to be scalable”。

This distinction in the positioning of the "Institution" fund is derived from a16z ' s general partner (GP) David Haber. He was one of the most "financial circles" in the team and called himself "a learner of business models of investment agencies". He explained that “the Fund's objective function (core objective) is to generate the greatest incidental gains in the shortest possible time, with the minimum human capacity, and that the goal of the institution is to create both excellent returns and competitive advantages that have a multiplier effect. What we want to think about is how to make companies stronger, not weaker, in the process of scaling up. I don't know

a16z operated by engineers and entrepreneurs. traditional asset managers typically compete for a larger share of a fixed “cake”, while engineers and entrepreneurs make the “cake” itself bigger by building better systems and promoting system size。

a16z is the "power in power in time" and the "body for the future". at a time of greater ambition, the institution would see itself as being on par with top global financial institutions, governments. it has stated that the goal is to be "morgan chase of the information age," but in my view, it still underestimates its true ambitions. if the government serves a "specified space range", then a16z serves a "the vast time dimension of the future". venture investment is only one way that it finds — one way in which it can have the greatest impact on the future, and the business model is best suited to the logic of “profits for the future”。

a16z creates and "sells" influence. it builds its influence through scale development, cultural building, human networks, organizational set-up and past success stories; it then gives it to science and technology start-ups in its portfolio — mainly through marketing support, marketing, talent recruitment, government relations maintenance, etc. however, in the words of its founders, a16z would "help as much as it can" and it seems to be much more than that。

if you're going to design such an institution – which is convinced that “technology is penetrating beyond the boundaries of traditional technology industries” and that “technology will eventually be made in all fields” – then you're going to build an enterprise that sells “winner power” to thousands of companies that “may form the core of the economy”. and i think that the structure that you eventually built would be very similar to a16z。

Because those companies that may form the core of the economy in the future tend to be small and weak in their initial stages. They were initially scattered in various fields, with different objectives and competitors, and often even competing with each other; at the same time, they were faced with giants who dominated the current market and were reluctant to yield to new entrants. A start-up company, however bright it may be, may not be able to recruit the best recruiters (and thus attract the best engineers and executives); may not be able to advocate for a level playing field for itself through policy; may not have enough audiences to allow its ideas to be heard; and may lack sufficient credibility to sell its products to government departments and large-scale enterprises that have been marketed to “commit to bring the next wind”。

For any start-up company, it would be illogical to invest billions of dollars to build these capabilities, but only to serve itself; but if those capabilities were distributed to "all these start-ups" and covered "a market worth trillions of dollars in the future", these small companies could suddenly own the resources of large companies. Their success or failure will depend only on the merits of the product itself, and they can drive the future in the way it should。

What would be the effect of combining the agility of start-up companies with innovation, and the influence and strength of the “time-field power holders”

that's what a16z has been trying to do... such an attempt has been made since it was a founding institution。

Why did Marc and Ben start a 16z

In June 2007, Marc wrote an article entitled " The One Important " [11], which is part of the Pmarca Entrepreneurship Guide [12]. On the face of it, the article is a proposal for a technology start-up company, but now it looks more like an "Operational Manual for the Creation of a16z". The core of the article answers the question: which of the three core elements of starting a company — team, product, market — is most important

Entrepreneurs and venture investors usually say "teams are the most important" and engineers say "products are the most important"。

"I personally support the third view," Marc wrote, "I think markets are the most important factor in the success or failure of start-ups. I don't know

Why? He explains:

"In a high-quality market — where there are a large number of real potential customers — the market will `pull' the starters to produce

On the contrary, in a bad market, even if you have the best product and the best team in the world, you are doomed to fail

In tribute to the former partner of Benchmark Capital, Andy Rachleff, I hereby propose the "Rachleff law of the successful founding company":

The primary cause of corporate failure is the lack of quality markets。

Andy says this:

Top teams meet bad markets and they win

Bad teams meet high-quality markets and they win

The highest-class teams meet high-quality markets before they produce extraordinary achievements. I don't know

I think that what Marc and Ben see in the venture capital industry is a "good market" (and no one was aware of how good it was), which is full of "bad teams" (and no one was aware of how bad they were)。

Between 2007 and 2009, Ben and Marc have been thinking about what to do next. They have been very successful technology entrepreneurs — both of them are holding on to a lot of energy despite success; and because of that success, they have the capital to “do not look at the human face” so that they can play their part without fear。

But what exactly is to be done

Whether as an entrepreneur or later as an angel investor, Marc and Ben have been dealing with many unprofessional venture capitalists who feel that "competing with these people may be interesting"。

"As far as I'm concerned, Marc never did it for money," David Haber told me, "He's been rich since he was about 20. In the beginning, he did it more probably for the purpose of "show Benchmark or Redwood capital." I don't know

The venture capital industry also has a character, and at the height of the economic downturn triggered by the global financial crisis (GFC), almost no one is aware of this: it is probably the world ' s best market. And this is critical for Marc。

Of course, not all venture capital institutions are bad. The two companies that Marc is trying to "grow some light" -- Redwood Capital and Benchmark -- are actually very good. Peter Thiel, for those who wanted to keep the management, founded the Foundations Fund as early as 2005, at a time when he was in the investment phase of the Second Fund (FF II) in 2007 – as Mario wrote, the fund ended up with a performance of $18.60 cash return (DPI, investment capital dividends)。

However, compared to today, the then-risk investment industry as a whole was still a “Lack, Closed, Manual” industry。

Marc used to tell a story: in 2009, when Ben and he were thinking about creating a16z, he met with a G.P. from a top wind projector, who compared the investment start-up company to "from a swing sushi conveyor belt to get sushi." According to Marc, this GP said to him:

"The venture capital business is like going back to Sushi for dinner. All you have to do is sit on Sand Hill Road, Silicon Valley, and the start-up company will come. It doesn't matter if I miss one, because the next sushi will soon pass. All you have to do is sit and watch Sushi pass by and reach out and grab a piece. I don't know

Marc explained in Uncapted that "if the goal is simply to `maintain the good days', it will also work if industry ambitions are limited." I don't know

But Marc and Ben have more ambitions than that. In the company they are about to set up, it would be the biggest mistake to "lost a quality project" — that is, not to invest in a good company. This is no small matter because it is clear to them that, as the market expands, the size of the large technology companies becomes far greater than they can imagine。

"A decade ago, about 50 million Internet users, with fewer broadband connections," Ben and Marc wrote in their April 2009 fund-raising memorandum, "A16z Fund I," that "Internet users now number about 1.5 billion, many of whom have broadband connections. Thus, the potential of the most successful enterprises in the industry, at both the consumption and infrastructure levels, is likely to be far greater than that of the most successful science and technology companies of the previous generation. I don't know

At the same time, the cost of starting a company has been significantly reduced and the process has become simpler — meaning that more start-ups will occur in the future。

In their letter to potential limited partners (LPs), they wrote: "The cost of developing a new technology product and entering the market at least in the form of a test version (beta) has fallen dramatically over the past decade; today it is usually only $500,000 to $1.5 million, compared to $5 million to $15 million a decade ago. I don't know

Finally, as start-ups shift from "tool providers" to "players directly competing with industry giants", their own ambitions are growing – meaning that all industries will eventually become science and technology industries, and that all industries will become larger。

That's why the "market" was so good at that node. Marc continues:

From the 1960s to around 2010, the venture capital industry had a set of fixed "playbooks" ... The company at the time was essentially a "tool provider" — the company that sells thorium and shovels — large hosts, desktop computers, smartphones, laptops, Internet access software, SaaS (software or service), databases, routers, switches, disk drives, text-processing software, all of which were tools。

Around 2010, there was a permanent change in the industry ... The most successful enterprises in the field of science and technology are increasingly those that have entered the traditional sector directly and competed with existing giants. I don't know

in the early days, a16z was "overpricing" for the company? or did the pricing then sound relative to the company ' s anticipated future potential

looking back now, it is easy to assert the latter; but the impressive thing about a16z is that they had that judgement before it happened。

As they have written: Every year about 15 technology companies eventually earn $100 million a year, and these companies generate 97 per cent of the total market value of the open market in which all companies were founded that same year — now known as Power Law. In that case, they must invest as much as possible at all costs in those companies that have the potential to become one of the 15 companies; then, in those companies, double and double the investment of the winners。

for this to happen, it is not enough for two investment partners alone — a16z must build a company in a way that is “unlike all its peers”。

Thus, after elaborating on the basic investment terms of the AH-1 fund (targeted at $250 million, of which $15 million would be funded by ordinary partners), Ben and Marc outlined the company’s core strategy。

AH-1 FUND-RAISING MEMORANDUM."

Even now that the company is much larger than the "two partners" and that ambition is no longer limited to the "first five" of the industry, they are still implementing this strategy。

a16z three stages of development

in my view, a16z's preposterous belief in the future and his asymmetric determination has always been its core competitive advantage throughout the company's development history since the inception of the fund. it is this differentiated characteristic that gives rise to all other competitive advantages。

As the ambition, resources, size and influence of companies grow, the ways in which they use this advantage and diversify are also evolving。

Phase I (2009 - approximately 2017)

in the first phase of a16z (2009 - about 2017), the core insight is that if "software is devouring the world", the top software company will have far more value than everyone would have valued at the time。

with this conviction, a16z has undertaken three initiatives that have succeeded in gaining top five investment companies from new entrants to the industry:

Pay for the high price of the transaction:As noted earlier, some of the transactions entered into by the early fund a16z were considered by many peers at the time to be overpriced or out of line. In Acquired's podcast, Ben Gilbert said, “There is widespread criticism that they are ‘smuggling money for fame’ and crowding into quality project camps through high-priced investments”, but at the same time he pointed out that this practice was justified at the time and said, “Is it true that today there are people who think that a16z is overvalued for any project that was invested between 2009 and 2015?” The answer is absolutely no. As Ben Horowitz explained in the 2014 case study of Harvard Business School (HBS): "Even in the face of billions of dollars, investors may have underestimated the potential of these companies." This "underestimation" is the opportunity of a16z。

In this post, we have been able to build a business infrastructure that is perceived by others as "waste":form a full service team, hire partners, set up an executive briefing centre... in the view of the fund managers at the time, these initiatives were all “additional costs” that would be costly. these inputs are justified, however, if they are convinced that companies in the portfolio can grow into industry poles for "defined goods" and require firm-level strength to achieve this goal. a16z this is a setup for the future - in the future, start-ups must have the image of a mature business in order to win a cooperative order from the fortune 500。

The technology founders are seen as scarce resources:At the same time, it is a bet that, because of the lower cost of starting a company and the lower threshold, even in the absence of traditional management experience, technocrats have the capacity and are bound to create more influential enterprises. Thus, a16z has done everything in its power to attract and support such founders by introducing the model of the Innovator Broker CAA into the industry. Today, "friendly to the founders" has become a popular concept in the industry, but at that time it was undoubtedly a very innovative initiative。

it is worth noting that, in the first phase, a16z's most central objective is to invest in the "right companies" and to reap the benefits of these companies as they grow to the desired level of success. of course, they will also focus on supporting the founders, but in essence, at the heart of this phase is the opportunity to seize the arbitrage of valuation。

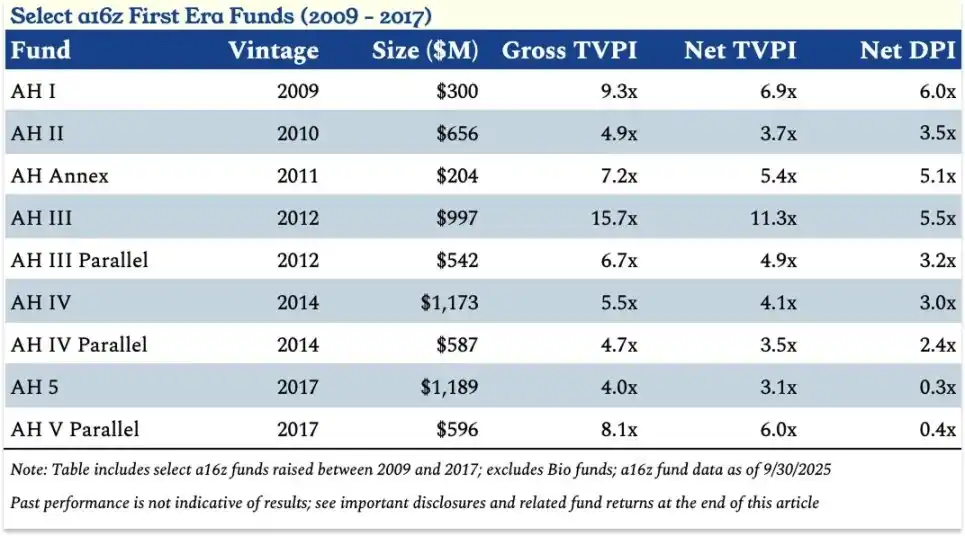

a16z core data for 2009-2017 (phase i)

a16z Fund No. 3 (AH III) is prominent because of its simultaneous investments in Coinbase and Databricks, but is even more noteworthy for its "continuing" performance。

"As a limited partner (LP), we would like to see the Fund achieve a three-fold (net) total value-to-cash capital ratio (TVPI) on a sustainable basis, with occasional more than five-fold (net) TVPI performances, and a16z just as it did, as VenCap's chief investment officer, David Clark, said (who has served as his LP since a16z third fund), "a16z is one of a few companies that can deliver such performance on a sustained and large scale over the long term. This can also be seen from the above-mentioned performance data。

if, at this stage, a16z is willing to “high-priced” and “cross-border investment like investment in pork futures” in order to create brand reputations and wait for long-term returns, in the short term the cost of such “paying” does not seem to be high。

Phase II (2018-2024)

in the second phase of a16z (2018-2024), the core conviction was changed to the belief that head enterprises would be larger than everyone expected, that they would remain private for longer and that technology would be more "absorption range" of the industry than others would realize。

it is in this belief that a16z has taken three initiatives to jump from top 5 companies to industry leaders:

Raise larger funds:In the first phase, a16z raised $6.2 billion through 9 funds alone, while in the second five years it raised $32.9 billion through 19 funds alone. The traditional industry consensus is that "the larger the fund, the lower the return," but a16z suggests the opposite: If the final value of the head enterprise becomes higher, then more capital is needed to maintain a meaningful shareholding ratio in multiple rounds of finance. The worst case scenario for windfall investments is either "missing the head enterprise" or "inadequate equity in the invested head enterprise". And Marc used to say, “You can only lose the principal of the input, or double it, but the ceiling is almost unlimited.” I don't know

To break the "single fund" model and diversify the layout:In the first phase, a16z is mainly raising core funds, accompanied by subsequent advanced funds. Although each of the general partners (GPs) has its own area of focus, all of the PPs invest in the same funds. In addition, a16z has raised a fund for biotechnologies - because the field of biotechnologies is very different from other fields. This paper will focus on a16z of wind investments in non-biotechnology and health。

After the second phase, a16z began to implement the "decentreization" layout: in 2018, under the leadership of Chris Dixon, a16z launched the first fund focused solely on encrypted money, CNK I; in 2019, the company hired David George to lead the creation of a special Late State Ventures (LSV) and raised the largest fund at the time, the LSV I, totalling $22.6 billion, about twice as much as a16z. During this period, a16z raised new funds around core tracks, encrypted currency, biotechnologies, LSV, and in 2021 launched a special seed fund (AH Seed I, $478 million), a special game fund (Games I, $612 million) in 2022, and a first cross-strategy fund (2022 Fund, $1.4 billion), which allows LP to invest proportionately in all funds in the same year。

Importantly, while individual funds can draw on corporate pooled resources (e.g., investor relations teams), each fund has formed an exclusive platform team covering marketing, operations, finance, campaign planning, policy research, etc. to meet the needs of its founders in specific vertical areas。

Extension of hold period:In the second phase of a16z development, the head enterprise began to remain private for longer and raised more funds in the private market — both “first-market financing” for company operations and “second-market transactions” to provide mobility for employees and early investors. When a16z bought the last second market shares in Facebook, Matt Cohler compared this to "investment in pork futures", and today this model has become the norm in the industry – companies such as Stripe, SpaceX, WeWork, Uber, etc. were able to obtain liquidity in the private market only before it became available on the open market。

This trend poses a challenge for the industry: LPs have difficulty in gaining easy access to liquidity, which hinders the allocation cycle. But this is a golden opportunity for institutions that believe that "technology companies will expand significantly" (e.g. a16z) – not only to provide opportunities to invest more in quality private enterprises, but also to transfer revenues that otherwise belong to open-market investors. In my view, this shift is one of the key reasons why windwards like a16z can grow in size without lowering returns。

In response to this trend, a16z has undertaken two key initiatives: to become a registered investment adviser (RIA), thereby freeing it to invest in encrypted currency, open stock and secondary market transactions; and to launch the previously mentioned LSV I Fund under the leadership of David George [9]. In the second phase, of the $32.9 billion raised by a16z, the LSV series contributed $14.3 billion. In addition, the Encrypted Monetary Fund has been split — the fourth Encrypted Monetary Fund (CNK IV) is divided into seed funds ($1.5 billion) and advanced funds ($3 billion)。

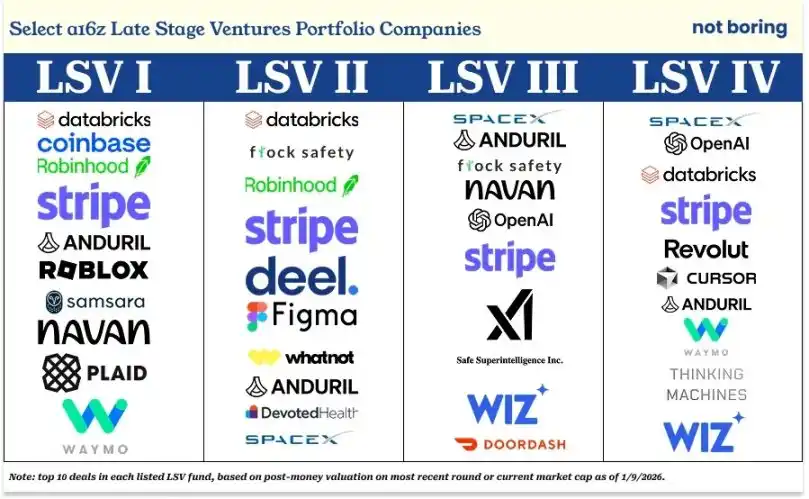

THE FOLLOWING ARE THE TOP 10 INVESTMENT ITEMS FOR EACH LSV FUND, RANKED ACCORDING TO THE LATEST POST-FINANCING VALUATION OR CURRENT MARKET VALUE:

LSV I: Coinbase, Roblox, Robinwood, Anduril, Databricks, Navan, Plaid, Stripe, Waymo, Samsara

LSV II: Databricks, Flock Safety, Robinhood (with exit from the open market and reinvested in Databricks), Stripe, Deel, Figma, Whatnot, Anduril, Devolded Health, SpaceX

LSV III: SpaceX, Anduril, Flock Safety, Navan, OpenAI, Stripe, XAI, Safe Superintelligence, Wiz, DoorDash

LSV IV: SpaceX, Databricks, OpenAI, Stripe, Revolut, Cursor, Anduril, Waymo, Thinking Machine Labs, Wiz

If a16z is invested to “spread the hotness of well-known enterprises”, as the outside world has previously accused, then the portfolio is undoubtedly a “quality heat list”. More importantly, according to Cambridge Association data for the second quarter of 2025, LSV I ranked 5 per cent in the top of the same tranche, and LSV II and LSV III were also 25 per cent in the top of the same tranche (i.e., first quarter)。

As of 30 September 2025, the net TVPI of LSV I was 3.3 times the net TVPI; the net TVPI of LSV II was 1.2 times the net TVPI (although this number may have risen after the recent completion of the financing of Databricks and SpaceX); and the net TVPI of LSV III was 1.4 times (in addition, there are reports that SpaceX is about to complete a large-scale secondary market transaction, valued or at $80 billion, which is two times higher than before, so that the net TVPI of LSV III is likely to rise further)。

The belief that the ultimate value of these head companies will be far greater than the expectations of most people (although not all of them — for example, the Foundations Fund — agree with SpaceX, Thrive's judgement of Stripe and a16z) has enabled a16z to invest more in these high-quality private technology companies while they remain private。

The key is that a16z has proven that growth-oriented funds can also achieve windfall-level returns under the right conditions. Specifically, according to the analysis I obtained from a16z LP, if Windward has a strong early investment capability, it will not only achieve windfall-level returns (multiple) but also higher internal returns (IRRs) through sustained additional investment in the growth phase. Of course, deeper cooperative relationships with these companies can further enhance the industry influence of a16z。

in the second phase, a16z considers that the most important objective is "to hold as many shares as possible in the head enterprise" - an objective that is easier to achieve if the company is better informed through early investment and is able to make additional investments on a continuous basis (or to make up for errors in early investment) with a dedicated, late-stage fund (although its shareholding ratio is still below the “control” level common in other asset classes)。

the core of this phase remains arbitrage, but unlike the first phase, a16z has done more to help individual portfolio firms succeed at this stage。

While the return cycle of the second phase of the Fund is not yet fully complete, the second phase of the Fund ' s return is now at a lead level compared to the performance of the first phase at the same time, when the Wall Street Journal reported poor performance。

a16z fund versus cambridge association industry benchmark investment return performance

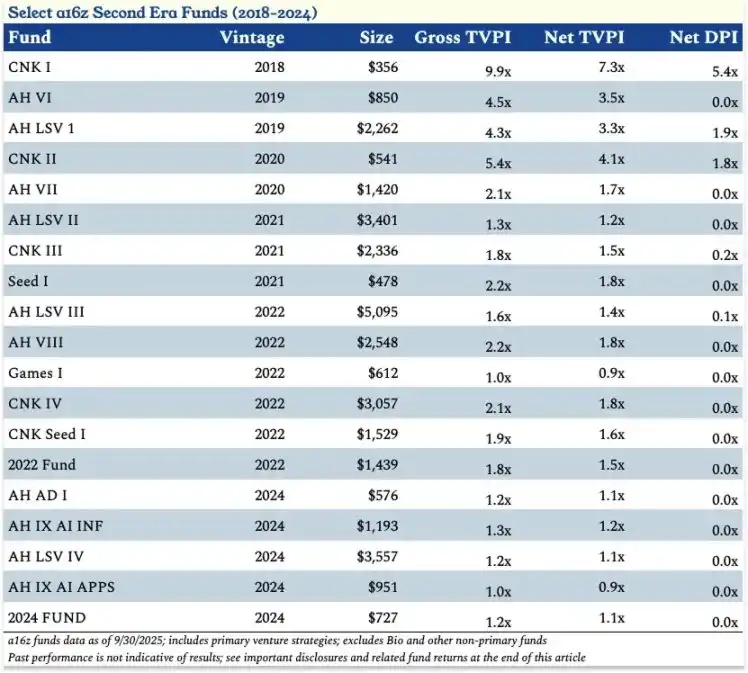

SPECIFICALLY, THE NET FUND RAISED IN 2018 WAS 7.3 TIMES MORE, THE FUND IN 2019 WAS 3.4 TIMES, THE FUND IN 2020 WAS 2.4 TIMES, THE FUND IN 2021 WAS 1.4 TIMES AND THE FUND IN 2022 WAS 1.5 TIMES。

a16z core performance data for part of the fund in 2018-2024 (phase ii)

The highlight of this phase is the outstanding performance of the Encrypted Monetary Fund (CNK 1-4 and CNK Seed 1) - of which CNK I has brought 5.4 times the net distribution to the paid capital ratio (DPI) returns to LP。

Even more surprising is the fact that, although a16z was questioned in 2022 about "the timing of the mistake and the collection of too many encrypted monetary funds", it has so far raised $3 billion for the 4th Encrypted Monetary Fund (CNK IV), 1.8 times the net TVPI。

The two core stories of the second phase — the LSV series of funds and encrypted monetary funds — coincided with a16z's belief in the future: the LSV is a "extension of the corporate private cycle and increased demand for private market financing." This trend responds to the fact that the encrypted currency represents an idea that innovation (and returns) may come from entirely new areas that differ from traditional investment tracks。

these two stories also highlight the need for a16z to further expand its services - both to support portfolio companies and to empower industries as a whole. for example, a16z needs to replicate part of the open market advantage in the private market in order to assist the development of later portfolio companies, while a16z has to go to washington (policy lobbying) to ensure the viability of the encrypted money industry in the united states and to ensure that new technology companies have a fair chance of competing with established giants。

this leads to the third phase of a16z (2024 - the future). at this stage, the core conviction is that, if there is an equitable development environment, new technology companies will not only be able to reshape industries, but will be able to win them all; and a16z will have to lead industries and the country as a whole in the right direction。

this belief has changed again the position of a16z. when the size of the company reaches a certain threshold (a clear sign is the $15 billion new fund raised this time), "selecting the winner" is no longer enough

To build winners, it is necessary to create an environment conducive to their competition。

As Ben said, "It's time to lead the industry." I don't know

phase three of a16z: it's time to lead the industry

At this point, you may be able to imagine a scenario in which a competitor's analyst sends a message to journalist Tad Friend saying, "In order for these two new funds, which total $15 billion, to yield 5-10 times more, you have to increase the size of the entire US technology industry several times over the current scale. I'm sorry

And you can probably guess that Marc and Ben will respond this way: Yeah, that's what we're going to do。

this is exactly the plan that a16z clearly proposed, the logic of which is as follows:

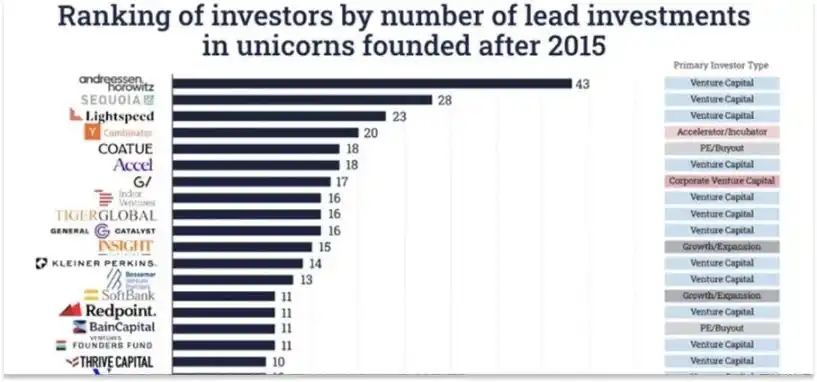

since 2015, a16z has invested in more unicorns at an early stage than any other investor, and the gap between it and the second-ranking investor (reswood capital) is comparable to that between second and twelfth。

Source: Professor, Stanford University, Ilya Strebulaev

CLEARLY, "THE NUMBER OF UNICORNS GROWING IN EARLY INVESTMENT ENTERPRISES" IS A VERY SPECIFIC AND EASY INDICATOR OF "BEST INVESTORS". THE MORE COMMON ASSESSMENT IS THE REFERENCE RATE OF RETURN — WHETHER IT IS A MULTIPLE RETURN, AN INTERNAL RATE OF RETURN (IRR) OR A SIMPLE TOTAL OF CASH ALLOCATED TO A LIMITED NUMBER OF PARTNERS (LP). THERE IS ALSO CONCERN ABOUT INVESTMENT IMPACT RATES OR PERFORMANCE STABILITY. THE WAY IN WHICH RANKINGS IN WINDFALL INDUSTRIES ARE ASSESSED VARIES FROM ONE PERSPECTIVE TO ANOTHER。

But this assessment, with the "unicorn number" at its core, seems to be highly consistent with a16z view of industry. In my interaction with the team in the field of encrypted money at a16z, I have repeatedly heard that: If it is because many good entrepreneurs are in a given area, it is entirely acceptable to be in that area, even if the final judgement is miscalculated; but it is unacceptable to choose the wrong investment enterprise in a given area, or to miss the final leader for any reason. As Ben said:

“We are well aware of the high risk of starting a business, and therefore we will not be too worried as long as the right process is followed in investing and risk is properly assessed, even if part of the investment ultimately fails. On the contrary, we would attach great importance to the failure to determine precisely whether an entrepreneur is the best candidate in his or her field。

The problem is small in the case of wrong emerging areas; the problem is serious in the case of wrong entrepreneurs; and the problem is also great in the case of bad entrepreneurs. Whether due to conflict of interest or voluntary abandonment, the consequences of missing an age-old enterprise are far more serious than investing in the best entrepreneurs in the area of miscalculation. I don't know

a16z has become a leader in the winding-up industry, according to its own definition of "core measure"。

Ben asked, "What does it mean to lead a business?" I don't know

IN A LONG ARTICLE ON THE X PLATFORM THAT ANNOUNCED THE COLLECTION OF $15 BILLION, HE GAVE THE ANSWER: "AS LEADER OF THE US WINDING-UP INDUSTRY, THE FUTURE OF NEW AMERICAN TECHNOLOGIES IS IN OUR HANDS TO SOME EXTENT. OUR MISSION IS TO ENSURE THAT THE UNITED STATES WILL WIN SCIENTIFIC LEADERSHIP FOR THE NEXT 100 YEARS. I DON'T KNOW

It is rare for a windfall company to say that。

but if you agree with the premise that science and technology are engines of progress, that the united states must have the technological advantage if it is to remain ahead of the lead, that a16z is the largest and most influential investor in america’s emerging science and technology enterprises, and that it has the capacity and resources to provide them with a level playing field with industry giants, then that is not unreasonable。

He further noted that in order to win the leading role in science and technology for the next 100 years (which, in a16z, appears to be equivalent to winning the overall leading position for the next 100 years), it was necessary to master the key new technological architecture — AI — and encrypted currency, and to apply these technologies to the most important areas, such as biotechnologies, national defence, health, public safety and education, and even to integrate them into government operating systems。

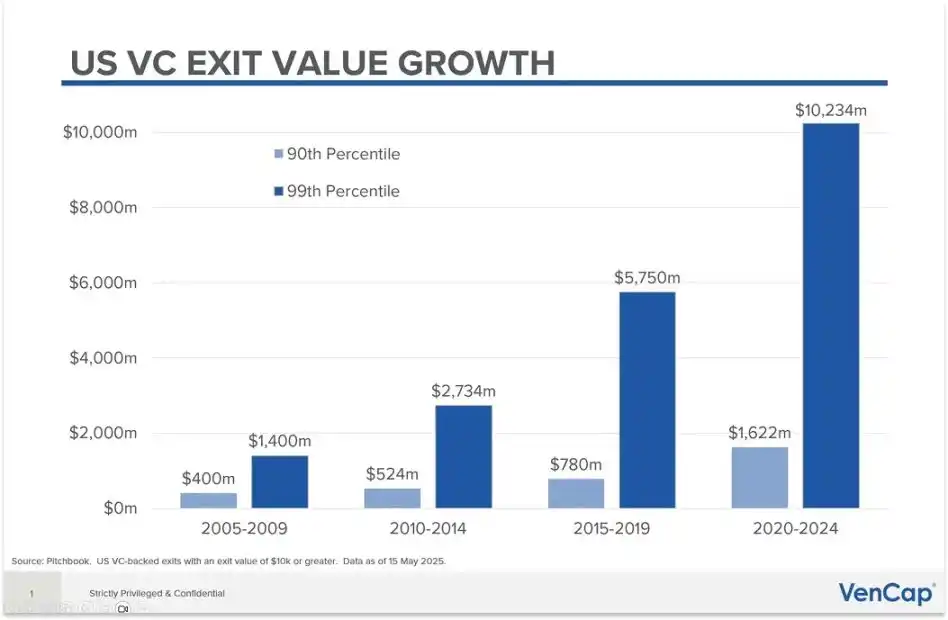

THESE TECHNOLOGIES WILL GREATLY EXPAND THE MARKET SCALE. AS I DISCUSSED IN MY ARTICLES " THE SIZE OF THE SCIENCE AND TECHNOLOGY INDUSTRY IS GOING TO EXPAND " AND " TECHNOLOGY FOR ALL " , INDUSTRIES AND TASKS THAT WERE NOT COVERED BY THE TECHNOLOGY INDUSTRY ARE NOW INCLUDED. THIS MEANS THAT THE INVESTMENTABLE VALUE OF WIND INVESTMENTS (VCAV) WILL ALSO INCREASE SIGNIFICANTLY。

The size of the US windfall exit is growing dramatically

this is the continuation of a16z’s long-standing investment strategy, but there is a key conceptual shift: as long as a16z fulfils his role as a good leader, these values can be released and the future of the united states (or even the world) secured。

Specifically, it means doing five things:

1. Reshaping the United States science and technology policy to bring it back to its peak

Filling the gap between private enterprise and the development of listed companies

3. Promote the evolution of marketing models to the future

4. To embrace new models of business creation

5. The continuous development of an enterprise culture while enhancing its capabilities。

a16z these seemingly puzzling initiatives are almost all aimed at achieving these five goals。

Most notably, over the past two years, a16z has become more vocal in the political sphere, and Marc and Ben have publicly supported President Trump in the last general election. This has led to widespread dissatisfaction, and the view has been expressed that investment funds should not interfere in national politics。

but a16z would strongly oppose that view. it wants "to reshape america's science and technology policy and bring it back to its peak."。

Marc and Ben set out their positions in the Small Science and Technology Enterprise Development Agenda, which can be summarized as follows:

Emerging science and technology enterprises are essential for national development。

To win the future, innovative legal, policy and regulatory systems are needed, while resource-rich industry giants must be prevented from blocking competition through "regulating capture"。

But the situation is the opposite: “We believe that poor government policies have become the number one threat to small technology enterprises. I don't know

Currently, there is no voice for emerging science and technology firms at the government level or against industry giants: industry giants will not do so and start-ups should not devote limited resources to such matters。

the financial gains of windsor are closely linked to the success of emerging technology firms, so that the windfall industry deserves to carry the flag; the leader of the windfall industry, a16z, is all the more responsible。

a16z is "single-oriented" in political positions, focusing only on the development of small technology enterprises, with a cross-party approach。

its public positions include: "we will not be involved in political disputes that are not directly related to small technology enterprises" and "we support or object to a politician, depending only on his attitude towards small technology enterprises and not on his party or on other issues." according to what i have seen and heard in a16z, these are not empty slogans, but their true operational norms。

a16z is involved in politics not because it's interesting (although at least Marc seems to enjoy this "hot scene"; he seems to be passionate about many things and can find humor in myths) It is an undervalued competitive advantage, but we do not have time to discuss it today). In the short term, a16z is willing to suffer from "stupidity" and criticism only to allow new technologies to flourish in the long run。

As Bill Gurley, a former partner in Benchmark, pointed out in 2581 Mile, for a long time, the technology industry has largely ignored Washington (the United States government), and Washington has largely ignored the technology industry. A few years ago, however, the situation changed, partly because, as I mentioned earlier, the technological sector has moved from being "manufacturing tools" to "competing with industry giants." The encryption money industry is the first area to face the pressure of "survival" regulation。

When a16z first entered the political circle of Washington, "Small Technology Enterprises" were not an influential group in Washington. Large technology companies have exclusive networks of lobbyists and government relations; industry giants — be they banks, defence firms or champions in other areas — also have their own lobbying resources and connections. However, there is no such support for small technology enterprises, including encrypted money enterprises. At that time, apart from Coinbase’s potential, no small technology enterprise could afford the cost and upfront of establishing a representational mechanism in Washington, D.C. (and even in the US state parliaments)。

As a result, in October 2022, a16z encryption currency team hired Collin McCune as the head of government, who led efforts to spread the knowledge of encrypted currency to US politicians. Collin, Chris Dixon, a16z General Counsel in the field of encryption currency, Miles Jennings, other members of the team, as well as entrepreneurs from the a16z portfolio and the entire encrypted money industry, travelled to Washington on several occasions to explain to politicians the operation of encrypted currency, its potential for development, and, more importantly, the risk that excessive regulation may lead to new technologies being "dead."。

These efforts have borne fruit. Thanks in large part to their contribution and that of the Inter-Party Political Action Committee, Fairshake SuperPAC, the encryption currency industry is no longer at risk of being "capped" by legislation. Last year, President Trump signed the GENIUS Act, which for the first time brought encrypted stabilization coins under regulation; in the meantime, a comprehensive bill on encrypted currency market structures was passed in the Chamber of Deputies with overwhelming cross-party support and is currently before the Senate for consideration, which is expected to be adopted later this year and signed into force。

This experience played an important role when artificial intelligence became the focus of Washington. Today, McCune is responsible for the entire government service of a16z, and has established a permanent presence in Washington, D.C., covering various areas such as AI, encrypted currency, and American Dynamism. At present, a16z is advocating the establishment of uniform federal standards of regulation of artificial intelligence in order to avoid inconsistencies in cantonal regulatory policies and to promote other policies conducive to innovation。

While the term "loaning" may have negative connotations, the current reality is that small technology firms’ competitors have mature government affairs and policy teams that are trying to make it difficult for new entrants to achieve a level playing field through "regulating capture."。

for the science and technology industry to win the future, for a 16z fund to pay off, it is no longer a viable option. the good news is that the survival of a16z depends on the creation, growth and success of new and emerging enterprises, and that it is therefore more motivated than any institution to maintain a level playing field conducive to innovation。

because even a16z itself admits that in the present, no one can predict what will happen in the future, nor how they will be born。

“new models for the acceptance of business start-ups” means recognizing the possibility that, with artificial intelligence technology, the number of employees that entrepreneurs may need to start a business in the future may be only 1/10 or even 1/100 in the past, and that the elements needed to build a good business may be different from those of the past. it also means that a16z itself needs to be adjusted。

For example, a16z has launched an internal accelerator project called "Speedrun": an investment of up to $1 million for start-ups and a 12-week incubation programme. Through the project, a16z is able to learn in advance about the start-up model of these new enterprises and to examine in depth each of the participating enterprises, thereby making it wiser to invest more in potential enterprises。

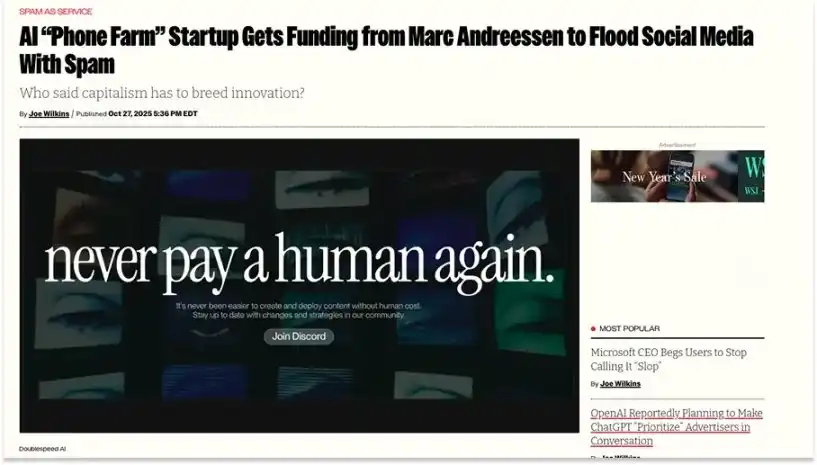

But this initiative also carries risks: increasing the number of businesses that can claim to have a16z investment and lowering the investment threshold may dilute the brand credibility of a 16z. For example, a16z has been controversial on platform X because of the investment in the Spedrun project by a company called Doublespeed — a company that claims to provide “synthetic creator infrastructure” but has been accused by others of “cell phone farms” and “waste information is service”。

Source: Futurism

The argument that “the company has received an investment from Marc Andreasen” is ironic, because Marc would not be involved in investment decisions for the Spedrun project for less than $1 million, after all, only about 0.001 per cent of a16z asset management scale. But that's exactly what's at the heart of the problem: I've seen a lot of references to this "a16z-funded business" on platform X, and it wasn't until later that I figured it might be a Speedrun hatching project, so I checked it out. Most people do not spend time verifying this。

Another more controversial case is Cluely, a start-up company that claims to be able to "help users cheat in a variety of matters", while a16z has led an investment of $15 million in the company through its artificial intelligence application fund。

One has reason to wonder why a16z, as an institution dedicated to shaping the future of the United States, invests in an enterprise that places "virtual transmission" above "ethics." Would the existence of a business like Cluely in a portfolio, in the eyes of people active in the network, undermine the credibility of all other investment firms

The answer is probably yes. Personally, I do not agree with this investment decision — it gives people a sense of “indecent” and “indecent”。

but! this decision is consistent in its own logic。

Because leaving out the product itself, the central message of Cluely is that, in the age of artificial intelligence, there is a fundamental change in business start-up patterns. This is premised on the fact that the capabilities of the bottom model are becoming integrated and commodified, so that the "dissemination capacity" will be the only key element; even if there is some controversy in order to be disseminated, it is irrelevant。

If a16z is really committed to "a new model of business acceptance", then it would be less costly to use $15 million and a small X platform dispute in exchange for a "front seat" to observe a very innovative business start-up model。

more broadly, in the industry in which a16z is located, it is a necessary cost to avoid repeating kodak’s mistakes. enterprises must be willing to take risks that go far beyond the financial dimension. at the size of a16z, a small investment is the least risky risk。

However, the view was also expressed that, in general terms, these minor disputes on the X platform (which is itself a 16z portfolio enterprise) were not relevant. In fact, when I asked a16z general partner, Katherine Boyle (who was also a co-founder of the company's American Dynamics business), she said:

"YOU MIGHT SAY, YES, WE DO GET SOME CRITICISM ON X PLATFORM FOR CERTAIN BUSINESSES -- PEOPLE IN SAN FRANCISCO OR IN SOME CIRCLES IN NEW YORK DON'T LIKE A COMPANY, THEY SAY, "WE DON'T LIKE THEM DOING AMERICAN DYNAMICS." WE DON'T LIKE THEM DOING ENCRYPTED MONEY! # I DON'T KNOW #

But in terms of the size of our entire system, these small-time disputes are not significant。

The top institutions have a system of scale, like the United States. Do we care when the United States makes some awkward moves on the global stage? No, as this would not have a material impact on the United States, just as similar events would not affect the Roman Catholic Church。

The dimension of our thinking is the century, not a tweet. I don't know

you may not agree with all the a16z, but you have to admire the company's boldness。

It is worth mentioning that when I asked some of the a16z's LPs what they thought of the businesses that caused the X platform dispute, they often responded with a blind face to ask, "Who?" - Apparently they've never heard of them。

For the return of a16z, what is really important is that the "leading enterprises" identify them as early as possible, successfully participate in their financing transactions and hold as many shares as possible over the long term. If you ask any of the a16z LPs if they know Databricks, they're all familiar。

Today, in the third phase of the “leading industry”, it is equally important that these leading enterprises continue to grow, even if they have expanded significantly。

I think that is what Ben meant by "filling the gap between private enterprise and the development of listed companies" -- and that is the most critical perspective of understanding a16z positioning now and how it is expected to yield a return of 15 billion dollars to 5-10 times。

Ben stated: "In the past, windfall investments have helped enterprises to earn $100 million and then hand them over to investment banks, which take over the business ' s subsequent listing process. But this time has gone on forever. Today's businesses not only remain private for a longer period of time but are also larger - this means that the industry represented by a16z needs to upgrade its capacity to meet the development needs of large enterprises。

To this end, a16z recently hired former VMware CEO Raghu Raghuram to give him a "triple role": as a general partner in the artificial intelligence infrastructure team led by Martin Casado, as a general partner in the growth investment team led by David George, and as a management partner in Ben's "adviser to assist its operating company". Raghu will co-lead a series of new initiatives with Jen Kha to "satisfaction the needs of large enterprises as they grow."。

In particular, these initiatives include: working with Governments around the globe to help portfolio enterprises develop and market expansion locally; building strategic partnerships with enterprises such as Eli Lily (which have jointly launched a $500 billion Biosciences Eco-fund); expanding the number and depth of limited partnership (LP) relationships globally; and expanding the services of a16z HLCM, which can provide customized services to large enterprises to directly connect them in relevant areas of the a16z portfolio。

even for large enterprises, it is neither realistic nor cost-effective for some resources to be created individually from zero, but it is a reasonable option for a16z to be unified and allocated to the entire portfolio. these resources coincide with the level of government, trillions of dollars in size and trillions of dollars in capital。

All these initiatives may allow businesses to remain private without sacrificing the credibility, cooperative relationships or access to financing that listed companies have。

this means that businesses can grow to larger-scale private markets - and private markets are the core areas covered by a16z。

this also means that a16z has the opportunity to invest more money and have a reasonable chance of getting a good return; and that more returns translate into more resources to enhance its own capabilities and to increase industry's influence – capabilities and influence that can further empower its portfolio of firms and even gradually the entire emerging science and technology industry, thereby promoting more and better-quality new technologies to be applied to more areas of the economy, ultimately giving everyone a better future。

Of course, there are risks inherent in the process. "The money's a lot of trouble," and the leaders always have to face more controversy, etc。

in my view, a16z is competing in industries on an unprecedented scale, with both opportunities and risks。

For example, the wider the coverage of operations, the more potential risk points naturally become. In theory, the longer an enterprise remains private, the more difficult it will be to create liquidity for a limited number of partners (LPs), and the more difficult it will be to invest in new funds, which are the financial base of a16z to invest in potential future giants。

ULTIMATELY, HOWEVER, THERE ARE TWO CORE GROUPS THAT DETERMINE EVERYTHING: THE FOUNDERS AND THE LP, WHO ARE BOTH CLIENTS AND INVESTORS OF THE COMPANY。

THE ONLY TWO KEY GROUPS: THE LP AND THE FOUNDER

These attitudes towards a16z, which the founders chose to accept for investment in, the LP to invest in, and the attitude of the founders to the a16z, amplified all the core logic that I discussed before。

The logic of my analysis is as follows:

if the top founders believe that a16z set-up system will help them to create a larger business than other means, they will give priority to a16z investment (at least ensuring that a16z is one of the objects of their financing)。

If LP believes that a16z will continue to invest in the best founders, even in the face of a liquidity crisis, they will give priority to a16z and hold their share of the fund。

When I spoke to Jen Kha, she shared anecdotal information that clearly showed that in the wind industry, "the best business in the world" was the only thing that matters。

A few years ago, during the brief windfall to Bear City, the market faced both liquidity concerns and uncertainty over the position of the Trump Government on the tax status of the Endowment Fund. a16z offered liquidity support to LP. Looking back at the news reports at the time — including rumours about top-level endowment fund sales portfolios — it was easy to find that a16z was carrying a glass of water in the desert。

Specifically, fund number a16z I (Fund 1) holds a seeder share of Stripe, while fund number III (Fund III) earns a large share in round A of Databricks. "We know you are facing a liquidity crisis." If you like, we can buy back the shares of these businesses in your hands and create some liquidity for you. I don't know

"Packy, this is the case," Jen recalled, "30-bit LP all reply "no consideration." They said, "Thank you for your kindness, but we do not want to cash out of the shares of these businesses, but we want to sell out the shares of others." I'm sorry

As a16z LP, VenCap Chief Investment Officer David Clark explained: "The core of windfall investment is not short-term liquidity, but multi-year compound growth. We do not want the fund manager to sell the best corporate shares prematurely. I don't know

Anne Martin of Wesley University is one of the 30 early LPs, and her investment experience is evidence of the resilience. Since the establishment of Fund No. 1 in 2009, she has supported this institution - She was also in the Yale Endowment Fund; she is now the chief investment officer of the University of Wesley and has participated in a16z 29 funds. a16z The recently collected fund will bring this figure down to 30。

"A16z, in my portfolio of leading investments, is not only large in size, but also the longest in time," she said last month when I spoke to Anne, "I recommended two new fund managers, a16z, to members at my first Investments Committee meeting. I don't know

Initially, Anne invested in a $300 million fund — Jen — saying, “She consulted directly with Ben on the terms of the Limited Partner Agreement (LPA). Anne shares the view of a16z that "market opportunities are enough to support larger funds":

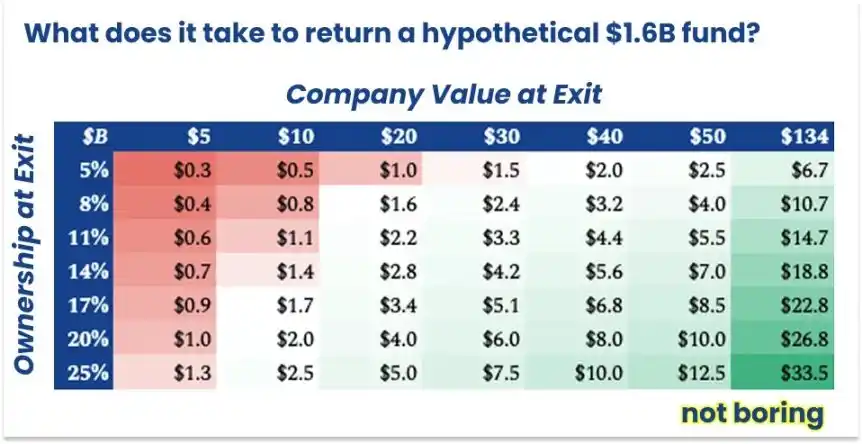

the special thing about a16z is... in the case of a $1.6 billion aii fund, you can simply set out a matrix: "assuming that they hold 8% of the shares at the time of the enterprise's withdrawal... how much will it take to get the fund back? if you hold 8% of the shares, you need the firm to withdraw to $20 billion. although such cases are not common, a16z seems to have been able to cast quite a few. of even greater concern is whether an 8 per cent shareholding ratio is reasonable for them. because in many cases, their shareholding is much higher. i don't know

Just for illustrative reference... but it's practical

"I think it's about equity for them and the ability to help these businesses achieve huge results," Anne tells me, "it's these two things that reassure the LP about large-scale funds. I don't know

it is precisely this ability to “help the firms achieve huge results” that makes even the most popular founders willing to offer a16z a better investment than other competitors. in 2025 alone, a16z made investments at lower value than other top institutions in the same round. although it is not easy to reveal the names of specific enterprises, i understand that in the past year alone, four well-known enterprises in the field of science and technology used this model in financing。

In fact, the founders were highly appreciative of the resources available from a16z and were sometimes willing to accept valuations below market levels. This is quite different from the situation in the early days of a16z, when the competition even gave it the nickname "A-Ho" because it was dissatisfied with a 16z, which is often expensive. Today's changes are sufficient proof that working with a16z can bring real and concrete value, and that companies are willing to trade for a higher dilution ratio。

This means that, although I mentioned two key groups before, in the end, there's only one core: if the top founder is willing to work with a16z, the best LP will follow。

a16z can the development results of the enterprise be enhanced

That's the core of the problem, isn't it? We can express it in a hypothetical formula:

a16z market value of contributions x total market value affected

And the difficulty of this formula is that if we want to raise the "contribution ratio" significantly on the left, we have to "cut the total market value" on the right. The minimum hours (i.e. the early stages of the enterprise) to help。

However, when you really help small businesses grow into giants of industry, your loyalty is priceless — the founders will volunteer to recommend you to other consider-financing founders, and they will speak for you in the media。

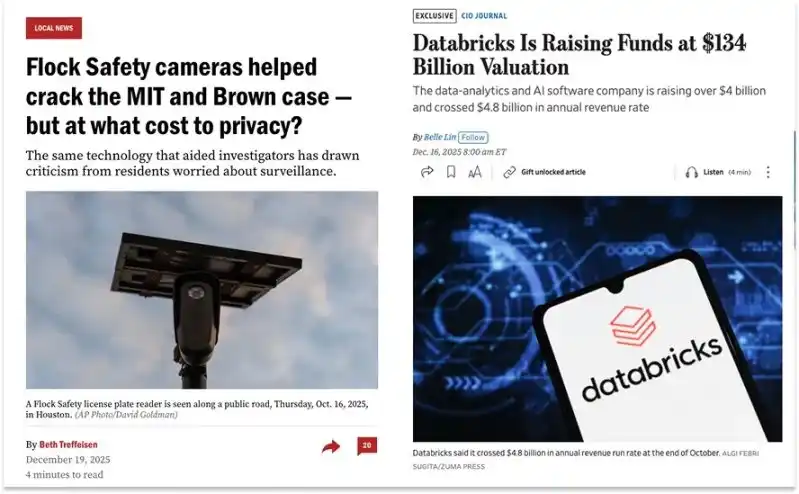

Earlier, I asked Erik Torenberg to help contact the founders of the a16z investment, who, in a few hours, had docked me with the founders of a business whose total market value was over $200 billion, including Ali Ghodsi of Databricks and Garrett Langley of Flock Safety。

I mention in particular the two founders because, within 48 hours of our association, two major events took place: the announcement by Databricks of $4 billion in financing, valued at $134 billion; and the assistance of Flock Safety in apprehending the alleged perpetrators of the murder of Brown University and MIT affiliates. These two things are a visual expression of the influence of a16z being invested in businesses。

Source: Boston.com and Wall Street Journal

but what i really want to know is how a16z uses its influence to support these businesses. does this support really change the trajectory of business? a16z a system of resources that invests hundreds of millions or even billions of dollars does it really bring about significant changes for enterprises

believe a16z in the third phase of the bet — that is, by increasing the size of the market for new and start-ups in science and technology and by increasing the value of the invested enterprises, creating a substantial return on the $15 billion new fund — you may need to believe that the answer to that question is yes。

And the answer is yes。

In retrospect, Ali of Databricks said: "No a16z, no Databricks today. One enterprise alone has added $134 billion (and is still growing) to the investmentable market, and a 16z net return of about $20 billion. Even if his statement was somewhat exaggerated, it would be difficult to argue that a16z's support for Databricks — from early marketing assistance to facilitating cooperation with Microsoft to helping build specific sectors — already covers all the inputs that a16z has made to the platform since his establishment。

In fact, we can make the assumption that if a16z still holds approximately 15% of the Databricks shares, a rough calculation is known, as long as a16z contributes about 25% of the value of Databricks, it will cover the regular windfall management fees it has charged since its inception。

All the founders I interviewed referred to a16z, a consistent working model — regardless of the general partner (GP) that clearly had the shadow of the Innovator Broker CAA: they would not interfere to allow you to run the business on your own when you did not need it; they would support it if you asked for it。

This is also a 16z key way to win investment transactions: the GPs of the funds are responsible for determining the investment target and, when needed, they mobilize all the company's resources — including Marc and Ben himself — to do their part。

"The company's ideal state is decentralization, shared faith, coordinated attack," David Haber told me, "Marc would basically say, "If you tell me it's the next Coinbase, I'll fly anywhere in the world. I could invite this entrepreneur to dinner at my house tonight. Do it now, at all costs. I'm sorry

AFTER THE DEAL WAS COMPLETED, THE SAME WAS TRUE OF THE PARTNERSHIP MODEL BETWEEN THE GP AND THE FOUNDERS。

“No matter what the circumstances, their support is unreserved. A16z would even overwhelm me and the team that was created, and they would never interfere too much, even if our views were divided, and Ali said, "But as long as you need help, they will be fully committed to ensuring that the problem is solved. I don't know

Of course, a16z's support for Databricks is so, and I heard exactly the same thing from a couple of other early-stage a16z companies。

a16z The CEO and co-founder of XMTP, Instant Communications Protocol Inc., an investment in encrypted currency, informed me that: